Thousands of small businesses change ownership each year, with additional off-market transfers not captured in public data. So the real number is larger! But how are people buying these businesses when the purchase price is often the biggest hurdle?

You got it. SBA loans.

An SBA loan can cover up to 90% financing, while a buyer only puts as little as ~10% down. A very practical solution, A lot of people are unaware that these loans are, in fact, for buying existing businesses.

That’s great news, isn’t it? But how can you get an SBA loan to buy a business? Where to apply? How soon can you expect it?

We cover it all below. Let’s begin, shall we?

SBA loan to buy a business: SBA 7(a) vs. SBA 504

For most business acquisitions, the SBA 7(a) is your go-to loan. But if the deal includes a building or heavy equipment, the SBA 504 might save you money, or work alongside a 7(a) to cover different parts of the deal. Here’s how to tell the difference:

The SBA 7(a) loan

This is the most flexible SBA loan and the most common way to finance a business purchase. You can borrow up to $5 million, and the loan can cover almost everything involved in a typical acquisition: goodwill, inventory, working capital, equipment, and intangibles like customer lists and brand value.

For most business purchases, the loan term is 10 years. The rate is variable, calculated as the Prime Rate plus a lender spread, and the SBA caps based on loan size. For acquisition loans over $350,000 (which describes most deals), the current rate runs approximately 9.00%–9.75%, based on the Prime Rate of 6.75% as of March 2026. Well-qualified buyers with strong credit and financials typically land closer to the lower end.

The SBA guarantees 75%–85% of the loan, depending on the loan amount. This guarantee is what makes lenders willing to finance deals they’d otherwise pass on, particularly those involving large goodwill components or limited hard collateral.

The SBA 504 loan

The 504 is built for deals that include commercial real estate or major equipment. It’s structured in three layers: the bank covers 50%, a Certified Development Company (CDC) covers 40% with a fixed, SBA-backed rate, and you put in 10%. The fixed rate on the CDC portion currently runs approximately 5.67%–5.91%. That’s lower than a 7(a), which is the appeal.

The catch: the 504 cannot cover goodwill, working capital, or intangibles. For any deal that includes those (and most small business acquisitions do), you’ll need a 7(a) for that portion. A common approach for asset-heavy deals is to use a 504 for the real estate and a 7(a) for the goodwill and working capital. The fixed rate on the CDC portion runs approximately 5.67%–5.91% based on current NADCO debenture pricing. Lower than a 7(a), which is the appeal.

| Feature | SBA 7(a) | SBA 504 |

|---|---|---|

| Max loan amount | $5 million | $5.5 million (CDC portion) |

| Down payment | As low as 10% | As low as 10% |

| Loan term | Up to 10 years (business purchase) | Up to 25 years (real estate) |

| Rate type | Variable (Prime + spread) | Fixed (CDC portion) |

| Current rate range | ~9.00%–9.75% (loans over $350K) | ~5.67%–5.91% (CDC portion, NADCO pricing) |

| What it covers | Goodwill, inventory, working capital, equipment, intangibles | Commercial real estate, major equipment |

| What it can’t cover | Nothing. Highly flexible | Goodwill, working capital, intangibles |

| Best for | Most acquisitions, especially service businesses | Asset-heavy deals with real estate or large equipment |

The decision rule: If your deal is mostly goodwill (a consulting firm, franchise, cleaning service, digital agency), use the 7(a) only. If you’re buying a business that includes a building or $500,000+ in equipment, run the 504 numbers. The fixed rate and longer term can reduce your monthly payment meaningfully.

What you need to qualify for an SBA loan to buy a business

SBA loans aren’t handed out freely, but they’re not as hard to get as most people assume. Lenders are checking seven things (requirements). Know what each one means, and you’ll walk into that conversation prepared instead of nervous.

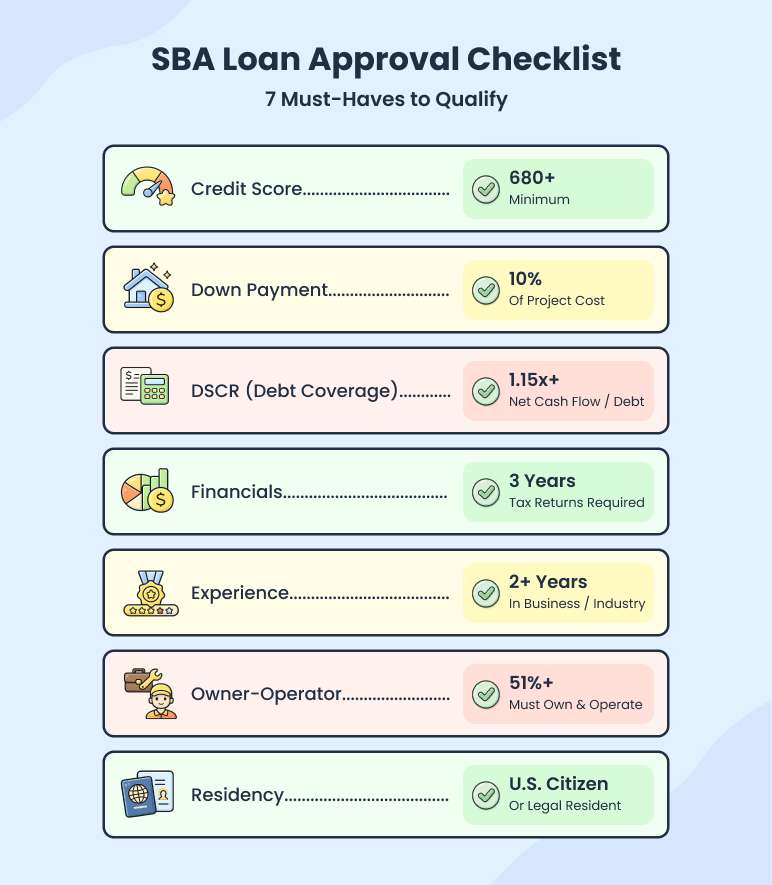

1) Credit score

Most SBA lenders want to see 680 or above. Below 650, your approval odds drop significantly. Not because of a hard program rule, but because lenders use it as a proxy for repayment reliability.

A past bankruptcy isn’t an automatic disqualification. If it’s been 5 or more years and your credit has recovered, lenders will consider the full picture. Recent late payments and delinquent federal debts hurt more than a few points below 680.

2) Down payment (equity injection)

The minimum is 10% of the total purchase price. On a $500,000 business, that’s $50,000.

Here’s the part most people miss: that 10% doesn’t have to come entirely from your own savings. Up to half of it can come from a seller’s note. At a minimum, 5% must come directly from you. Cash, a documented gift from a family member, or retirement funds rolled over through a ROBS (Rollover for Business Startups) arrangement. The remaining 5% can be covered by the seller carrying a note on standby.

3) Debt service coverage ratio (DSCR)

This is the number lenders care most about. Your DSCR needs to be at least 1.15x to 1.25x, meaning the business generates $1.15 to $1.25 in net cash flow for every $1.00 in loan payments.

In practice, if your monthly loan payment is $5,000, the business needs to produce at least $5,750 to $6,250/month in net cash flow after operating expenses. Run this math before you fall in love with any business.

4) Business financials

Lenders want 3 years of business tax returns and profit and loss statements. The business should show stable or growing revenue and consistent profitability.

A business with one strong year sandwiched between two weak ones will raise questions. Lenders are looking for a trend, not a single good year.

5) Management experience

You don’t need to have owned a business before. You do need relevant industry or management experience that makes a lender confident you can run this specific business.

If you’re buying a landscaping company, prior landscaping or field operations experience matters. If you’re buying a medical practice, a clinical or healthcare management background carries weight. The closer your background is to the business, the easier this conversation becomes.

6) Owner-operator requirement

SBA loans aren’t for passive investors. You must plan to actively manage the business day-to-day. If your plan is to hire a manager and stay hands-off, you won’t qualify.

This is also why the management section of your business plan matters. Lenders want to see that you’re the one running this.

7) US citizenship or permanent residency

You must be a US citizen or a lawful permanent resident. There are no workarounds here. It’s a program requirement, not a lender preference.

Not sure where to start with your acquisition plan?

Build a lender-ready business plan before you apply

How to get an SBA loan to buy a business (7 guided steps)

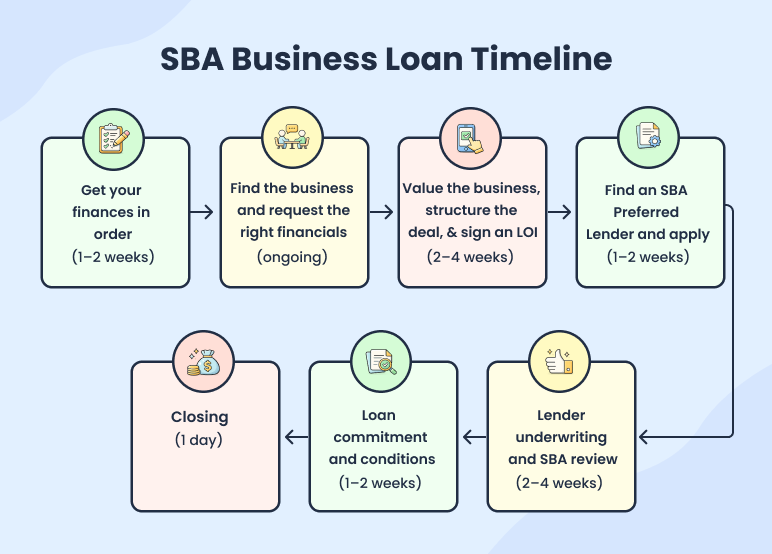

Getting an SBA loan for a business purchase is a process, not an event. From the moment you start getting your finances in order to the day funds hit the seller’s account, you’re looking at 45 to 90 days—sometimes less if you’re prepared, sometimes more if you’re not. Here’s exactly what happens, in the order it happens.

Step 1: Get your finances in order (1–2 weeks before you start shopping)

Before you look at a single listing, get your own house in order. Pull your credit report from all 3 bureaus and dispute anything inaccurate. Pay down any revolving balances you can. Gather 3 years of personal tax returns. Put together a personal financial statement. By that, I mean a clean summary of your assets, liabilities, and net worth.

Lenders will ask for all of this eventually. Having it ready on day 1 signals that you’re a serious buyer and cuts weeks off your timeline later.

Step 2: Find the business and request the right financials (ongoing)

Finding the right acquisition target runs in parallel with getting your own finances in order. You can source deals through business brokers (who are paid by the seller, making their service free to you), public marketplaces like BizBuySell and BizQuest, or direct outreach to owners in your target industry. Off-market deals found through direct outreach often come with less competition and more motivated sellers.

Once you find a business worth exploring, the very first thing you do is sign an NDA. Do not ask for financial details before it’s signed. Once the NDA is in place, request exactly three things:

- Three years of business tax returns

- Three years of profit and loss (P&L) statements

- Confirmation that the current owner is willing to fully exit, or step back to a limited consulting role (the SBA does not allow sellers to remain as owners or key officers)

If the seller hesitates on any of these, walk away. You cannot get an SBA loan without them.

Step 3: Value the business, structure the deal, and sign an LOI (2–4 weeks)

Once you have the financials, you need to answer two questions before you go any further: what is this business actually worth, and how will the money come together at closing?

Valuing the business

There are three methods lenders use, and the right one depends on the deal. For most small business acquisitions, the SDE multiple method is what you’ll encounter. SDE is the business’s net profit added back with the owner’s salary, benefits, and any personal expenses run through the business. It reflects what a new owner-operator could actually expect to earn. Service businesses typically sell at 2x–3x SDE; manufacturing businesses command 2.5x–4x, depending on equipment condition, customer concentration, and revenue stability.

For asset-heavy businesses, lenders use asset-based valuation — tangible assets valued at liquidation or replacement cost. For businesses with available market data, comparable sales (what similar businesses sold for recently) provide a useful cross-check.

One practical note: for deals with goodwill over $250,000, the lender may require an independent third-party appraisal. Budget $3,000 to $5,000 and an extra week or two in your timeline.

Structuring the deal

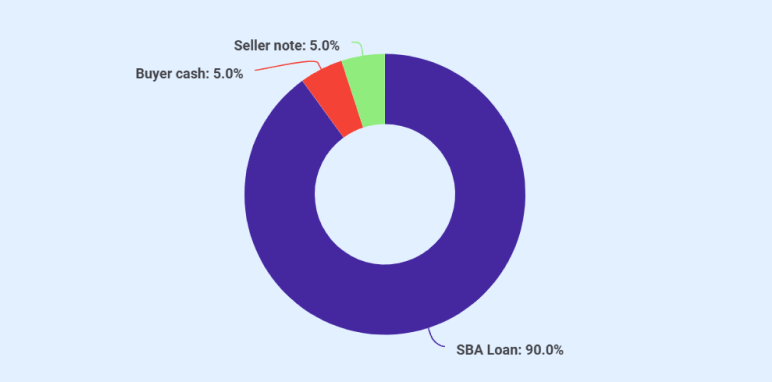

Most people think of an SBA acquisition as two parts: the loan and the down payment. In practice, there are often three: the bank loan, your cash, and a seller note. Here’s what a real $500,000 acquisition looks like:

| Component | Amount | % of Purchase Price |

|---|---|---|

| SBA 7(a) loan | $450,000 | 90% |

| Buyer cash | $25,000 | 5% |

| Seller note (on standby) | $25,000 | 5% |

| Total | $500,000 | 100% |

At closing, the bank wires $450,000 to the seller. You bring $25,000 in cash. The remaining $25,000 is a note. The seller receives that portion after the SBA loan is satisfied, on a schedule the lender approves. Interest accrues during the standby period; the seller isn’t forgoing a return entirely, just deferring it.

Seller financing can also go beyond the required equity injection. If a seller carries a larger note, say $75,000 on a $500,000 deal. That reduces the bank loan to $425,000 and lowers your monthly payment, which can strengthen your DSCR on paper.

Signing the LOI

Once valuation and deal structure are agreed on, document the key terms in a Letter of Intent (LOI). The LOI is non-binding. Neither party is locked in, but it establishes the purchase price, deal structure, and conditions before you spend money on lenders and attorneys. It’s also what you bring to the lender. Without it, most won’t start underwriting.

Include a financing contingency clause. This gives you a legal out if the SBA loan falls through, so you’re not on the hook for a deal you can’t finance.

Step 4: Find an SBA Preferred Lender and apply (1–2 weeks)

Not all SBA lenders are equal. An SBA Preferred Lender Program (PLP) lender can approve your loan in-house without sending it to the SBA for review. That saves 2–4 weeks. On a deal with an impatient seller, those weeks matter.

Use the SBA Lender Match tool to find PLP lenders in your area. When you apply, expect to submit:

- SBA Form 1919 (borrower information)

- SBA Form 413 (personal financial statement)

- 3 years of business tax returns and P&L

- 3 years of personal tax returns

- Purchase agreement or LOI

- Business plan with financial projections

- Independent business valuation (for deals with goodwill over $250,000)

Get everything into a shared folder with your accountant before you sit down with a lender. Incomplete applications are the single biggest cause of delays.

Read more: Best SBA lenders in 2026

Step 5: Lender underwriting and SBA review (2–4 weeks)

The lender reviews your full package, orders a business appraisal if needed, and evaluates the deal against SBA guidelines. Expect follow-up questions on your financials, the business’s tax returns, your transition plan, or the deal structure.

Respond to every document request within 24 hours. I mean that literally. Every day you sit on a lender’s question is a day added to your timeline. Buyers who respond fast close faster. It’s that simple.

If your lender isn’t a PLP lender, the file goes to the SBA for an additional review after the lender approves it. That adds 1–3 additional weeks.

Step 6: Loan commitment and conditions (1–2 weeks)

When underwriting clears, the lender issues a commitment letter, their formal offer to fund the loan, subject to conditions. Common conditions include:

- A life insurance policy naming the lender as beneficiary

- A signed standby agreement for the seller’s note

- Opening a business bank account

- Final confirmation of the seller’s financials

Work through these quickly. Each condition is a checkbox. The faster you check them, the sooner you close.

Step 7: Closing (1 day)

Both parties sign. The bank wires funds to the seller. And that’s how you own the business.

Closing day is usually anticlimactic compared to everything that led to it. A few hours of signatures, a wire transfer, and a handshake. The real work is the 6 steps before this one.

How long does it take to get an SBA loan to buy a business?

SBA lenders often quote 30–90 days. That range is accurate but not useful if you’re trying to keep a seller from walking. Here’s what those 90 days actually look like…and the two things that determine whether you’re at 30 days or 90.

| Phase | Time Estimate |

|---|---|

| Preparation (finances, documents, credit) | 1–2 weeks |

| Deal negotiation and LOI | 2–4 weeks |

| Application and underwriting | 3–6 weeks |

| SBA review (non-PLP lenders only) | 1–3 additional weeks |

| Conditions and closing prep | 1–2 weeks |

| Closing | 1 day |

| Total (signed LOI to funded) | 45–90 days |

Two factors determine how long it takes to get the SBA loan.

The first is how complete your document package is on day one. Buyers who walk into the lender with every document ready, 3 years of business and personal tax returns, a personal financial statement, an LOI, and a business plan.

Move through underwriting in 3-4 weeks. Buyers who trickle documents in over two weeks add that time directly to the back end of the process.

The second is whether your lender is an SBA Preferred Lender. A PLP lender approves your loan in-house. A non-PLP lender sends the file to the SBA for a separate review after approving it internally, adding 1-3 weeks you can’t control or speed up.

To protect the deal while financing is in process, include a financing contingency clause in your LOI and purchase agreement. If the loan falls through for any reason, this gives you a documented out without losing your deposit or exposing yourself to a breach of contract claim.

5 Mistakes that hurt your SBA loan approval chances

Most SBA acquisition loans that fail do so for predictable, avoidable reasons. Banks don’t publish this list. It’s not in their interest to. But having seen what derails deals, here are the 5 I’d warn every buyer about before they start the process.

1) Not having enough personal liquidity after the down payment

Draining your savings to make the 10% and walking in with nothing left is a red flag that lenders notice immediately. They want to see reserves after closing, money to cover unexpected expenses, a slow first month, or a key employee leaving. The down payment gets you in the door. Post-closing liquidity is what tells a lender you’ll survive the first year.

2) Buying a business that can’t service the debt

This is the most expensive mistake on the list because it’s the hardest to recover from. Run the DSCR math before you fall in love with any business. If the loan payment consumes more than the business generates in net cash flow, no lender will approve it. And you wouldn’t want them to.

3) Using a lender that isn’t SBA Preferred

A non-PLP lender adds 1–3 additional weeks to your timeline by sending the file to the SBA for a separate review. On a deal where the seller has given you a 60-day window to close, that delay can kill the transaction. Check PLP status before you apply, not after.

4) Submitting an incomplete or generic business plan

Lenders review acquisition business plans every day. They can tell within minutes whether projections are built from the actual business’s financials or copied from a template with the business name swapped in. A generic plan signals that you haven’t done the work, and raises questions about whether you’re ready to run the business at all.

5) Not disclosing known issues upfront

Surprises during underwriting sink deals. If there’s a pending lawsuit, a key customer contract expiring in 6 months, an environmental issue on the property, or a key employee who has signaled they might leave. Tell your lender before they find it themselves. Lenders can work around disclosed problems. Undisclosed ones appear deceptive, and the deal falls through.

“Business plans make SBA approval easy.” — loan experts

Most SBA loan guides mention the business plan in a single sentence and move on. That’s a mistake. For acquisition loans specifically, the business plan is the document that either builds or destroys a lender’s confidence in you as the new owner. A weak plan doesn’t just hurt your chances; it can kill an approval that would otherwise go through.

Here’s what lenders are actually looking for in an acquisition plan, and why a generic template won’t cut it.

What lenders specifically review in your business plan? (expert insights)

1) Financial projections (3–5 years): Revenue, expenses, and cash flow that demonstrate a DSCR of 1.15x or higher after debt service. Start from the seller’s actual historical financials, not round numbers. Year 1 should track closely with the seller’s last three years. Lenders flag hockey-stick projections from first-time buyers immediately.

2) Transition plan: How you’ll retain key staff, communicate the ownership change to customers, and maintain supplier relationships through the handover. This is the section most acquisition plans get wrong, and the one lenders notice is missing.

3) Market analysis: Specific to the business’s actual market, not a generic industry overview. If you’re buying a plumbing company in Phoenix, show Phoenix data, not national plumbing stats.

4) Your management background: Why are you the right person to run this specific business? Be direct. Relevant experience, industry knowledge, and any key hires you’re bringing in.

5) Use of proceeds: Every loan dollar accounted for, such as purchase price, working capital, inventory, and closing costs. Lenders distrust vague allocations.

A template gives you structure. It doesn’t give you the numbers. Lenders can tell the difference in about 30 seconds between a plan built around the actual business and one with swapped-in placeholders.

My advice: Start with the business plan before you even talk to a lender. It forces you to stress-test the numbers, think through the transition, and articulate why you’re the right person to run the business. By the time you sit down with a lender, you’ll already know whether the deal makes sense.

Use the Upmetrics SBA loan business plan template to build lender-ready projections from the ground up. And 400+ sample business plans, if you want a head start on the full plan structure.

The business is out there. Go find it.

Frequently Asked Questions

Can I use an SBA loan to buy a franchise?

How much do I need to put down to buy a business with an SBA loan?

What credit score do I need for an SBA loan to buy a business?

Can the seller stay involved after I buy the business?

What documents do I need to apply?

Can I roll working capital into the SBA acquisition loan?

Kaylee Philbrick-Theuerkauf

Kaylee Philbrick-Theuerkauf is the lead business plan consultant at Upmetrics. She specializes in guiding entrepreneurs to create clear and effective business plans. With over 8 years of experience, she has assisted many business owners in achieving their planning goals, raising over $1.5 billion in client funding. Read more