A declared disaster is overwhelming on its own. Your property is damaged, your income has stopped, your insurance company isn’t returning calls, and you’re trying to figure out what happens next.

So the thought of applying for an SBA disaster loan comes with its own list: forms, tax returns, ownership records, repair estimates, insurance details, and it keeps going.

I know you’re already dealing with the loss. The paperwork shouldn’t be the second thing you lose sleep over.

So I’ve broken it down. This guide covers how to check whether you qualify, which loan type fits your situation, what documents you actually need, how to fill out the application, and what happens after you submit.

Do you qualify for an SBA disaster loan?

SBA checks four things before your paperwork comes into consideration, so make sure you pass all those checks before diving straight into the application.

First, is your area covered by a federal disaster declaration?

You can confirm this through FEMA’s disaster declaration search or the SBA’s active disaster list. Declarations are usually county-based. If your county isn’t listed, you generally cannot apply under that declaration, whether the damage hit your home, your rental property, or your business.

Second, which applicant are you?

Business owner, homeowner, or renter. All three apply through the same SBA disaster loan program, but the form you file, the loan you’re eligible for, and the amount you can borrow all change based on this answer.

A business owner applying for a damaged storefront and a renter replacing a flooded couch are in the same program and have almost nothing else in common. So you have to get this right before you touch a form.

Third, can you prove the loss came from the disaster?

For physical damage, that’s before-and-after photos, contractor repair estimates, inventory loss records, and your property damage forms. For economic injury, there’s nothing to photograph. What you need is monthly revenue records showing the actual drop-off, which means the months before the disaster matter as much as the months after.

If you haven’t started documenting, start now. Take photos before cleanup. Save every email from your insurance company. Get customer cancellations in writing.

Fourth, are you still inside the filing window?

Physical damage loans give you 60 days from the disaster declaration, and Economic Injury Disaster Loans give you 9 months. So apply before the deadline even if your insurance claim is still pending. You can update the SBA later when the settlement comes through.

You cannot reopen a window that has closed. Which means the first real decision is what type of loan you’re applying for.

Which SBA disaster loan do you need?

Before you look at a single number, figure out which SBA disaster loan you are actually applying for, because the form, the limit, and the terms all follow from this.

Start with one question: did the disaster break something, or did it just cost you money?

If it broke something and you’re a business, that’s a Business Physical Disaster Loan. It covers repair or replacement of real estate, equipment, inventory, fixtures, machinery, and the rest of your business property.

If it costs you money without touching your property, you want an Economic Injury Disaster Loan (EIDL) that covers working capital when a disaster makes it hard to pay normal operating expenses.

Homeowners have two options, and they cover different things. A Home Disaster Loan repairs or replaces the residence itself. A Personal Property Loan covers what was inside it: furniture, clothing, appliances, a car. Renters can apply for that second one too. You do not need to own the building to get help replacing what you lost inside it.

Mitigation assistance sits slightly outside this framework. It doesn’t fix what the disaster did. It funds improvements that reduce the damage next time, like floodproofing, drainage work, or fire-resistant materials.

A business can use a physical disaster loan and an EIDL together. Homeowners can combine a home disaster loan with a personal property loan. Applying for one does not close the door on the other. Which raises the obvious question: how much does each one actually give you?

SBA disaster loan limits, rates, and repayment terms?

Once you know your loan type, the SBA decides the amount based on your verified loss, what insurance or other aid covers, and whether you can repay it

Here is the simplest way to think about the loan limits:

| Applicant or loan type | Maximum amount |

| Business physical disaster loan | Up to $2 million |

| Economic Injury Disaster Loan | Up to $2 million |

| Homeowner real property loan | Up to $500,000 |

| Homeowner’s or renter’s personal property loan | Up to $100,000 |

| Mitigation assistance | Up to 20% of verified physical damage |

There’s a good chance you’ll assume a business can take $2 million in physical damage money and another $2 million in EIDL. It can’t. A business that qualifies for both is capped at $2 million combined.

Homeowners work the opposite way. The $500,000 for the residence and the $100,000 for personal property are separate ceilings, so a homeowner who loses the house and everything in it can reach $600,000 across two loans.

So that’s the size of the loan. What it costs to carry it matters more, and I’d argue it’s the part people skim past fastest. On a 30-year term, that’s where most of the real money sits.

What does it cost?

Your first payment is usually deferred for 12 months, and interest does not accrue during that time. After that, repayment can stretch up to 30 years, based on your ability to repay. There is no prepayment penalty.

The interest rate depends on whether the SBA believes you can get credit elsewhere.

- If you cannot reasonably borrow from a conventional lender, the rate will not exceed 4%.

- If you can get credit elsewhere, the rate will not exceed 8%.

That decision matters most for EIDL. Economic Injury Disaster Loans are only available to small businesses that the SBA finds unable to get credit elsewhere.

For homeowners and renters, rates are usually lower than regular business disaster loan rates.

Will you need collateral?

Below a certain size, none. Physical damage loans require collateral only above $50,000 in a Presidential declaration, or above $14,000 in an agency declaration. For EIDL, the threshold is $50,000.

Above those lines, the SBA asks for what you have. Real estate is preferred, even when the equity doesn’t cover the full loan.

If you’re a business owner reading that with your house in mind, there’s a protection worth knowing. On loans of $200,000 or less, the SBA will not require your primary residence as collateral if you hold other assets of equal quality and equal or greater value.

The bottom line is that the SBA will ask for available collateral, but it will not decline a loan for lack of collateral. Credit works on the same logic. Though it helps shape the loan offer, it doesn’t get you rejected.

Will your credit disqualify you?

There’s no published minimum credit score for disaster loans. What the SBA reviews is repayment ability, federal debt status, and other risk factors.

The genuine blockers could be

- Delinquency on federal debt

- An active bankruptcy

- An unresolved problem on a prior SBA loan

If credit is your main worry, read our separate guide on how to get an SBA loan with bad credit.

Everything so far has assumed your loss is uncovered. It usually isn’t, and that changes the number more than credit ever will.

How does insurance change the number?

The SBA will not pay you twice for the same damage. If insurance, FEMA, or another source covers part of it, your loan amount comes down, or you agree to put those proceeds toward repaying the loan.

None of that is a reason to wait for a settlement, and waiting is the mistake that costs people the most.

If your claim is pending, apply anyway and say so. The SBA can lend against your total loss up to the program limits, provided you agree to use the insurance proceeds to reduce or repay the loan. Give your best estimate, include the claim details you have, and update the number when the settlement lands.

Insurance timelines routinely outlast the 60-day physical damage window. The SBA can adjust your loan amount later. It cannot reopen a deadline you missed.

What documents do you need for an SBA disaster loan application?

Every document you upload answers one of four questions. What was damaged? What did the disaster cost you? What will insurance cover? Can you repay the loan?

Which documents you need depends on which question is doing the heavy lifting for your loan type.

Documents for a business physical disaster loan

For a business physical disaster loan, you have to prove that specific property was damaged and estimate what it costs to make it whole. So the documents you will need are:

- Completed SBA disaster loan application, usually SBA Form 5

- Business tax returns

- Personal tax returns for each principal owner

- SBA Form 413 for personal financial information

- SBA Form 2202 for business liabilities

- IRS Form 4506-T, if the SBA needs tax transcript authorization

- Business registration documents and ownership details for major owners

- Insurance policy details and claim status

- Repair estimates, contractor quotes, and photos of the damage

- Inventory loss records, if inventory was destroyed

Documents for an EIDL application

The entire case is financial, and it’s a comparison of what your revenue looked like before the disaster against what it looked like after.

- Completed SBA disaster loan application, usually SBA Form 5

- Business tax returns

- Personal tax returns for each principal owner

- SBA Form 413 for personal financial information

- SBA Form 2202 for business liabilities

- IRS Form 4506-T

- Profit and loss statement

- Monthly sales or revenue records covering the months before and after the disaster

- A schedule of fixed operating expenses: rent, payroll, utilities, fixed debt payments

- Business registration documents and ownership details

Pull more months than you think you need. A twelve-month overview gives your drop-off a baseline to sit against.

A business with both physical damage and revenue loss files for both loans, which means assembling both sets.

Documents for homeowners and renters

For homeowners and renters, it’s far shorter, and the split between the two comes down to what you own.

- Completed SBA disaster loan application, usually SBA Form 5C

- Proof of identity

- Proof that the damaged home was your primary residence

- Insurance policy details and claim status

- Photos of the damage

- Repair or replacement estimates

- Records for damaged personal property

- Income or repayment-related documents, if requested

Homeowners are documenting the structure, and renters are documenting what was inside it: furniture, clothing, appliances, a vehicle. If you rent, you don’t need to prove anything about the building; just have the receipts, photos, or a credible account of what you lost handy.

Before you upload anything, put your documents side by side and check that names, addresses, dates, ownership percentages, and dollar amounts agree across every one of them.

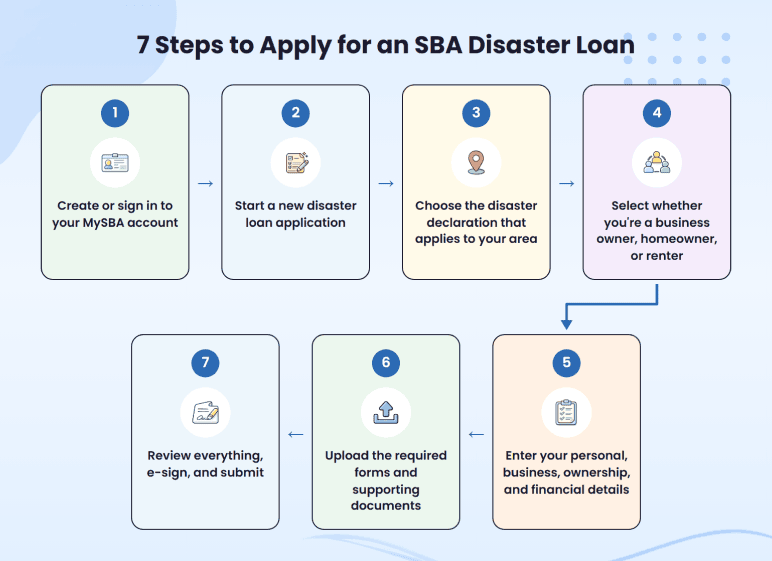

How to fill out the SBA disaster loan application (the application process)

Once your documents are ready, the application itself is fairly straightforward.

You can apply online through the MySBA Loan Portal, by phone through SBA disaster assistance, or in person at a Disaster Recovery Center if one is available near you. For most applicants, applying online is the easiest route because you can upload documents, track requests, and check your status in one place.

Here’s the basic process:

The fields that need the most attention are usually the financial and ownership sections.

For a business application, enter your legal business name, EIN, business structure, and industry code exactly as they appear in your registration and tax records. If the form asks for revenue, cost of goods sold, or operating expenses, do not estimate or round the numbers. Use the same figures that appear in your tax returns, P&L, or monthly revenue records.

Ownership details also need to be current. List owners with the required ownership percentage, and make sure names, addresses, Social Security numbers, and ownership shares match your business records.

The insurance section is another place where applicants make mistakes. Do not leave it blank just because your claim is still pending. Add your insurance details, claim number if you have one, and note that the settlement is pending.

Before you submit, do one last consistency check. Your application, tax returns, P&L, ownership records, insurance details, and SBA forms should all be correct.

What happens after you submit your SBA disaster loan application?

After you have submitted your application, SBA starts with a couple of basic checks that include verifying your identity, checking credit history, and reviewing federal debt (or any other eligibility flags)

If there’s physical damage involved, SBA may review repair estimates, photos, insurance details, or inspection information. For economic injury, it reviews financial records to understand the revenue impact.

After the review process, the SBA checks whether the loan amount makes sense based on your loss, repayment ability, insurance, and other aid. Based on that, you may be approved, partially approved, asked for more information, or declined.

If the loan is approved, you will be asked to review the loan terms and sign the loan documents before funds are disbursed.

How much time does the entire process take?

The timeline is not fixed, but here is a realistic range to keep in mind:

- Clean physical damage application: often around 2 to 3 weeks for a decision

- EIDL application: often closer to 3 to 6 weeks

- High-volume disaster period: 8 to 12 weeks is not unusual

- Missing documents or unanswered SBA requests: can push the timeline longer

The process can get delayed in case of missing documents, unanswered financial questions, or if the volume of disaster loans is high.

While your application is under review, check the MySBA Loan Portal regularly. Most delays happen when the SBA asks for a corrected document, explanation, or extra proof, and the applicant does not respond quickly.

Though you can’t control the timeline of the loan process, what you can control is ensuring your application is complete and being prompt in case of follow-up questions. That itself is enough to speed up the process.

Wrapping up

The tough part about filling out an SBA disaster loan application is about giving the SBA a file that is easy to verify.

So before you apply, make sure your disaster declaration, filing deadline, insurance status, financial records, and required forms are in order. Your numbers should match across your tax returns, profit and loss statement, revenue records, and application.

And if you need help preparing SBA-ready financials, Upmetrics provides SBA-specific templates, AI-assisted writing, and financial forecasting built for disaster and 7(a) applications.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

Do I have to accept the full SBA disaster loan amount?

Can I use an SBA disaster loan to upgrade damaged property?

Can I apply if my business is closed temporarily?

What if I make a mistake after submitting the application?

Anthony Ray

Anthony Ray is an SBA Commercial Loan Officer specializing in commercial lending, financial analysis, and risk management. Over the years, he has helped business owners secure the financing they need to grow and succeed. Besides that, he shares practical insights on banking, loans, and financial strategies based on his industry experience. Read more