Writing a business plan sounds like the easy part of starting a business. You already know your idea, your product, roughly who you’re selling to, and how you plan to make money. But oftentimes when you open a blank doc, none of it comes out right.

Figuring out how to write a business plan isn’t really about the writing. It’s about turning what’s in your head into something a lender, investor, or partner can read and take seriously.

Which section comes first? How much detail is too much? What numbers do you include, and how do you keep them from sounding like guesses?

I’ll go section by section, show you what belongs in each part, how much to write before you’re overdoing it, and how the numbers connect. Whether you’re applying for an SBA loan, pitching investors, launching a new venture, or just trying to think through your business more clearly, you’ll finish with a plan that holds up.

First, choose the right business plan format

Even before you write the “perfect plan,” you have to choose the perfect format, because that’s half the work. Okay, that might be an exaggeration, but the format you pick decides how much you write, what you spend time on, and whether the person reading it takes you seriously.

There are three formats you should know about:

| Format | Length | Best for | Time taken to write | Who is it for (audience) |

| Traditional | 20-40 pages | SBA loans, bank financing, equity raises | 2-4 weeks | Lenders, investors, formal partners |

| Lean | 5-10 pages | Internal clarity, fast iteration, early-stage validation | 3-5 days | You, your co-founder, and advisors |

| One-page | 1 page | Quick alignment, partner pitches, MVP stage | A few hours | Partners, friendly investors, and yourself |

If you’re still on the fence, let me put it this way.

If you’re writing for funding, go traditional. That’s what lenders and serious investors expect, and there’s no real way around it. Even then, I’d draft a lean version first. By the time you sit down to write the traditional plan, half the thinking is already done.

A one-page format works for early partner conversations or MVP-stage alignment. For anything else, traditional or lean is the safer call.

Format is only half the decision. What you’re writing for changes what you emphasize. For lenders, consider cash flow, projections, collateral, and use of funds. For investors, consider market size, traction, growth potential, and team. For internal use, weight goals, operations, and milestones.

Once that’s clear, you can start writing the actual plan.

How to write a business plan step by step

Before you open a doc, spend an hour pulling your inputs together. It’s the single easiest way to avoid stopping mid-section to hunt for a stat or a number.

Have these ready:

- Market data for your industry and location (reports, census figures, trade association stats)

- A shortlist of 5-7 competitors with notes on pricing and positioning

- Your numbers, that includes pricing, unit costs, monthly expenses, and sales assumptions

- Team info consisting of short bios and the roles you plan to hire for

- The basics, including entity type, licenses, key suppliers, and any existing traction

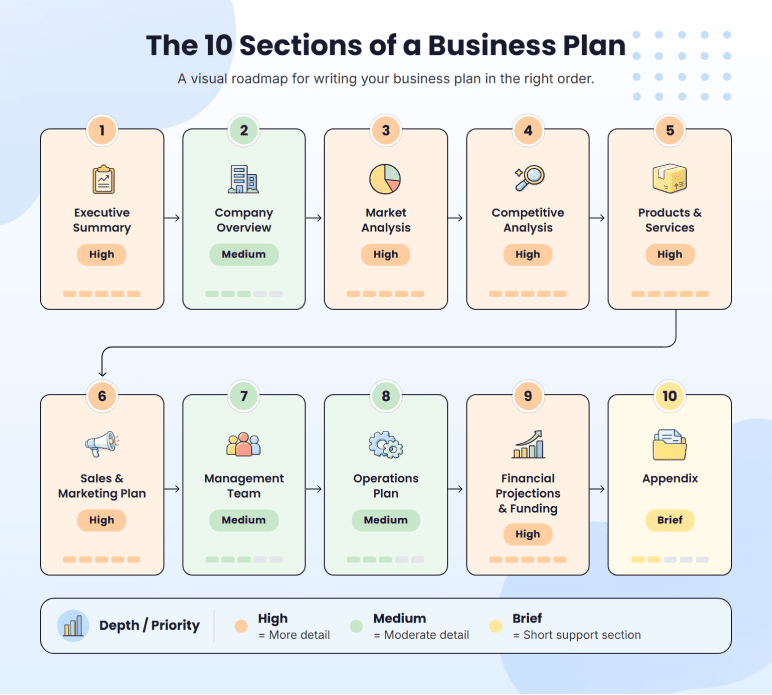

Some sections are more factual, while others require research, assumptions, and defensible numbers. Either way, the thinking part is covered. I’ve walked through what you need inside each step.

Step 1: Executive summary

An executive summary is basically a short version of your whole business plan. It’s the first section someone sees when they open your plan, but it should be the last one you write. It kinda makes sense if you think about it. You can’t really summarize something you haven’t written yet, right?

Even if you’re writing it last, this is the first thing a lender or investor reads. A lot of times, it’s the only thing they read before deciding if they want to keep going. So everything important should be visible right there.

Keep it simple and cover these things:

- What your business is, where it’s based, and what you do

- The problem you’re solving and who has that problem

- Your solution and what makes it different from what’s already out there

- The market you’re going after and a rough sense of how big it is

- Where you are today, like how much you’ve sold or how many customers you have

- What you’re asking for, whether that’s money, a partnership, or a sign-off

- Description of your team and why you’re the right people to do this

As for length, keep the executive summary to one page if you can. For a longer, lender-ready plan, two pages are acceptable, but only if the extra space is doing real work.

If you want a fuller breakdown with examples, we have a separate guide on how to write an executive summary that you can dig into.

Step 2: Company overview

A lender who reads 40 plans a month uses the company overview to categorize your business. Retail or service? LLC or sole prop? Pre-revenue or operating? Once they’ve placed you in a bucket, they know which underwriting framework to apply.

That’s the job of this section.

Cover these five things:

- Business name, location, and start date (or planned start)

- Legal structure: LLC, S-corp, C-corp, or sole proprietorship

- Mission and vision, one line each

- Business model: how the money actually comes in

- Where do you plan to be in one year, and in five years

The mission and vision in this section can be confusing when writing this section. Compare these two:

“To revolutionize the coffee industry by delivering exceptional experiences that empower communities and inspire connection.”

“To be the go-to morning stop for downtown Eugene commuters by serving locally roasted coffee in under 90 seconds.”

The second one is a mission that a lender can hold you to with a specific customer, location, and promise. The first could belong to any coffee brand on the planet.

Step 3: Market analysis

A lender’s first instinct on this section is skepticism. So your job here is to show you’ve actually looked at the market that matters to your business. That means writing about your target customer (who they are, what they spend on, what problem they’re paying to solve), sizing the market in three layers instead of one, naming two or three real trends with sources, and calling out any regulations that affect how you operate.

Most first-timers reach for the biggest number they can find, which is obviously something you should avoid. Be specific: your TAM is everyone who could buy this kind of product, your SAM is the portion you can realistically reach given your location, channel, price, or business model, and your year-one target is the small piece of SAM you expect to capture in the first 12 to 24 months.

For data, the U.S. Census Bureau, IBISWorld, and Statista are good starting points. Pew Research is also useful for consumer behavior, and trade associations in your industry often publish reports that go deeper than national-level stats.

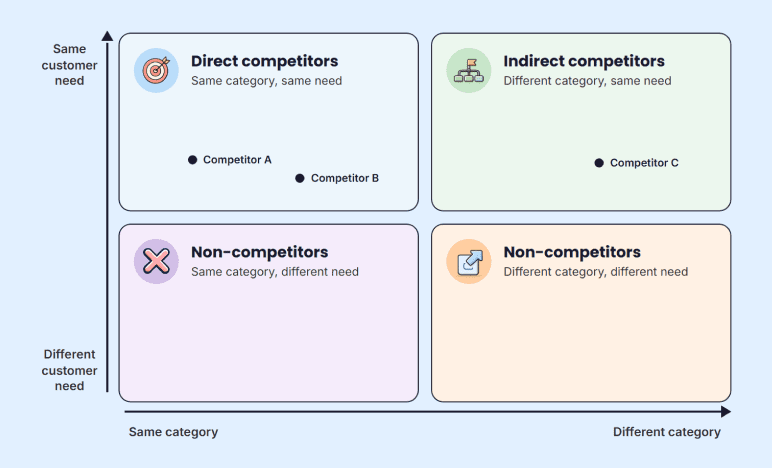

Step 4: Competitive analysis

Most first-timers write this section defensively. They list two or three competitors, say something vague about how their business is “different,” and move to the next section. If you can’t name who you’re up against, they’ll assume you haven’t looked hard enough to know.

Cover four things: three to five direct competitors and what they do well, two or three indirect competitors that could pull the same customer away, a SWOT comparing your business to theirs, and one or two real reasons a customer would pick you.

The differentiation piece is the most important part of this section. So make sure whatever you put in there is a real, defensible reason a customer would pick you over someone bigger, cheaper, or already established.

If you want a deeper walkthrough of how to research and structure this section, we have a separate guide on how to write a competitive analysis that you can dig into.

Step 5: Products and services

Write this section for a stranger. Someone who has never heard of your business, your industry, or the pain point you’re solving.

Cover five things:

- What you’re selling in plain language

- The problem it solves

- Your pricing

- How you arrived at it,

- How the customer actually receives the product from order to delivery

- How do you keep the experience consistent as you grow?

The founders who write this section well, apart from just describing their product, also describe what it replaces. That’s the real switch you’re asking a customer to make, and it forces you to write from the customer’s side of the table.

Step 6: Sales and marketing plan

This is the section where you have to lay out how people turn into paying customers. It’s a bit tricky to write this one, partly because marketing feels like it could include everything, and partly because no one wants to commit on paper to a specific channel and risk being wrong.

So pick two or three channels you can realistically run. If you’re a fashion brand, that’s probably some mix of paid social, influencer, UGC, and email. If you’re B2B, it’s probably outbound, content, and referrals. Whatever it is, write down why you picked those over the ten others available.

Hit these points:

- One sentence on what you stand for and who it’s for

- The channels you’ll use and why those over others

- How someone moves from first hearing about you to buying

- Your expected customer acquisition cost, based on planned channel spend, expected leads, and estimated conversions

- Your sales process, if you have one, especially for B2B or higher-ticket products

Write down the assumption you’re working with and how you’d test it in the first three months. A number with a clear assumption is more credible than no number at all.

If you don’t have CAC data yet, start with an assumption. For example, if you plan to spend $1,000 on local ads and expect 100 first-time customers from it, your estimated CAC is $10. Then explain how you’ll test that assumption in the first 60-90 days.

Step 7: Management team

If a plan’s numbers look shaky, the team section can still save it. If the team looks shaky, no numbers will save it. That’s the weight this section carries.

When writing for the first time, it’s common to write full LinkedIn bios for every person on the team. A lender only needs to learn why you specifically are the right person to pull this off.

So for each person, write one short paragraph covering their background, the specific experience that maps to what you’re building, and their role in the business. That’s it. Another important thing here is if your team has obvious gaps, add those details too.

Step 8: Operations plan

This section should only include operational details that affect delivery, cost, quality, capacity, timeline, or risk.

Cover your key suppliers and any backups if a primary one falls through, the tools and software you rely on to run the business, how a product gets made and delivered end-to-end, your location (office, warehouse, retail, or remote), your production or service capacity before you need to scale, and how you keep quality consistent as volume grows.

If you’re running a software or service business, keep this section light. A few lines on tools and workflow are enough. If you’re in retail, food, or manufacturing, this is where a lender will spend real time, so give it the depth it deserves.

Step 9: Financial projections and funding request

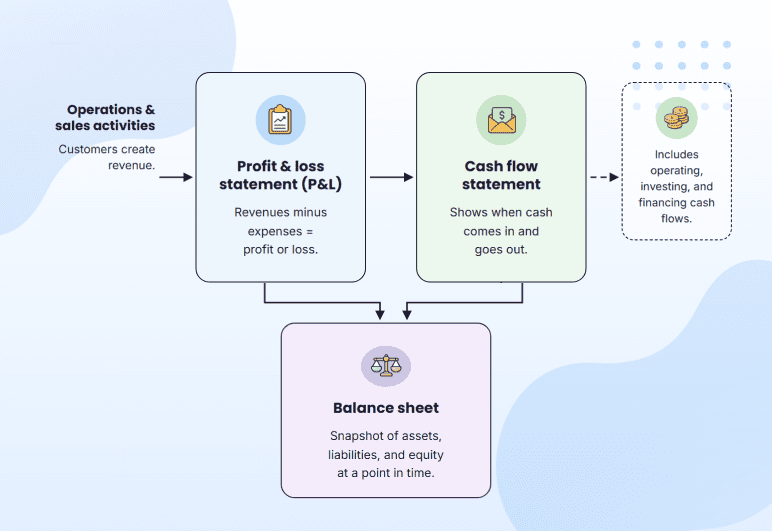

If you ask a lender what they read first, most of them will say the numbers because the numbers tell them if the story is possible.

Your financial projections are estimates, and they’ll never be exact. What matters is that every number ties back to an assumption a lender can check.

Build your financials bottom-up. Start with what you can estimate directly: units sold, price, frequency, and cost to deliver. From there, your sales forecast, expenses, profit, and cash flow all connect.

At a minimum, your financials should include:

- A monthly sales forecast for year one and annual figures for years two and three

- An expense budget covering rent, payroll, marketing, inventory, and software

- A profit and loss statement

- A cash flow statement, because a profitable business can still run out of money

- A balance sheet, providing a snapshot of your assets, liabilities, and equity

- An assumptions log tying every number to something real

The funding request

If you’re raising money, don’t leave the ask as one loose sentence. State how much you need, what you’ll use it for, and how it maps to your projections.

A coffee shop asking for $60,000 might allocate $25,000 for equipment, $8,000 for opening inventory, $7,000 for launch marketing, and $20,000 for working capital.

The

Build lender-ready financial projections with AI

SBA’s guide to writing your business plan is a solid reference for how lenders expect a funding request to be structured.

Step 10: Appendix

The appendix is where anything that supports a claim in the main plan but would slow down the read goes. A lender who wants to verify your numbers or check your credentials should find the evidence here without having to ask for it.

The easiest way to build it is backwards. Go through the plan section by section and note anything a careful reader might want proof of. Then collect those items into one labeled, indexed section at the end.

Common appendix items include:

- Founder and team resumes

- Business licenses, permits, and registrations

- Supplier and vendor quotes for equipment, inventory, or services referenced in your operations plan

- Lease agreements or letters of intent for your business location

- Product photos, prototypes, or design mockups

- Detailed market research reports or survey data you referenced but didn’t include in full

- Full financial worksheets, including monthly line-item projections that were summarized in the main plan

- Legal documents like partnership agreements, incorporation paperwork, or IP filings

- Letters of intent from customers, partners, or investors that show early traction

- Insurance policies, if applicable to your business type

Order the items in the sequence they show up in the main plan, and label each one clearly.

So that’s the 10 sections.

If you want to see what a finished business plan looks like with everything put together, you can browse business plan samples on Upmetrics. Each one shows the full structure across all 10 sections, so you can see how the writing, formatting, and numbers come together on paper.

Now, before you send your plan to anyone, run it through one more filter.

The investor checklist: will your plan survive scrutiny?

Once the plan is done, read it like someone who owes you nothing. A lender or investor may have 20 plans on their desk and only 15 minutes to decide whether yours deserves a second look.

These are the questions they’ll ask:

On the market

- Is the opportunity real, or does it only look big because you sized it generously?

- Why now? What’s changing that makes this the right moment to build this?

On the model

- Do you make money per customer after the cost of getting them?

- Can you defend your pricing against what it costs you to deliver?

On the team

- Why you, specifically? What’s the experience that makes you the right person for this?

- What gaps are in the team right now, and what’s the plan to fill them?

On the money

- Is every number tied to an assumption someone could check?

- If you’re asking for funding, is the use of funds clear and broken down by category?

On the risk

- What are the two or three things most likely to go wrong, and what’s your response to each?

- Is there a single supplier, channel, or customer that the whole business depends on?

I must warn you here that no matter how hard you try to read your plan like a stranger would, the bias will creep in. You wrote it, and you know what you meant, so your brain will most likely fill in the things that aren’t actually on the page. That’s just how it works. But you don’t have to do this part entirely on your own anymore.

How AI can help you write and review your business plan

For me, AI is most useful at the two ends of the writing process. Right at the start, when you don’t know how to begin. And right at the end, when you’ve read your own draft so many times, it stops making sense.

I’ve listed four important ways you can use AI:

- For your first draft, feed it your notes and get a structured first pass back in seconds.

- For a proper review, paste your finished section back in and ask it to flag weak spots, thin logic, or numbers that don’t tie.

- For research purposes, use it to surface competitors you missed or pull benchmarks for your assumptions.

- For stress testing, ask it to read your plan like a skeptical investor and call out the gaps.

AI, no doubt, can do a lot of things. But what AI can’t do is the actual thinking. It can’t tell you what your customer wants, why your business will work, or how to split your raise. So as for the thinking part, it’s on you.

If you’re using AI, use a tool that comes close to making your thinking sharper and is built for business planning. That’s the gap we tried to close with Upmetrics. It handles the structure, the section prompts, and the financials, so you can spend your time on the parts only you can do.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

Can I write a business plan myself?

How long should a business plan be?

Is a pitch deck the same as a business plan?

What are the 3 C's of a business plan?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more