If you’re reading this, you probably just got a no. Maybe today. Maybe an hour ago. Maybe the rejection email is still open, and you’ve read it four times trying to figure out what they really meant.

I’ve been there. Every founder I know who has tried to raise money has been there, too.

Let’s say the obvious part out loud, because most advice skips it. This hurts. The self-doubt shows up fast. You start wondering if you’ve completely misunderstood the opportunity. You feel embarrassed because you told friends or family that investor conversations were going well. You may even want to send a long email explaining why the investor is wrong.

Feel all of it. It doesn’t mean you’re weak, and it doesn’t mean your company is finished.

One thing I wish someone had told me earlier is this: most investor feedback is not really about your business. The founders who deal with rejection well stop reacting to every single no. Instead, they look for patterns across many conversations.

In this piece, I’ll give you three things in this order. Permission to feel what you’re feeling. A frame for what just happened on the other side of that meeting. And the tactics for what to do next.

Don’t make any decisions tonight

Right now, your brain wants to do something:

- Reply to the email

- Redesign the deck

- Message your co-founder late at night asking for thoughts

- Move to the next investor and push even harder

That feeling does not mean you’re falling apart. It means you care. Founders who can easily brush off a serious investor rejection usually either stopped caring a long time ago or were never deeply invested to begin with. Neither is a good sign.

The problem is that the same instinct that makes you care also makes you react. And tonight, those reactions probably won’t lead to your best decisions.

That’s why the rule is simple: wait 24 hours.

Not because the feeling will disappear. It may not. But because the calm and rational part of your brain is exhausted tonight. It comes back tomorrow. Most things you send tonight would probably be rewritten tomorrow. Most decisions you make tonight would probably feel questionable by the next afternoon.

So tonight, don’t reply to the email. Don’t spend hours trying to understand every reason they said no. Don’t update your team if you’re still emotional. The clear thinking you’ll have tomorrow is more valuable than anything you can do tonight.

You’re not behind. You just had a hard day in a long process.

Why investors actually say no (and why their reasons rarely are the reason)

The hardest part of a rejection usually isn’t hearing no. It’s hearing the reason behind it:

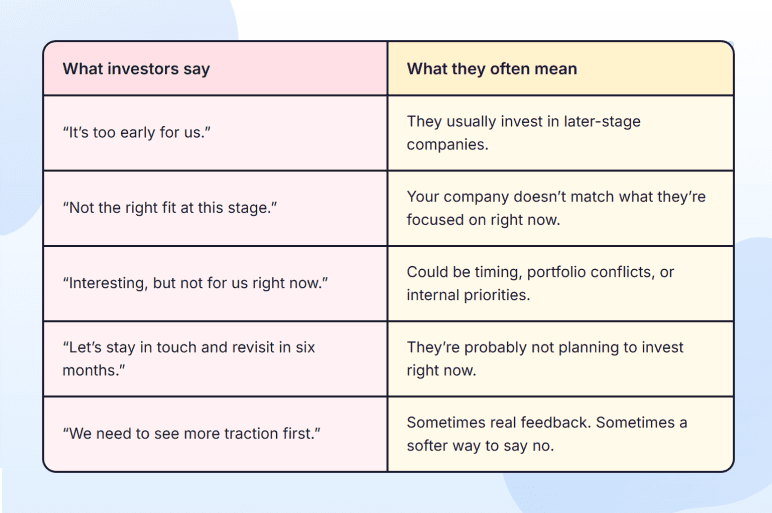

- “It’s too early for us.”

- “Not the right fit at this stage.”

- “Interesting, but not for us right now.”

- “Let’s stay in touch and revisit in six months.”

- “We need to see more traction first.”

Many people assume these comments explain the real reason. Most of the time, they aren’t.

In many cases, the polite explanation and the real reason are two different things:

And honestly, this makes sense from their side too.

Investors usually don’t want to damage relationships. You may raise a larger round later. Your company may grow into something much bigger. You may even introduce them to another founder in the future. So most investors avoid giving extremely direct feedback unless they really have to.

That means the explanation you receive is often meant to protect the relationship, not fully explain the decision.

What makes this even harder is how quickly many investors make up their minds.

DocSend’s pitch-deck research has consistently found that investors spend an average of 3 minutes and 44 seconds looking through a pitch deck before deciding whether they want to move forward.

And when they do evaluate a company, they tend to focus on a small set of signals. Harvard Business Review surveyed nearly 900 venture capitalists and found that investors place the most weight on things like:

- The team

- The market

- Traction

- Whether the company fits their investment focus

By the time the rejection email arrives a few days later, the real decision has usually already been made. The explanation in the email often comes after the decision, not before it.

Sometimes the rejection really is about the business. Maybe the market feels too small. Maybe traction isn’t strong enough yet. Maybe the investor doesn’t believe the timing is right.

But many rejections happen for reasons founders never see.

Here are some common examples:

| Structural reason | What it usually means |

| Stage mismatch | The fund invests in companies at a later stage. |

| Thesis mismatch | Your sector isn’t part of their current focus. |

| Portfolio conflict | They already invested in a similar company. |

| Fund timing | They’re near the end of their current fund cycle. |

| Partner bandwidth | The partner already works with too many companies. |

| LP (limited partners) pressure | Their investors pushed them toward different types of investments. |

From the founder’s side, these different types of rejection often look exactly the same in the email.

That’s why reacting too strongly to one rejection is a mistake. One investor “no” usually doesn’t tell you much by itself, no matter what reason they gave.

Your next pitch starts here

Build an investor-ready plan that holds up to tough questions

After the 24 hours: what to actually do (and not do)

It’s the next morning. You waited. The reply you wanted to send last night is probably not the reply you want to send now. That’s a good sign.

Now send a simple thank-you message.

This may sound small, but it matters more than most founders think. Investors remember how founders handle rejection. They talk to each other. They remember who stayed professional and who reacted emotionally. These relationships often last for years, not just one fundraising round.

Keep your reply short. Three sentences are enough. For example:

“Thanks for taking the time to meet and for the thoughtful pass. I really appreciated [one specific thing they said or asked]. I’d love to send you an update in about six months when we’ve hit [a specific milestone you’re working toward], and I hope we can stay in touch in the meantime.”

That’s it.

Don’t defend the business. Don’t re-pitch. And definitely don’t send a long message about how they misunderstood your market or unit economics.

If they misunderstood something important, fix it with progress, not arguments.

For example, instead of trying to convince them your market is big enough, send them an update six months later showing your user sign-ups grew by 20% or that customers are now paying consistently.

Your future results will explain it better than any other email ever could.

There are two common mistakes founders make after a rejection.

The first mistake: trying to reverse the no

No follow-up emails trying to reopen the conversation. No updates two weeks later, asking them to reconsider. The decision has already been made. Trying to change their mind immediately usually makes you look like someone who can’t accept signals or move on.

The second mistake: disappearing completely

A no today does not always mean no forever. The investor who passed in this round may invest later. They may introduce you to another investor. They may even lead a future round if the company grows in the right direction.

That’s why the six-month update matters. It keeps the relationship alive without forcing it.

Some founders eventually raise money from the same investors who passed the first time.

How to actually extract signal from rejection (without spiraling on a single no)

After a rejection, many founders fall into the same trap. They treat the rejection as a directive.

One investor says the market feels too small, so the founder spends the next week rebuilding the TAM (total addressable market) slide. Another says the team needs a technical co-founder, so the founder starts cold emailing CTOs. A third says the pricing is too aggressive, so the founder rewrites the pricing page.

A month later, the deck becomes a mix of conflicting feedback, and the founder’s own conviction starts disappearing.

Now every meeting starts with the question: “What will this investor want me to change?”

That’s a hard meeting to win, because you’re no longer pitching what you believe in. You’re pitching what you think other people want to hear.

The fix is to stop reacting to single data points. One no tells you almost nothing. The signal lives in the pattern across many no’s.

So keep a simple rejection log. For every no, write down four things:

- The date

- The investor’s name

- The pass reason in their exact words

- Whether you think it was structural (stage, thesis, fund timing) or business (market, traction, team, unit economics)

A note on your phone or a simple spreadsheet works fine.

Then wait until you have around 5 to 10 entries before drawing conclusions.

Less than five is usually just noise. Once the same concern starts showing up repeatedly, that’s when it becomes useful.

If the same concern appears in around 30% of your no’s, it’s worth looking into. If it shows up in 50%, it’s probably a real issue you need to address.

But one or two comments usually aren’t enough reason to change your strategy.

The “exact wording” part matters more than many founders realize.

Most people paraphrase feedback in their head, and when they do that, they lose useful context.

For example: “We’re not sure about TAM at the seed stage.”

That sounds like a market-size concern. But it may actually be a stage concern. The investor may simply think the company is too early for that kind of market discussion. The exact wording helps you tell the difference.

There’s also feedback you should mostly ignore:

- “Too early”

- “Not the right fit”

- Vague concerns

- Feedback that completely contradicts what other investors are saying

Those are usually polite passes or one-off opinions, not strong signals.

If you do ask for feedback after a rejection, these three questions usually lead to the most useful answers:

- “Was there anything specific that didn’t fit your fund’s current thesis?”

- “If you were in our shoes, what’s the one thing you’d want to see in six months?”

- “Who else should we be talking to?”

The third question is the most valuable.

Even if the investor doesn’t give detailed feedback, they almost always know other investors who are active in your space.

One no is a data point. Five no’s saying the same thing is the real signal.

When the no is about the pitch (and when it’s about the business)

Once you start seeing patterns across 5 to 10 rejections, the next question becomes harder: Is the problem the pitch, or is it the business itself?

Usually, the pattern tells you:

| What the pattern looks like | What it usually means | What to fix |

| Same concern shows up in 30%+ of no’s | Business issue | Traction, unit economics, team gaps, market size, customer proof |

| Different concern every time | Pitch or narrative issue | Story flow, first 60 seconds, ask, deck visuals, team slide |

If the problem is the pitch, start with the first 60 seconds. That’s where many investors make their first real judgment. If the opening is unclear, confusing, too detailed, or weak on conviction, the rest of the meeting becomes harder.

But if the problem is the business itself, accept that these fixes take time. You cannot solve weak traction, poor unit economics, or missing customer proof by redesigning slides.

Business-level problems usually take months to improve, not days. And that’s okay.

A lot of founders treat business-level changes like failure. They’re not. If multiple investors keep pointing to the same issue, sometimes the right response really is to change something important.

At the same time, don’t overreact to random feedback.

If three out of ten investors mention pricing, but the other seven all focus on different things, pricing may be worth thinking about, but it’s not a strong signal yet.

The worst thing you can do after a rejection is change the business based on one investor’s opinion.

Wait for the pattern before making major decisions.

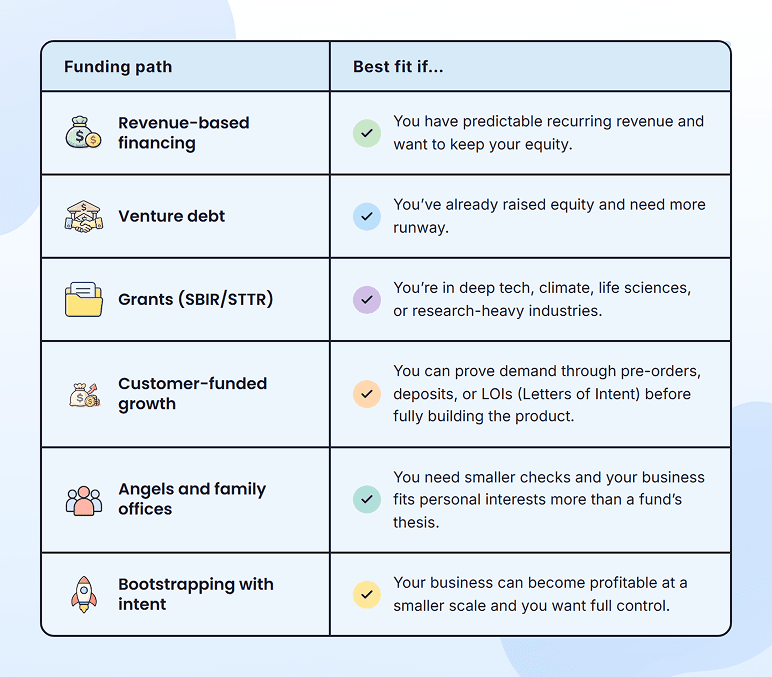

When to stop pitching this round and look elsewhere

Sometimes the pattern across many no’s is not telling you to fix the pitch or change the business. It’s telling you that you’re talking to the wrong type of investors.

Here’s a useful benchmark: if you’ve had 30 or more real investor conversations and the same structural concern keeps coming up (that the business isn’t venture-scale, or the growth shape doesn’t match your unit economics, or the timeline doesn’t fit a fund’s return horizon), the issue may not be the pitch or the company. It may be the type of capital you’re trying to raise.

Venture capital becomes the default path for many founders because it’s the most visible one. But VC only fits a certain type of business. Many good companies simply don’t match that model.

Here are some other paths worth considering:

These are not backup options.

Non-dilutive funding has grown quickly over the last few years. According to The Business Research Company’s report, revenue-based financing reached nearly $9.77 billion in market volume in 2025, and SBIR grants distribute more than $4 billion to founders every year.

The money exists. Many founders just don’t think beyond venture capital.

Changing funding paths is not a failure. It’s simply choosing the type of capital that fits the business you’re actually building.

Why I tell founders the early no’s are sometimes helping them

I know this sounds strange, but hear me out.

The wrong investor on the wrong terms can be worse than no investor at all.

- Maybe you give away too much equity at a low valuation and regret it later.

- Maybe you end up with board members you can’t remove, who want the company to go in a direction you no longer believe in.

- Maybe your terms make it harder to pivot because the investors backed the first version of the business and don’t want it to change.

- Maybe you get pushed to grow faster than the business realistically can, simply because the fund needs a certain outcome on a certain timeline.

The difficult part is that these problems usually don’t show up right away.

They show up a year or two later, when the business needs to change direction, and you no longer have the freedom to make that decision easily.

That’s why some early no’s are actually protecting you.

They protect your cap table, your board, and your flexibility. They filter out investors who may have said yes, but under terms you would eventually regret.

This is not the same as saying: “Every no is secretly a yes.”

That’s not true.

What I am saying is simpler: some of the no’s you’re hearing right now may actually save you from much bigger problems later.

Some yeses end up costing more than the no’s that came before them.

A better starting point: build a plan that earns the yes

The pitches that get to a fundable yes are usually backed by plans that took investor questions seriously before the investor asked.

A strong business plan forces you to think through the same things investors are going to test anyway. Unit economics that make sense before the market story does. Financial forecasts that hold up beyond the pitch. Competitive positioning that clearly explains who you’re really competing against, not just the obvious names in the market.

Founders who do this work before fundraising walk into meetings differently. The pitch becomes a presentation of what they already understand, not a defense of what they hope is true.

That’s what we built Upmetrics to help with: a guided business planning platform that helps founders build financial forecasts, understand unit economics, and create business plans that stand up to investor questions.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

Is it appropriate to ask why an investor passed?

How many investor rejections is normal before you raise a round?

Can an investor who rejected me become a yes later?

Should I share investor rejections with my team?

When should I stop pitching VCs and consider other funding paths?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more