When people ask me when they should write a business plan, my answer is always the same: it depends on where they’re at right now.

Do you have a business idea? Are you about to launch? Do you need a loan? Are you already running a business without a plan? Each of these situations calls for a different kind of business plan.

Timing within those situations matters too. Writing a plan two days before a loan meeting is usually too late. Writing a detailed plan before you’ve talked to a single customer is often too early. If the timing is wrong, the plan won’t be as useful, no matter how well it’s written.

In this guide, I’ll show you the best time to write a business plan based on where your business is right now.

When is the best time to write a business plan?

The best time to write a business plan depends on your situation. There isn’t one right time that works for everyone.

Below are the six situations I see most often when founders ask when they should write a business plan. Find the one that best matches your situation and start there. If your situation changes later, you can always come back and read the others.

Here’s the quick filter I recommend: write a business plan now if you’re about to spend money, seek funding, hire, sign a lease, launch, expand, or change direction. But if you still don’t know your customer, demand, pricing, or basic business model, don’t force a full plan yet.

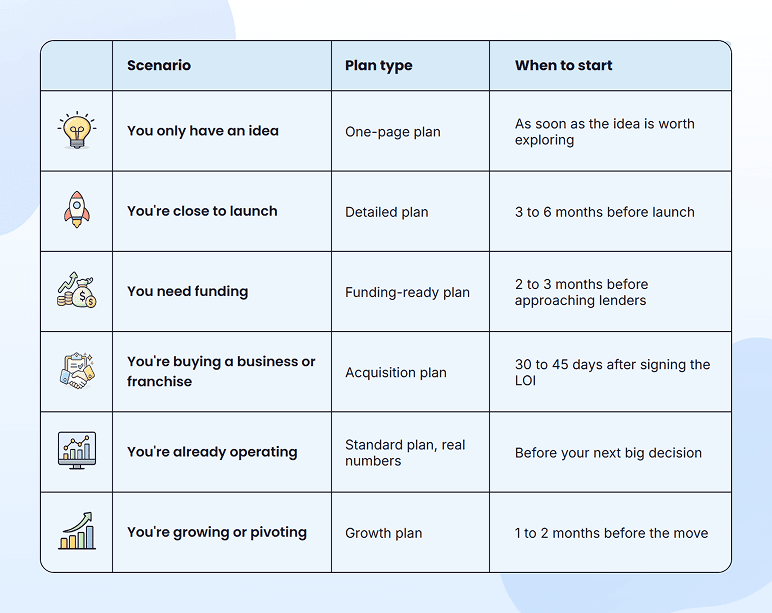

1. If you only have an idea

You have a business idea and a feeling that it could become something real. What you don’t have yet is proof.

A simple one-page business plan can help. It forces you to think through who your customer is, what they’ll pay for, and how much money you’ll need to get your first sale.

At this stage, a one-page plan is enough. Write down your goals, target customer, competitors, revenue streams, and finances. Just make sure each section is specific.

Once you’ve written it down, ask yourself two questions:

- Could this idea make more money than it costs to run?

- Is there a real market for what I want to sell?

If you can’t answer those two questions, the idea probably isn’t ready yet. You need more time talking to potential customers, not more time writing.

Start writing as soon as you decide the idea is worth exploring. Just don’t spend more than an afternoon on it.

2. If you are close to launch

Once you’ve decided to launch, it’s time for a more detailed business plan. This is the plan you’ll actually use to run the business.

At this stage, your plan should cover your business model, target market, competition, marketing, operations, and financials.

A detailed plan will help you:

- Figure out how customers will actually find you, compare you, and decide to buy

- Catch launch problems early, such as permits, supplier delays, staffing gaps, inventory, or fulfillment issues

- Check whether your pricing, sales forecast, and monthly expenses can support the business

- Decide what needs to happen before opening day, and who is responsible for it

- Build a backup plan for slower sales, higher costs, or delays after launch

The financial section is especially important. Many founders rush through it, but it’s the part that tells you whether the business can actually survive or not.

Make sure you have realistic revenue forecasts, expense projections, cash flow forecasts, and a break-even analysis. These numbers help you understand whether the business can make it through the first few months.

Start writing 3 to 6 months before launch. The financials take real time to get right, and you want them clear before the lease is signed or before making other major commitments.

3. If you need funding

If you need outside funding to start or grow your business, a complete business plan (funding-ready plan) is no longer optional. Lenders and investors don’t fund ideas. They fund evidence that you’ve thought it through, run the numbers, and considered what could go wrong.

A funding-ready plan includes everything in a launch plan, plus a few extra pieces:

- A strong executive summary

- Three to five years of financial projections

- A clear explanation of how you’ll use the money

- A repayment plan for lenders or an exit strategy for investors

If you’re applying for an SBA loan, you’ll also need to show your owner equity injection and how the business will repay the loan.

The people reviewing your plan are trying to answer one question: Can this business use the money successfully and either pay it back or generate a return?

That’s why they pay close attention to:

- Your financial projections

- Your use of funds

- Your experience and management team

Start writing this plan 2 to 3 months before you plan to seek funding. Financial projections take time to build, and the executive summary is usually one of the last sections you finalize.

Build a funding-ready plan with projections lenders trust

4. If you are buying a business or franchise

When you’re buying a business or franchise, the business plan is for two people: the lender, who may finance the purchase, and you, the buyer.

The lender wants to know if the deal makes financial sense. You need to know whether the business is actually worth buying.

An acquisition plan includes everything in a funding plan, plus a few things specific to buying an existing business:

- A review of the business’s revenue history and performance

- Any major risks, such as relying too heavily on one or two customers

- A 90-day transition plan for taking over the business

- A working capital calculation to cover the first few months after closing

The most important step is checking the numbers.

Sellers often present their business in the best possible light. Some expenses may be treated as one-time costs even though they happen every year. A large share of revenue may come from just a few customers. Sometimes the tax returns and internal financial statements don’t tell the same story.

Before writing the plan, verify the numbers yourself. Build your plan around what’s actually true, not just what the seller says.

Another thing many first-time buyers overlook is working capital.

The purchase price is only part of the cost. You’ll also need enough cash to keep the business running during the first few months while you take over operations and wait for revenue to come in. SBA lenders pay close attention to this.

Start writing the plan within 30 to 45 days of signing the letter of intent (LOI). Most SBA lenders expect it during that period, and verifying the numbers usually takes longer than buyers expect.

5. If you have already started

If you’ve been running your business for months or even years without a business plan, you’re not behind. In fact, you have something many first-time founders don’t: real customers, real sales, and real data.

At this stage, you need a standard business plan built around real numbers. The goal isn’t to create paperwork. It’s to take a business you’ve been running from experience and put it on paper so you can clearly see what’s working, what’s not, and what needs to happen next.

The plan still covers the usual sections: your business model, market, customers, operations, and financials. The difference is that you’re working from real numbers.

Your financial section should start with the last 12 months of actual results: how much money came in, how much went out, and what your cash flow looked like. Your marketing section should start with where your customers actually came from, not where you hope they’ll come from.

Build the plan around what’s true today.

One mistake I see is founders writing a plan just to have one. A business plan is only worth the effort if it helps you make a real decision, such as:

- Raising prices

- Hiring someone

- Expanding into a new market

- Applying for a loan

- Dropping a product or service that isn’t working

Start writing before your next big decision, not after. Real numbers go out of date faster than most founders expect, and a plan based on six-month-old data can already be leading you in the wrong direction.

6. If you are growing

When your business is about to take a big step, such as opening a new location, entering a new market, making a key hire, changing prices, or shifting your business model, the plan that got you here may not be enough for what comes next.

Growth changes the numbers, and your old plan was built for a different stage of the business.

At this point, you need a growth plan. It covers the same areas as your current plan: your business model, market, customer acquisition, operations, and financials. The difference is that everything has to be viewed at a larger scale.

Customer acquisition costs that work today may not work as you grow. Operations that one person could manage at $500K in revenue may require a team at $1.5M. Cash flow can also change as you add inventory, payroll, equipment, or new locations.

The plan needs to account for those changes, not just assume today’s numbers will scale.

One mistake I see often is founders planning for only the best-case scenario. They assume growth will go exactly as planned and make decisions based on that assumption. When growth is slower than expected, cash can become a problem very quickly.

That’s why your growth plan should include at least two scenarios:

- Your expected outcome

- A lower-growth scenario where revenue comes in 30-50% below expectations

Start updating the plan 1 to 2 months before the growth move, not after you’ve already committed to it.

The plan is most useful when it’s helping you decide whether to move forward. Once you’ve signed the lease, hired the team, or changed the pricing, the plan becomes a record of the decision instead of a tool for making it.

So that’s the six situations. Six different versions of a business plan. What makes them work isn’t the format or the length. It’s the timing. A business plan is most useful when it helps you make a decision, not when it simply documents one you’ve already made.

How long does each type of business plan take?

The answer depends on the type of plan you’re writing. A one-page plan and a funding-ready plan require very different amounts of work.

| Plan Type | Typical Time | Best For |

| One-page or lean plan | 1-2 hours | Idea stage, side hustles, internal planning |

| Detailed business plan | 3-7 focused days | Pre-launch businesses, growing companies |

| Funding-ready plan | 2-4 weeks | SBA loans, bank loans, investor pitches |

| Acquisition plan | 2-4 weeks | Buying a business or franchise |

| Growth plan | 1-2 weeks | Expansion, new locations, new markets, pivots |

The goal isn’t to spend as much time as possible. It’s to spend enough time to make better decisions.

Research published in the Harvard Business Review found that entrepreneurs who spent around 3 months planning were more likely to build a successful business. But spending much longer than that didn’t provide additional benefits because markets, customers, and assumptions can change over time.

A six-month business plan isn’t six times better than a three-week plan. Most of the time, it’s just six months older.

If you’re unsure how detailed your plan should be, see our guide on how long a business plan should be.

Conclusion

If you’ve read this far, the answer is probably much clearer now. There isn’t one best time on the calendar to write a business plan. It depends on your situation.

A one-page plan if you’re exploring an idea. A complete plan before launch. A formal plan when you’re seeking funding. An acquisition plan if you’re buying a business. A standard plan built on real numbers if you’re already operating. A growth plan if you’re expanding or making a major change.

Most business plans don’t fail because they’re written badly. They fail because they’re written too late to influence anything.

Pick the situation that matches where you are, set yourself a real deadline, and get started. And if you need help along the way, Upmetrics offers business plan templates, an AI business plan generator, and built-in financial forecasting tools to make the process easier.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

What if my business plan turns out to be wrong?

Should I write a business plan before or after registering my business?

Should I write a business plan before talking to customers?

How often should I update my business plan?

Do I need a business plan if I already have a pitch deck?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more