There are moments in running a business when the amount of money in the bank account no longer feels reassuring.

- Revenue may be inconsistent from month to month,

- Costs often continue to rise regardless of performance,

- And decisions like hiring or cutting expenses start getting delayed

Because there is no clear sense of timing. The real problem here isn’t how much cash is available, it’s how long that will last given current scenarios.

Without that clarity, every financial decision becomes reactive, driven more by pressure than by planning.

Your cash runway is the single most important metric here.

It helps you translate available cash and ongoing expenses into a simple measure of time, and allows you to understand how many months the business can continue operating before additional revenue or funding is required.

Let me show you how to calculate your cash runway today.

What is a cash runway? (Don’t confuse it with burn rate)

I just explained this: a cash runway means how long your business can keep operating before it runs out of cash, assuming money keeps coming in and going out at the current pace.

For example, if the cash you have on hand (cash on hand: money you can use today) can cover your costs for the next eight months, that means you have eight months of runway.

People often mix this up with burn rate, but they’re not the same thing. Burn rate is how fast you’re spending cash, shown as a dollar amount per month.

They’re definitely related, but not the same.

The easiest way to understand the distinction? Burn rate is the speed at which you’re spending, and runway is how much time that speed leaves you.

The cash runway formula (& the inputs that actually matter)

That speed-and-time relationship is exactly what the cash runway formula helps you measure.

If burn rate shows how quickly your business is using cash, runway shows how long your available cash can support that pace. So when you calculate runway, you’re simply asking: If cash keeps moving in and out like this, how many months do we have before the money runs out?

Here’s the formula for that:

The math is simple. But the number can still be wrong if you use the wrong inputs.

For the cash side, use only the money your business can spend today, as discussed earlier. If it is still expected to come (restricted or not reached in the account yet), don’t count that.

For the burn side, be a bit more careful. Spending alone doesn’t always show the full picture, especially if the business is still bringing in revenue every month.

So you need to look at the two sides of the burn rate:

- Gross burn is the total cash your business spends in a month.

- Net burn is the cash gap after subtracting collected revenue from monthly spending.

For example, if your business spends $80,000 in a month and collects $30,000 from customers, your gross burn is $80,000, and your net burn is $50,000.

That $50,000 is the number that shows how much your cash balance actually dropped that month.

If revenue is steady and collected on time, net burn usually gives you a more useful runway number. But if you are pre-revenue or revenue is unpredictable, gross burn gives you a safer view because it does not assume money will keep coming in.

So don’t use the number that makes your runway look better. Use the number that gives you the clearer picture.

How to calculate the cash runway? (with example)

I know the formula itself is simple. You can calculate runway in a few seconds: divide cash by burn rate, and you have a number.

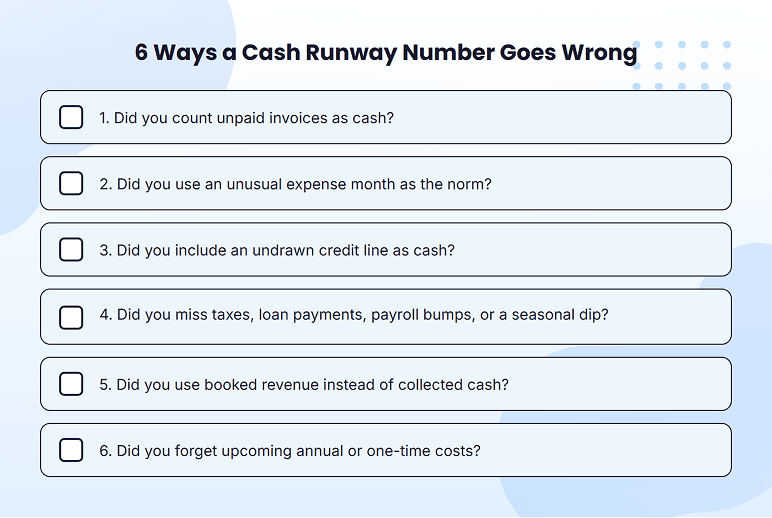

But that number is only useful if the inputs are right. That’s where the calculation often goes wrong. You might count money you can’t use yet, use one unusual month as normal, or count revenue before the cash is collected.

So let me walk you through three quick steps, using a simple coffee shop example, that make sure you get a number that reflects your real cash position.

Step 1: Estimate your usable cash

Start with the money your business can spend today. This usually includes your checking balance, savings account, reserve account, or loan money that has already landed in your account.

Do not subtract upcoming bills here. Those will show up when you calculate burn.

For example, the coffee shop has $28,000 in checking and $12,000 in savings, so its usable cash is:

$28,000 + $12,000 = $40,000

The shop also has a $6,000 unpaid customer invoice and a $10,000 unused credit line, but neither goes into the runway calculation. The invoice has not been collected yet, and the credit line is not cash until it is drawn.

So the cash number for the formula is $40,000.

Step 2: Find your average monthly burn

Next, figure out how much cash the business loses in a normal month.

Add up the cash that goes out for rent, payroll, supplies, utilities, taxes, loan payments, software, contractors, and other operating costs. Then subtract the cash you actually collected from customers. The gap is your net burn.

Use collected revenue, not invoiced revenue. An unpaid sale does not help your cash yet. I’d also avoid using one unusual month as your burn number. A large one-time purchase or annual bill can make burn look higher than normal, so a recent three-month average gives you a cleaner number.

For the coffee shop, about $38,000 goes out in a normal month for rent, wages, supplies, utilities, taxes, and loan payments. It collects about $32,000 from sales.

So its monthly net burn is:

$38,000 – $32,000 = $6,000

Step 3: Divide cash by the monthly burn

Now divide usable cash by monthly burn.

For the coffee shop, that means:

$40,000 ÷ $6,000 = 6.7 months of runway

So at its current pace, the coffee shop has a little under seven months before cash runs out.

That number helps the owner make real decisions: whether to hire a third barista, delay a second location, reduce costs, or push catering sales harder to close the gap.

But the runway is still a snapshot. It changes when sales slow down, a customer pays late, expenses rise, or the owner adds a new hire. So write the number down with the date and recalculate it each month. The trend tells you more than one reading.

And the cash flow forecast takes it one step further by showing how upcoming revenue, expenses, debt payments, and delayed collections could change your runway before they hit the bank account.

What is a good cash runway?

There is no single “good” cash runway number. A stable small business, a seasonal shop, a bootstrapped startup, and a funded company all need different cash buffers.

A good runway depends on how predictable your cash flow is, how fixed your expenses are, and whether you’re planning a major move like hiring, expansion, or fundraising.

Here’s what that looks like by business type:

| Business type | Practical runway target | Why |

| Stable small business | 3–6 months | Covers slower sales, late payments, and surprise costs |

| Bootstrapped growing business | 6–12 months | Room to grow without leaning on outside funding |

| Pre-revenue or pre-seed startup | 12–18 months | Gives time to build, test, and reach early traction |

| Seed to Series A startup planning a raise | 18–24 months | Gives time to hit milestones and start fundraising early |

| Funded startup in a slower funding market | 24+ months | Gives more room if the next round takes longer |

| Seasonal business | Slow season + buffer | Covers the months when cash inflow drops |

Use these as planning ranges, not fixed rules. A business with steady sales and low monthly costs may not need as much runway.

But if your cash flow changes month to month because of payroll, inventory, debt payments, slow-paying customers, or seasonal sales, you’ll need more room than a business that gets paid at the time of sale.

What does your runway number actually tell you?

Once you compare your runway against a practical range, you can see whether it feels short, normal, or comfortable for your situation. But the number becomes more useful when you connect it to your next decision.

- Can you afford to hire now?

- Should marketing spend stay where it is?

- Do you need to follow up harder on receivables?

- Is it time to delay a purchase or start funding conversations?

Still, one number is only a snapshot. The direction it moves matters more because it shows whether the business is gaining room or getting tighter.

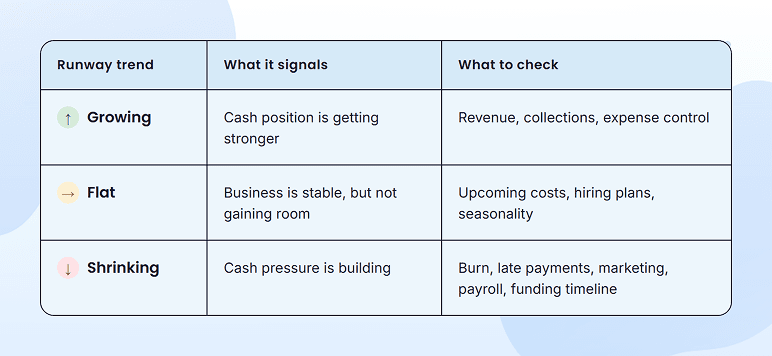

If your runway is growing, your cash position is getting stronger. Check what’s behind it. Better revenue, faster collections, or tighter spending are good signs. Delayed bills or cuts that hurt the business are not.

If your runway is flat, the business is stable but not gaining much ground. Look ahead before making new commitments. A hire, renewal, loan payment, or seasonal dip can quickly turn flat into shrinking.

If your runway is shrinking, cash pressure is building. Start with the numbers that move fastest: burn rate, late payments, marketing spend, payroll, and funding timeline. Then check whether spending is growing faster than cash coming in.

Here’s what your runway trend is telling you:

Paul Graham’s default alive vs default dead idea is also useful here. Ask: if you keep your current cash, burn, and revenue trend, will the business reach break-even before cash runs out?

If yes, you’re default alive. If no, you’re default dead, which simply means the current path needs to change through revenue, expenses, funding, or payment timing.

So the real question is not only “How many months do I have?” It is: do you have enough room to keep going as planned, or do you need to extend your runway while you still have options?

How to extend your cash runway?

If your runway is shorter than you expected, the first question is usually the obvious one: Can I fix this?

Most of the time, yes. But the answer isn’t to start cutting costs randomly. A short or shrinking runway just means you need to find out what is putting pressure on your cash. And your job is to find what, then pick the right fix.

Sometimes the problem is real: money is going out faster than it’s coming in. Other times, the runway only looks bad because the calculation is off.

So before you change anything around spending, hiring, or funding, check the number first. A low runway is often a calculation mistake, not a real emergency. Then look for the usual mistakes:

If the number is off, you might be fixing a problem you don’t have. If it holds up, start with the moves that protect cash without hurting the business, starting with the changes that add time every month, not just once.

Reduce or delay expenses

Start with spending that can be stopped or delayed without affecting customers or revenue. That could be unused software, non-urgent projects, weak ad campaigns, events, travel, or contractor work that can wait.

Don’t cut blindly. If a tool, person, or campaign is helping you bring in or keep revenue, cutting it may make the runway problem worse.

Avoid new monthly commitments

When the runway is tight, be careful what you commit to next. Delay a hire, hold off on a big purchase, or renegotiate a contract before you renew it.

The point isn’t to stop growing the business. It’s to avoid signing up for costs you may not be able to carry yet.

Improve the cash coming in

Here’s what works here: follow up on overdue invoices, ask for deposits on larger projects, shorten payment terms, or offer annual prepay where it fits. For a service business, even shifting from “paid on completion” to “half upfront” can take pressure off.

You can also raise prices or grow revenue from existing customers. Those moves last longer than one-time collections, but don’t count the money until it’s actually in the account.

Use funding carefully

Funding only works if it fixes a real issue (not if it hides one). It makes sense when the business is healthy and just needs more time to reach the next milestone.

But it doesn’t help when the problem is thin margins, slow collections, or overspending, because then you’re borrowing time to repeat the same mistake.

And before selling equity, look at non-dilutive options like a line of credit or revenue-based financing first. They give you time without giving up ownership.

The best fix, though, is seeing the problem before it arrives. A simple cash flow forecast shows you a tight runway months ahead, while you still have easy options instead of hard ones.

Track your cash runway over time

Calculating your runway once gives you a useful starting point. It tells you how many months the business has if cash keeps moving the way it does today.

But don’t treat it as a one-time calculation. Your runway changes every time the business changes. A new hire, delayed customer payment, large expense, funding round, or marketing increase can all shift the number.

So track it monthly, and use a cash flow forecast to look ahead, not just back at what already happened. That’s where Upmetrics can help. You can add your cash, revenue, expenses, loans, and planned spending, then see how future decisions may change your runway before you make them.

Calculate your runway, track it regularly, and plan your next move while there’s still time to adjust.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

How do I calculate the runway if my revenue is growing fast?

What's the difference between a cash runway and an operating runway?

How do investors look at my runway during diligence?

My runway just dropped 6 months, should I panic?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more