If you have a business idea but limited money to start with, bootstrapping is probably one of the first options you will come across.

It is how most founders actually start, using their own savings instead of outside investors.

But for a first-time founder, it brings up some honest questions. Can you really start without investors? How is bootstrapping different from raising money? And is it the right choice for your business?

These are important questions to answer before putting your own money into the business. Bootstrapping gives you full control, but it also puts your savings at risk.

In this guide, I’ll explain how bootstrapping works and how to know if you can afford it. We’ll also look at founders who did it successfully and when it makes sense to raise outside funding instead.

What is bootstrapping in business?

Bootstrapping means starting and growing a business with your own money and the income the business earns, instead of taking money from investors.

In simple terms, you use personal savings to get started, find paying customers as early as possible, and reinvest the money you make back into the business.

Many bootstrapped founders handle most things themselves in the beginning, including sales, marketing, customer support, and day-to-day operations. Growth is usually slower, but you keep full ownership and control of the business.

Should you bootstrap or raise funding?

This is one of the biggest questions first-time founders struggle with.

The real answer is not always “bootstrap if you can” or “raise money if you want to grow fast.” The better question is: what kind of business are you building?

Some businesses work well with bootstrapping. Others need funding from the start.

Bootstrapping means you build the business with your own money and the money your customers pay you. You usually keep more ownership and control. You do not have investors, board meetings, or pressure to sell the company within a certain number of years.

But there is a tradeoff. You can only grow as fast as your revenue allows. You also take all the financial risk yourself.

Raising funding works differently. You get outside money, which can help you grow faster, hire earlier, and compete more aggressively. But you give up some ownership, share decision-making, and bring in investors who expect a return.

The simple way to think about it is this:

- Bootstrapping = more control, slower growth.

- Raising funding = faster growth, less control.

Neither option is automatically better.

It depends on how much money your business needs before it can start making money, how quickly customers pay you, and how expensive it is to grow.

Which businesses are easier or harder to bootstrap?

Some businesses are easier to start with little money. Others need a lot of capital from the beginning.

| Easier to bootstrap | Harder to bootstrap |

| Consulting and freelancing | Hardware and manufacturing |

| Digital agencies | Biotech and pharma |

| Low-cost SaaS | Deep tech and AI research |

| Online courses and coaching | Marketplaces |

| Newsletters and paid media | Expensive retail businesses |

| Print-on-demand e-commerce | Restaurants and hotels |

| Dropshipping stores | Medical devices |

| Simple mobile apps | EV and clean energy startups |

| Digital products and templates | Real estate development |

| Bookkeeping and accounting services | Logistics and supply chain businesses |

The pattern is simple. Businesses on the left are easier to self-fund because they can start small, get customers quickly, and grow from their own sales. Businesses on the right usually need more money upfront, more time to launch, or both, which makes self-funding much harder.

How do you know if you can afford to bootstrap?

To know if you can bootstrap, look at two numbers:

- How long your money will last

- How long your business will take to pay for itself (break even)

If your money lasts longer than the time your business needs to break even, you can probably bootstrap.

If your money runs out before the business can cover its costs, bootstrapping will be risky.

The first number is called your runway.

Runway means how many months you can keep going with the money you have today.

The second number is your time-to-break-even.

Time-to-break-even means how long it will take until your monthly income covers your monthly costs.

As I mentioned in the table above, some businesses are easier to bootstrap because they can start small and make money quickly. Others are harder because they need more money upfront and take longer to cover their costs.

A simple rule: If your runway is longer than your time-to-break-even, you can afford to bootstrap.

But do not cut it too close. Try to have at least a 2 to 3 month cushion.

For example, if you think your business will break even in month 6, your money should last until at least month 8 or 9.

If your money only lasts until month 6, one bad month can put the business in trouble.

How to calculate your runway?

Use this formula:

Runway = total cash you have ÷ monthly expenses

Your total cash is the money you have saved for the business and your personal life.

Your monthly expenses include both business costs and personal costs.

That matters because if you are bootstrapping full-time, the business has to support both the company and you.

But not everyone bootstraps full-time.

If you still have a job, freelance income, or a partner with a steady income, your runway can be much longer.

So it is smart to calculate both:

- What happens if you go full-time

- What happens if you don’t

Example: Here is what the math looks like for a solo founder starting a consulting business.

| Item | Amount |

| Personal savings set aside | $30,000 |

| Monthly personal expenses | $3,500 |

| Monthly business expenses | $500 |

| Total monthly burn | $4,000 |

| Runway, best case | 7.5 months |

| Runway with 30% buffer | 5.8 months |

In the best case, this founder has 7.5 months before the money runs out.

But real life usually costs more than expected. With a 30% buffer, the safer number is closer to 6 months.

That means this founder should try to get the first paying client within 60 to 90 days.

They should also aim to reach around $4,000 in monthly revenue by month 4 or 5, not wait until month 6.

Many founders do not run out of money because the business idea was bad. They run out because they planned for everything to go perfectly.

Steps to bootstrap a business

You don’t need a 50-page playbook to bootstrap a business. You just need to take a few important steps in the right order.

Here are the five that matter most:

1) Write a simple spending and revenue plan

Before you spend a dollar, write down two things: how your business will make its first sale, and how long your cash will last while you get there.

This is not a formal business plan with market analysis and projections. It is a short working document, one or two pages, that answers four questions:

- What will you sell, and how will you make your first sale?

- What will it cost you to run each month?

- How much cash do you have to spend on this?

- How long will that cash last before the business covers its own costs?

The point is to know your runway before you start spending.

This plan also gives you something to check later. If sales are slower than expected, you can look back and see which assumption was wrong.

2) Start with your savings, but set a hard limit

Many founders start with $5,000 to $30,000 of their own money. The exact amount matters less than the rule you set around it.

Before you put money into the business, decide on two things in advance.

- The maximum amount you are willing to invest in the business.

- The personal savings you will not touch, no matter what.

This could be your emergency fund, six months of rent, or anything else you need to protect.

This sounds obvious, but many founders skip it. Without a hard limit, “just one more month” can slowly drain your bank account.

3) Get to your first paying customer fast

Revenue is the only fuel a bootstrapped business has. The sooner you collect money, the longer your runway lasts.

Do not wait for the product to be perfect. Do not wait for the website to look polished. Start with the smallest version of your offer that someone would actually pay for, and begin selling.

Two ways to get to revenue faster:

- Pre-sell before you build. Take deposits, early orders, or signed interest before the full product exists.

- Sell to people you already know first. Your network is usually your fastest sales channel.

If you cannot sell a rough version to anyone, the polished version may not sell either.

4) Stay lean as you grow

Once you launch, keep your costs as low as possible for as long as possible.

Today, this is easier than ever. AI tools can help with writing, research, customer support, and admin work that used to require freelancers or employees.

No-code tools can help you build a SaaS product, e-commerce store, or membership site without hiring engineers. Many hosting, CRM (Customer Relationship Management), accounting, and email tools also have free plans that are enough to get started.

Do not pay for something if a free version works.

And do not upgrade just to make the business look more serious. Upgrade only when the free version becomes a real limit.

5) Track your cash every week

Bootstrapped businesses do not have outside funding to fall back on. That makes cash the most important number to watch.

Many founders check cash once a month, or only when something feels wrong. That is too late. By the time you notice a cash problem in a monthly review, you may have already lost three weeks you could have used to fix it.

Once a week, spend 15 minutes checking:

- How much cash is in the bank right now

- What bills are due in the next 30 days

- Which invoices clients still owe you

- How much revenue you expect in the next 4 weeks

- How much runway you have based on those numbers

This is not about worrying all the time. It is about catching small problems early.

A client who is 30 days late may only need a reminder call. A client who is 90 days late can turn into a serious cash flow problem.

6) Reinvest only where it helps revenue

When money starts coming in, it is tempting to spend it.

A better office. Your first hire. A marketing agency. Better tools.

Try to resist that for as long as possible. In the early stage, every dollar you put back into the business can help it grow faster later.

A simple rule: if an expense doesn’t help you earn more revenue or save a meaningful amount of time, it can wait.

These five steps are what bootstrapping looks like in real life. Follow them well, and you can turn an idea into a business that covers its own costs.

Once you get there, the question changes. Instead of asking, “Can I afford to bootstrap?” you’ll start asking, “Should I keep bootstrapping, or is it time to raise funding?”

When to switch from bootstrapping to raising funding?

Many founders feel like raising money means they failed at bootstrapping.

It doesn’t.

The steps that help you get from an idea to a working business are not always the same steps that help you grow to the next stage. Knowing when to switch is part of building the business.

Here are five signs it may be time to consider outside funding.

1) Demand is more than you can handle

Customers want what you offer, but you can’t keep up.

Maybe you’re turning down customers, missing deadlines, or losing deals because you can’t hire or grow fast enough using revenue alone.

Before you treat this as a funding problem, try raising your prices first. Higher prices can help you manage demand and bring in more revenue.

But if you’ve already raised prices and still can’t keep up with strong demand, that may be a sign the market wants more than you can deliver right now.

2) A big opportunity comes up, but you can’t afford it

Sometimes a clear growth opportunity appears, but you don’t have enough cash to take it.

It could be a bulk inventory deal, a new market, or an infrastructure investment that would likely pay for itself.

If you can’t fund it from cash flow, outside capital may make sense.

But this does not always mean equity funding.

Equity funding is usually better saved for bigger, riskier growth moves.

3) Funded competitors are moving ahead in a market where size matters

This does not apply to every business.

In many markets, bootstrapped and funded companies can compete side by side. Basecamp, for example, still competes in a space with funded tools like Asana, Monday, and Trello.

But some markets reward speed and size more than others.

If competitors are locking up customers, signing exclusive partnerships, or controlling important sales channels, slow growth can become a real problem.

In those cases, funding may help you compete before the market gets harder to enter.

4) You are burning out

Bootstrapping often means the founder does almost everything.

That can work in the beginning, but it can become too much over time.

If you’re working long hours, losing sleep, and the business still needs more than you can give, the current setup may not be sustainable.

Funding can help you hire people and reduce the load.

But hiring is not an automatic fix. You also need to be ready to hand over work and manage the team. Otherwise, hiring while burned out can just add more work.

5) The market window is closing

Some opportunities do not stay open for long.

A new regulation, a change in customer behavior, or a short-term advantage over bigger competitors can create a limited window to grow.

When timing is the main advantage, growing slowly can become the wrong tradeoff.

You do not need all five signs. One or two steady signals are often enough to start thinking seriously about raising money.

If you decide to raise, the work changes. You need to make the business fundable. That usually means clean financial records, a clear plan for how you will use the money, and proof that customers want what you sell.

If you’re seriously considering this path, our guide on raising outside funding walks through what comes next.

But raising money is not the only right move.

Some founders stay bootstrapped and build steady, profitable businesses. That is a real choice too.

Staying bootstrapped isn’t the mistake. The mistake is ignoring what your business is telling you and continuing with the same approach that only worked at the start.

Plenty of founders have faced this decision. Here’s how a few of them handled it.

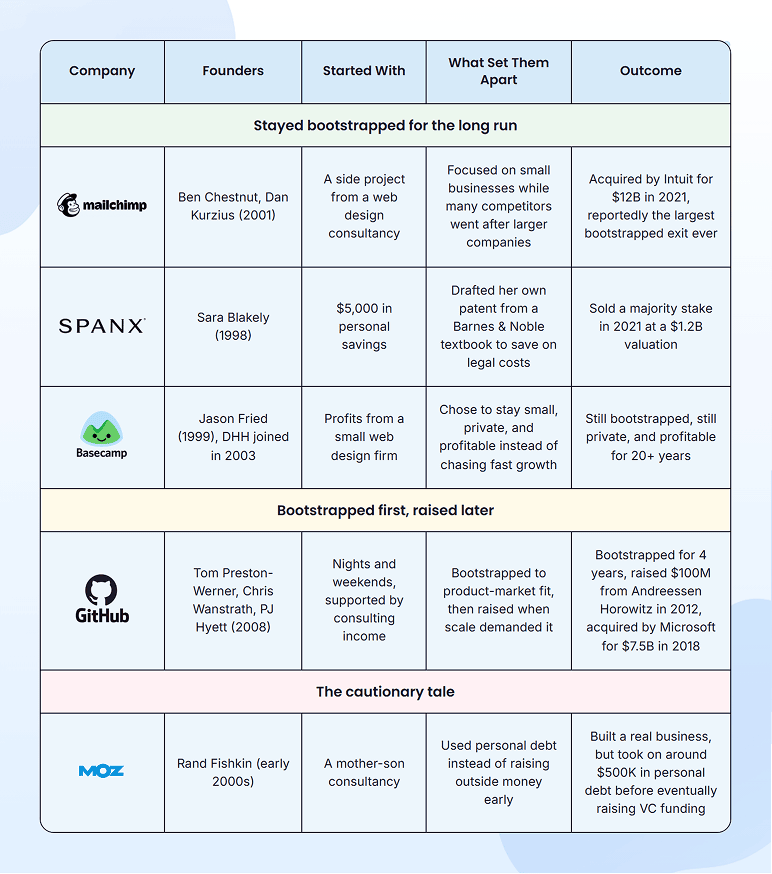

Examples of successful bootstrapped companies

Some well-known companies started with personal savings, side income, or small service businesses. They did not raise money right away. They grew slowly, stayed focused, and made careful choices.

If you’re trying to start a business without much money, these are useful stories to study.

Here are five real examples. Some stayed bootstrapped for the long run. Some bootstrapped early and raised later when the timing was right. And one shows that even successful bootstrapping can come with serious financial pressure.

The common pattern is that each founder made a clear choice early on.

- Mailchimp focused on small businesses.

- Spanx kept costs extremely low.

- Basecamp chose profit over fast growth.

- GitHub charged customers from the start.

- Moz shows that bootstrapping can work, but it can also create real personal financial strain.

Bootstrapping is not one fixed playbook. It is a set of tradeoffs. Every founder has to decide how much control, risk, speed, and pressure they are willing to take on.

Bootstrap or raise funding, but have a plan!

Bootstrapping or raising funding can both work. The mistake is choosing either one without a plan.

Bootstrap without planning, and your savings can run out too soon.

Raise without planning, and you may give away equity you did not need to lose.

So choose on purpose. Run the numbers, understand the risk, and write a business plan before you start spending.

A plan will not guarantee success, but it gives you something to measure against when reality changes.

Upmetrics AI business plan generator can help you build the structure, financials, and forecasts you need.

Bootstrap or raise. Just do not drift.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Anthony Ray

Anthony Ray is an SBA Commercial Loan Officer specializing in commercial lending, financial analysis, and risk management. Over the years, he has helped business owners secure the financing they need to grow and succeed. Besides that, he shares practical insights on banking, loans, and financial strategies based on his industry experience. Read more