Got your SBA loan declined? Here’s something to make you feel a little less alone.

According to the Federal Reserve’s 2025 Small Business Credit Survey, 45% of businesses that applied for an SBA loan were flat-out rejected. Only 32% got full approval.

As a lead business consultant at Upmetrics, I talk to dozens of business owners every week. Someone walks me through their whole plan, their numbers, their excitement, and then: “…but I got denied.”

The frustration is real. You did the work, pulled together the paperwork, waited weeks, and got a letter that feels like a door slamming shut.

But here’s what I’ve learned after helping dozens of applicants come back from a denial: nine times out of ten, there’s one specific thing that tripped them up. Not ten things. One. And that one thing is almost always fixable.

In this guide, I’ll walk you through the most common denial reasons, what to do in the next 90 days, and where to find funding if you can’t wait that long.

Understand why your SBA loan was denied (w/ 10 potential reasons)

Before you take the next steps, first you’d need to understand why you got denied in the first place. So let’s discuss that.

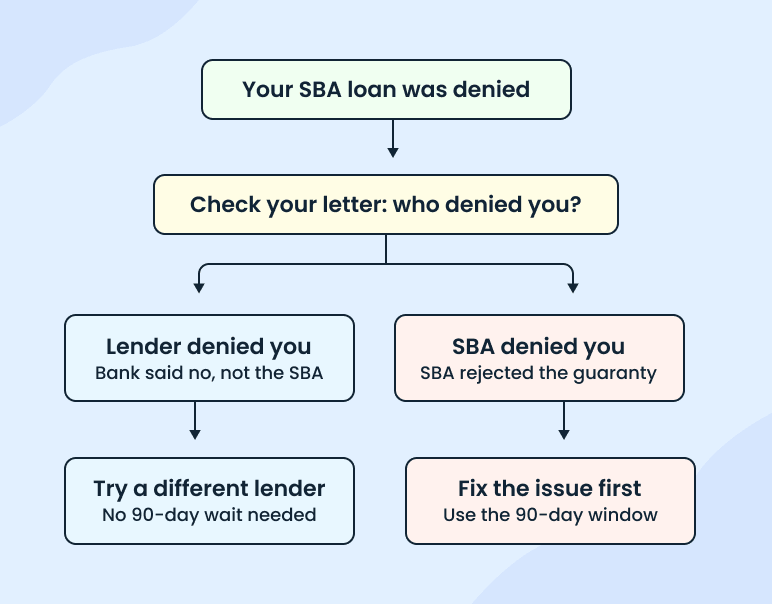

Reading your SBA loan denial letter?

The first thing I tell every denied applicant: go read your denial letter again. Carefully this time.

Most denial letters are about a page long. Somewhere on that page, there’s a line that states the reason you were denied. It might say something like “insufficient cash flow,” “credit history,” or “ineligible business type.” That one line is your starting point.

The letter should also tell you what type of SBA loan you applied for, who denied you (the lender or the SBA), whether reconsideration is an option, and how to contact someone for more details.

If your letter is vague, or if you read it and still don’t understand what went wrong, call the lender directly and ask for the specific reason in writing. You’re entitled to that. Don’t assume or guess. Get it in writing so you know exactly what to fix.

Did the lender or SBA deny your application?

When you apply for an SBA loan, your application goes through two layers. First, the lender (usually a bank) reviews it against their own standards. If they approve it, they send it to the SBA for a guarantee. The SBA then runs its own check.

So a denial can come from either side, and the difference matters.

If the lender denied you, that means the bank said no based on its own risk appetite. A different SBA-approved lender might look at the same application and say yes. You can shop around right away.

If the SBA denied you, that means the application passed the lender but failed at the SBA level. This is usually an eligibility issue: wrong industry, size standard violation, or a flag in the CAIVRS database (which tracks prior government loan defaults). You need to fix the problem before reapplying anywhere.

10 Most common SBA loan denial reasons

Your denial letter may sum up the reason in one line. Here’s what that line actually means, and what a realistic fix looks like.

1. Credit score too low. Most lenders want a personal credit score of 680+, with many preferring 700+. On the business side, your FICO SBSS score should be at least 165 out of 300.

2. Insufficient cash flow or low DSCR. Your debt service coverage ratio (operating income ÷ total debt payments) needs to be 1.15 or above. Below that, lenders don’t see enough margin.

3. Not enough time in business. The SBA doesn’t set a minimum, but most lenders want 2+ years of operating history.

4. Too much existing debt. A high debt-to-income ratio signals you’re already stretched thin.

5. Insufficient equity injection. The SBA typically expects at least 10% owner investment for new businesses or acquisitions.

6. Inadequate collateral. Not always required (especially for smaller 7(a) loans), but if the lender asked and you came up short, that’s a flag.

7. Ineligible industry. Nonprofits, banks, gambling, life insurance, passive real estate, and lobbying firms. Check the SBA size standards table to confirm eligibility.

8. Prior government loan default. It shows up in the CAIVRS database. Hard stop, not fixable in 90 days.

9. Business plan not convincing. Weak projections, missing market analysis, no clear use of funds. Lenders read these closely.

10. Incomplete or inaccurate documentation. Missing financial statements, stale tax returns, numbers that don’t match. Frustrating because it’s entirely avoidable.

For more details, check out our detailed blog post on SBA loan requirements.

Can you appeal an SBA loan denial?

Most people don’t know this option exists. The SBA has a formal appeals process through its Office of Hearings and Appeals (OHA).

That said, I want to be upfront: OHA appeals are most useful for eligibility disputes and not credit-based denials. If you were denied because of a size standard determination, a NAICS code error, or a question about whether your business qualifies for the program, the OHA is worth looking into.

You can file through the Hearings and Appeals Submission Upload Application at appeals.sba.gov, by email, or by fax. Appeals typically take about 90 days to process.

But if you were denied for low credit, weak cash flow, or an unconvincing business plan, my honest advice is to skip the appeal. Fixing the issue and reapplying will get you funded faster.

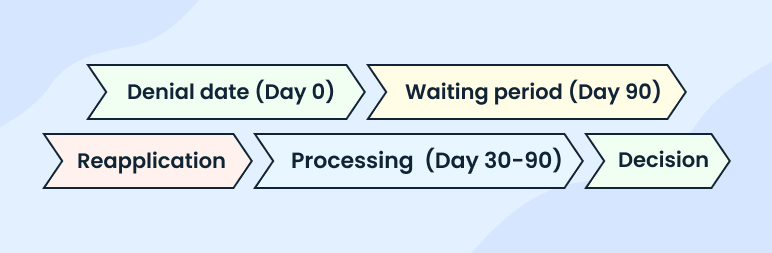

The 90-day rule: what it actually means

Ever since you got your denial, you must’ve heard about this 90-day thing. So to clear the air, it’s how long you have to wait before reapplying for an SBA loan.

But there’s more to it than just “wait three months and try again.”

First, the period starts from the date on your denial notice (not the date you submitted your application). Check that letter. That’s your Day 1.

Second, this rule has some exceptions that a lot of guides don’t mention. If you can provide new documentation that directly addresses the denial reason (say, updated financials or a revised business plan), some lenders will review your application sooner than 90 days.

It’s not guaranteed, but it’s definitely worth asking.

Third, and this is the most important one:

If your denial came from the lender and not the SBA, you may not need to wait.

Different lenders have different risk appetites. A community bank that specializes in your industry might approve a file that a national bank turned down. You still need to disclose the prior denial, but you can start that conversation right away.

Now, a question I get asked a lot: “Did the denial hurt my credit?”

The denial itself doesn’t show up on your credit report. But the application did trigger a hard inquiry, which can temporarily lower your score by a few points. That effect usually fades within 12 months.

So don’t panic about it, but don’t go submitting applications to five more lenders in the same week either. Each one is another hard pull.

My advice: use the 90 days productively. Don’t just sit and wait. This is your window to fix whatever caused the denial, and I’ll walk you through exactly how to do that in the next section.

Next steps: strengthening your application before you reapply

Three months may feel like a long wait when you desperately need that funding. Here’s what I suggest: a realistic fix plan, organized by what you can fix the fastest.

Improve your credit score

This one is the slowest fix on the list, so if credit was your denial reason, start immediately. On the personal side, most SBA lenders want a 700+ FICO score. Some will work with 680, but below that, you need to work really hard.

Pay down credit card balances to get utilization below 30%, set up autopay on everything, and don’t open any new credit accounts while you’re working on this. Check your report at AnnualCreditReport.com and dispute any errors you find.

On the business side, your FICO SBSS score should be 165 or above. You can build this by opening a business credit card, paying it on time, and making sure your vendors report payment history to business credit bureaus.

Timeline: 6 to 12 months for meaningful improvement. There’s no shortcut.

Fix your cash flow/DSCR

The DSCR formula is simple: available operating income ÷ total debt payments. Lenders want that number at 1.15 or above. If yours came in lower, you have two options to fix that: increase income or reduce expenses.

Go through your recurring costs line by line.

- Cancel what you don’t need.

- Renegotiate vendor contracts where you can.

On the revenue side, document everything. If you have income that wasn’t reflected in your last application (cash sales, new contracts, seasonal bumps), make sure it shows up in your updated financials.

Then run a cash flow projection that includes your proposed loan payment. Lenders want to see that the payment fits inside your monthly cash position.

Timeline: 3 to 12 months, depending on how much ground you need to cover.

Equity injection (3-6 months to save or liquidate)

The SBA typically requires at least 10% owner investment for new businesses or acquisitions. That money needs to come from acceptable sources such as personal savings, liquidating personal assets, or, in some cases, seller financing.

What lenders won’t accept is a personal loan that’s going to be repaid from the business. That totally defeats the purpose. They want to see that you have skin in the game with real capital at risk.

If you’re short on the 10%, start saving now. Even if it takes 3 to 6 months to get there, having that equity ready makes the rest of your application significantly stronger.

Get documentation in order

This one is the easiest and fastest to fix. And honestly, one of the most common reasons applications get rejected. Missing documents aren’t a judgment on your business. They’re just a paperwork problem.

The most common things applicants miss are: personal financial statements, 2 to 3 years of both business and personal tax returns, a current profit and loss statement, and a current balance sheet. “Current” means within 60 days of your application date.

Yet another mistake I see business owners constantly make is that they apply in January or February with preliminary financials that haven’t been filed yet.

So wait for your filed returns. Applying with draft numbers is just giving lenders a reason to say no.

Timeline: 2 to 4 weeks if you have the records and just need to organize them.

Fix your business plan and financials

A weak business plan is one of the most fixable denial reasons, and one of the most common. I say this to clients all the time: the plan doesn’t need to be 50 pages. It needs to answer the questions that lenders are actually asking.

Here’s what they’re looking for:

- A clear, specific use of funds (not just “working capital”),

- Realistic financial projections with monthly cash flow for 18 to 24 months,

- Three scenarios (conservative, moderate, optimistic) so they can see your downside thinking,

- Market analysis showing demand in your specific geography,

- A management team section that proves you can execute, and

- A repayment plan that shows how loan payments fit into your projections.

If your previous plan got denied, here’s why it probably fell short: projections were too optimistic without supporting data, assumptions weren’t explained (where did those revenue numbers come from?), personal financial statements weren’t tied to the business plan, or the numbers were outdated.

If you’re rebuilding your business plan or financial projections for your next SBA application, consider using Upmetrics to simplify updating your plan. It has everything you need to draft a lender-ready business plan and financial projections.

You can start with an SBA-ready business plan template and build from there, or check out our guide on how to write a business plan for a loan.

Seek assistance from SCORE mentors and SBDCs when needed

SCORE mentors and SBDCs are available in every US state. Get in touch for any guidance or assistance throughout the process.

SCORE offers free mentors who’ve guided hundreds of business owners through exactly this process. SBDCs (Small Business Development Centers) can review your financials, help you build a stronger application, and even practice your lender pitch with you.

I’ve seen clients completely turn around a denied application with six weeks of SBDC support. It’s free. Use it.

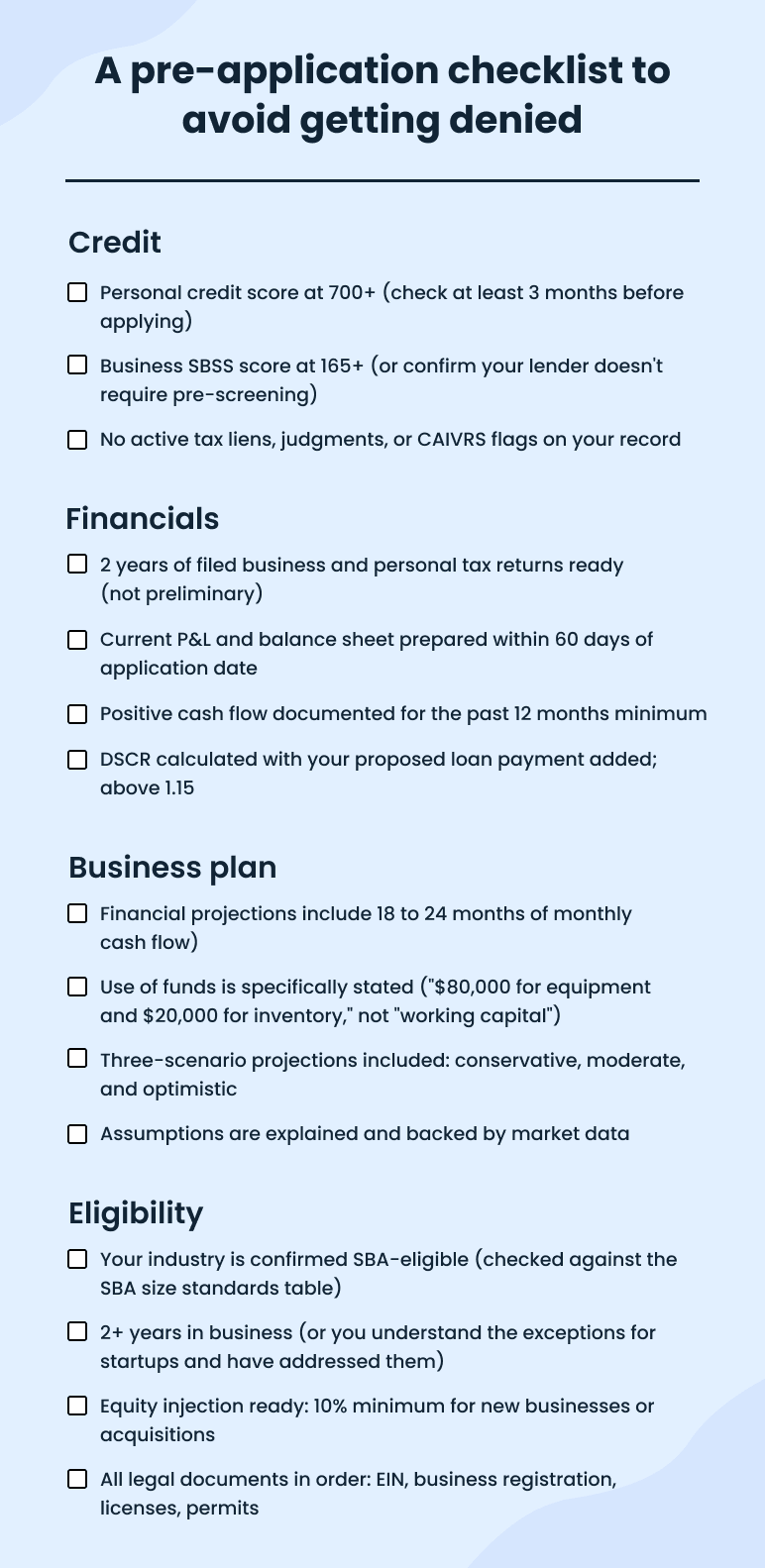

A pre-application checklist to avoid getting denied

If your denial was a documentation gap, a credit score that was just barely short, or a business plan that needed more detail, and you’ve worked through the fixes I covered in the previous section, you’re probably in good shape to reapply.

However, before you submit that application again, run through this checklist. It takes 10 minutes and can save you another 90-day wait.

Credit

- Personal credit score at 700+ (check at least 3 months before applying)

- Business SBSS score at 165+ (or confirm your lender doesn’t require pre-screening)

- No active tax liens, judgments, or CAIVRS flags on your record

Financials

- 2 years of filed business and personal tax returns ready (not preliminary)

- Current P&L and balance sheet prepared within 60 days of application date

- Positive cash flow documented for the past 12 months minimum

- DSCR calculated with your proposed loan payment added; above 1.15

Business plan

- Financial projections include 18 to 24 months of monthly cash flow

- Use of funds is specifically stated (“$80,000 for equipment and $20,000 for inventory,” not “working capital”)

- Three-scenario projections included: conservative, moderate, and optimistic

- Assumptions are explained and backed by market data

Eligibility

- Your industry is confirmed SBA-eligible (checked against the SBA size standards table)

- 2+ years in business (or you understand the exceptions for startups and have addressed them)

- Equity injection ready: 10% minimum for new businesses or acquisitions

- All legal documents in order: EIN, business registration, licenses, permits

Consider alternative funding options while you wait

Let’s be practical. A 90-day waiting period plus another 30 to 90 days for SBA processing means you could be 6 months out from SBA funding. You can’t put all your eggs in one basket.

You need to consider other options, if your business needs money before that.

None of these are as cheap as an SBA loan. That’s the tradeoff. But some of them can get cash in your hands within days, and they can keep your business running while you work toward a stronger SBA application.

Here’s a quick comparison:

| Option | Best For | Funding Speed | Typical Cost | Min Credit |

|---|---|---|---|---|

| Online term loans | Established businesses needing a lump sum | 1-7 days | 10-40% APR | 600+ |

| Business line of credit | Recurring expenses, variable cash needs | 1-7 days | 10-30% APR | 600+ |

| SBA Express Loan | Faster SBA option (still SBA-backed) | 36-hour decision | SBA rates | 650+ |

| SBA Microloan | Startups, small needs (up to $50,000) | 2-4 weeks | 8-13% | 575+ |

| Business credit card | Small recurring purchases | Immediate | 20-28% APR | 640+ |

| Merchant cash advance | High-volume retail/restaurants | 24-48 hours | Very high (factor rates 1.2-1.5) | 500+ |

| CDFI / nonprofit loans | Underserved communities, micro-businesses | 2-4 weeks | Below market | Flexible |

A few things worth calling out. SBA Express Loans still go through the SBA program, but lenders can make decisions within 36 hours instead of weeks.

If your denial was lender-level and you’re switching to a new lender, ask if they offer Express. SBA Microloans go up to $50,000 through nonprofit intermediaries, and the credit requirements are lower than standard 7(a) loans, which makes them a solid option for startups.

Merchant cash advances are fast, but they’re expensive. I’d only recommend them if you have strong daily card revenue and need bridge funding for a very short period. For most business owners, a line of credit or an online term loan is a better middle ground.

Important: As of 2025, SBA loans can no longer be used to refinance MCA debt, so factor the full cost into your decision.

We’ve put together a more detailed guide on “SBA loan alternatives” that breaks down each of these options further.

Can you switch SBA lenders and apply right away?

Yes, if your denial came from the lender and not the SBA itself. I covered this distinction earlier, but it’s worth repeating because it changes your timeline completely.

Different SBA-approved lenders interpret the same SBA guidelines differently. A community bank that specializes in restaurants might approve a file that a big national bank turned down, even with the same numbers.

Consider using the SBA Lender Match tool to find approved lenders in your area, and be upfront about the prior denial, and explain what you’ve fixed. Lenders respect that.

Your next application needs a stronger plan behind it

Build a lender-ready business plan that passes review

Ready to Reapply?

Getting your SBA loan denied is common. It’s not a verdict on your business, but feedback on your application.

Now you know the most likely reason it happened. You know whether the lender or the SBA made the call, what the 90-day rule actually means, and which fixes to prioritize based on your specific denial reason.

The next step is simple: pick the one thing that caused your denial and fix it. If it’s your credit score, start paying down balances today. If it’s documentation, gather your filed returns and updated financials. If it’s your business plan, rebuild it with the projections and details that lenders actually want to see.

That last one is where we can help. Upmetrics is a modern, advanced business planning software that helps you build or update your business plan, financial models, and statements, and everything an SBA lender might ask; all in one place.

And if you want a second set of eyes before you reapply, our consulting team has helped dozens of business owners come back from a denial with a stronger application. Get in touch, we’re happy to walk you through it.

Frequently Asked Questions

Can I reapply for an SBA loan after being denied?

What disqualifies you from an SBA loan?

Does a denied SBA loan hurt your credit?

What is the SBA Office of Hearings and Appeals?

How long does it take to get an SBA loan approved after being denied?

Kaylee Philbrick-Theuerkauf

Kaylee Philbrick-Theuerkauf is the lead business plan consultant at Upmetrics. She specializes in guiding entrepreneurs to create clear and effective business plans. With over 8 years of experience, she has assisted many business owners in achieving their planning goals, raising over $1.5 billion in client funding. Read more