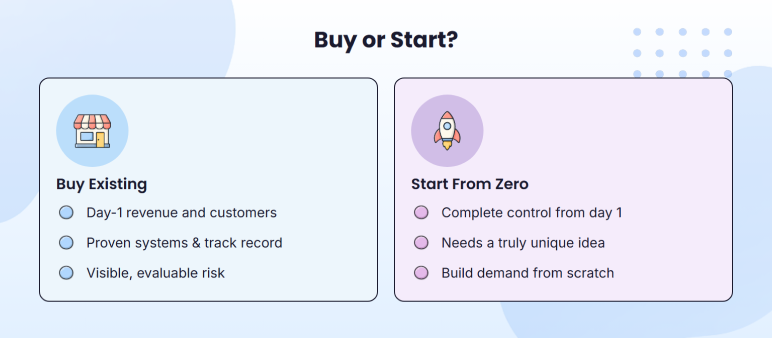

Buying an existing business removes the hardest question: will this work? The answer is already there in the revenue, the customers, and the day-to-day operations.

But…

Knowing how to buy a business without making a costly mistake is exactly why you’re here. Most first-time buyers get stuck on the process: what to evaluate, what to offer, and what to watch out for before signing anything.

That’s exactly what this blog covers. I will take you step by step through the whole process, in 8 easy-to-follow steps, starting with locating the right business and ending with the deal.

Why buy an existing business (instead of starting a new one)?

The biggest advantage that first-time buyers overlook is that an existing business can cover your salary and debt service from day one. You don’t have to wait months or years to reach profitability, as the cash flow is already there.

For lenders, that matters too. Banks and SBA lenders are far more willing to finance an acquisition than a startup because the risk is visible and measurable. There’s a track record, real revenue, and proof that the market works for this business. A startup has none of that.

That’s the other thing buying gives you: market validation you didn’t have to pay to test. The customers are already there. The pricing works. The location or channel is proven. You’re not gambling on whether demand exists. You’re evaluating a business that already answers that question.

Starting from scratch still makes sense in some situations. If you have a genuinely new concept, can’t find a business that fits your criteria, or want full control from day one, building your own is the right call. But if an existing business fits your goals, you’re starting with something that already works.

The first thing you need to get straight before you begin to browse through listings of businesses is what type of business will make sense to you.

Step 1: Decide what kind of business to buy

Begin with a position. Will it be a business needing day-to-day operation, or can it operate with an existing team? A lot of small businesses are very owner-dependent, and SBA loan-supported acquisitions are frequently participatory. When that is not your availability, it weeds out many options at the outset.

Budget is the second filter. And it’s not just the asking price. Factor in working capital, deal fees, and a buffer for the first few months. If you have $350,000 to work with, you’re realistically shopping in the $250,000-$300,000 listing range, not $350,000. Know that before you start.

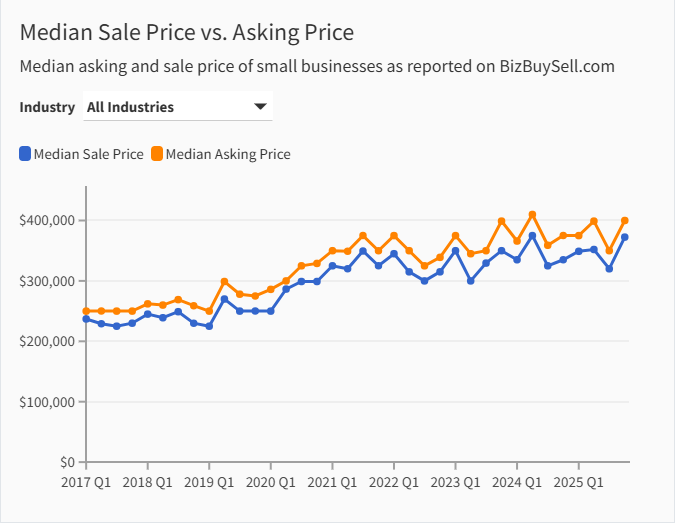

Then narrow by scope: location, size, and complexity. The operation of a single-location service business is very different than a multi-location one. According to the Insight Report of BizBuySell, the median price of the sale of any small business is approximately $350,000, which provides a good reference point of what most first-time buyers will eventually consider.

All this can be put in a one-page buyer profile before you even open a single listing:

- Position: Manager or owner-operator?

- Budget: Full picture, not just the asking price.

- Location: Local only, or open to relocating?

- Size and complexity: One location or multiple? Team in place or solo operation?

Once those filters are set, every listing becomes a screening exercise based on defined criteria.

One criterion that often gets overlooked at this stage is the type of business itself. Buying an independent business gives you full control over how it runs. Franchising sits in the middle: you get an established brand, a proven system, and built-in support, but you operate within the franchisor’s rules.

If you’re drawn to that model, it’s worth understanding the FTC’s Franchise Rule early, which requires franchisors to share a Franchise Disclosure Document before you sign anything. This guide on writing a franchise business plan is a good place to start.

Use this startup costs calculator to get a realistic picture of what you’ll need beyond the purchase price.

Step 2: Find businesses for sale

There are thousands of businesses available at any given time. The trick is what channel to look in and what each channel actually provides. The vast majority of purchasers turn to a combination of three: online marketplaces, direct outreach, and brokers.

1) Online marketplaces

BizBuySell, BizQuest, and BusinessesForSale.com are sites that pool listings by industry and geography. You can filter by location, industry, annual revenue, and asking price in all 3, which means that it is easy to create a shortlist that actually fits your criteria.

The listings tend to be high-level, though. Financials are summarized, and a few remain active even with an ongoing deal. Never put time into any listing without checking on the availability.

2) Business brokers

Brokers operate in the same way as real estate agents. They have access to numerous off-market deals, and they do the initial screening and communication between the two parties. A majority will charge a 10-12% commission on the price of sale, and in most instances, that will be borne by the seller, not you.

I would refer brokers when you want to have curated opportunities and a more organized process. That said, brokers represent the seller. Their job is to close the deal, so your own independent evaluation still matters. You can find certified brokers through the International Business Brokers Association (IBBA).

3) Direct outreach and networking

Somewhere between 20-30% of businesses sell off-market. The owners are usually keen on silent sales to prevent disturbing employees or clients, and these are not featured on any platform.

The way to find them is through relationships. Make direct outreach to business owners, collaborate with accountants and lawyers that advise sellers, participate in industry events, and network with your local chamber of commerce. It is harder to negotiate, but it generally involves less competition and improved terms.

Step 3: Evaluate the business

The first conversation with the seller or broker should cover four areas. Here are the questions I’d ask in each:

Financials

- Can I see three years of tax returns and profit and loss statements?

- What does the add-back schedule look like?

- Is revenue growing, flat, or declining, and what’s driving that?

Operations

- What percentage of revenue comes from your top three customers?

- Does the business depend on you personally to run day-to-day?

- Are there any key employees, supplier contracts, or systems I should know about?

Reason for selling

- Why are you selling now, and what’s your timeline?

- Have you tried to sell before?

Growth potential

- What would you do differently if you were staying?

- Are there opportunities you haven’t pursued yet, and why?

This is your first-call script before spending a dollar on due diligence. Watch for these early: inconsistent financial records, reluctance to share basic details, sudden revenue drops, or anything that doesn’t line up across documents and conversations. The goal at this stage is to decide whether it’s worth moving forward with due diligence.

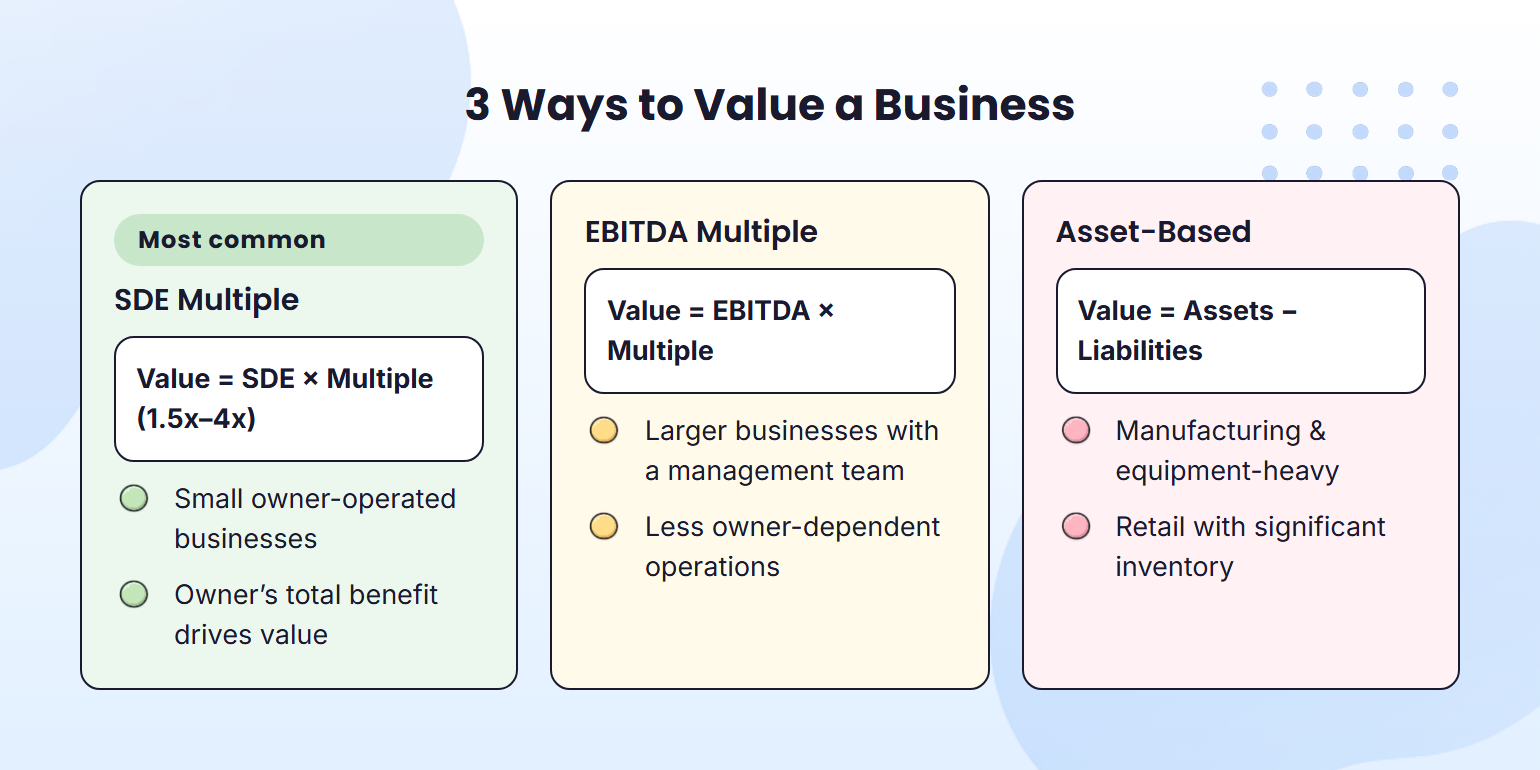

Step 4: Value the business

The asking price is just a starting point. Valuation is what tells you whether that number actually makes sense and what you should offer. For small business acquisitions, three methods are commonly used.

1) SDE multiple (most common)

Seller’s Discretionary Earnings (SDE) represents the total financial benefit to the owner. This is the widely used method for small business acquisitions.

Business value = SDE × multiple

For small businesses, multiples typically range from 1.5x to 4x, depending on industry, stability, and risk. For example, if a business generates $120,000 in SDE and the industry multiple is 2.5x: Value = $120,000 × 2.5 = $300,000

What I’d point out here is that the asking price you see on a listing is rarely what the business actually sells for. Transaction data consistently shows a gap between asking prices and final sale prices.

This gap is where negotiation happens. In most cases, buyers don’t pay the full asking price, especially when risks or dependencies surface during evaluation.

2) EBITDA multiple

This method is used for larger businesses with management teams in place and less owner dependency.

Business value = EBITDA × multiple

Multiples here depend on scale, margins, and how independently the business runs without the owner.

3) Asset-based valuation

This method applies when the business value comes primarily from its physical assets, common in manufacturing, retail, or equipment-based operations.

Business value = total assets − liabilities

For deals above $500,000, I’d recommend getting a professional valuation. Small errors in assumptions can lead to significant pricing differences at that level.

| Method | Formula | Best For |

| SDE Multiple | SDE × Multiple (1.5x-4x) | Small owner-operated businesses |

| EBITDA Multiple | EBITDA × Multiple | Larger businesses with management teams |

| Asset-Based | Total Assets − Liabilities | Asset-heavy businesses (manufacturing, retail) |

Step 5: Perform due diligence

When buying an existing business, it is important to verify everything the seller told you, not just what’s on the surface. The due diligence process of small business acquisitions takes 30-90 days. In this window, you examine finances down to the last detail, look at legal risks, and find out about operational dependencies.

Most deals collapse at this point, as the reality is not what was projected. Divide it into four regions:

| Category | What to check | Why it matters | Red flag |

| Financial | 3 years of tax returns, P&L, cash flow | Confirms real profitability | Numbers don’t match across documents |

| Legal | Licenses, contracts, pending lawsuits | Ensures compliance and ownership clarity | Expired licenses or unresolved disputes |

| Operational | Employees, suppliers, key processes | Reveals dependency on the owner or staff | One person controls critical operations |

| Market | Customer mix, competition, trends | Tests long-term viability | Over-reliance on 1-2 customers |

Majority of the problems are usually revealed by financial checks. See past revenue and look at consistency. Check costs, pinpoint one-time costs, and learn about add-backs: costs that the current owner incurs in the business that will not happen with you as the new owner.

Legal and operational checks focus on risk transfer. Can leases be transferred? Are supplier contracts stable? Are there obligations that carry over after the sale? These details affect both valuation and deal structure.

I’d also recommend looping in the right professionals at this stage. An accountant reviews financial quality, an attorney handles legal structure and contracts, and in some cases, an industry expert helps assess operations. Each one protects a different part of the deal.

Financing adds one more requirement to the list.

Step 6: Secure financing

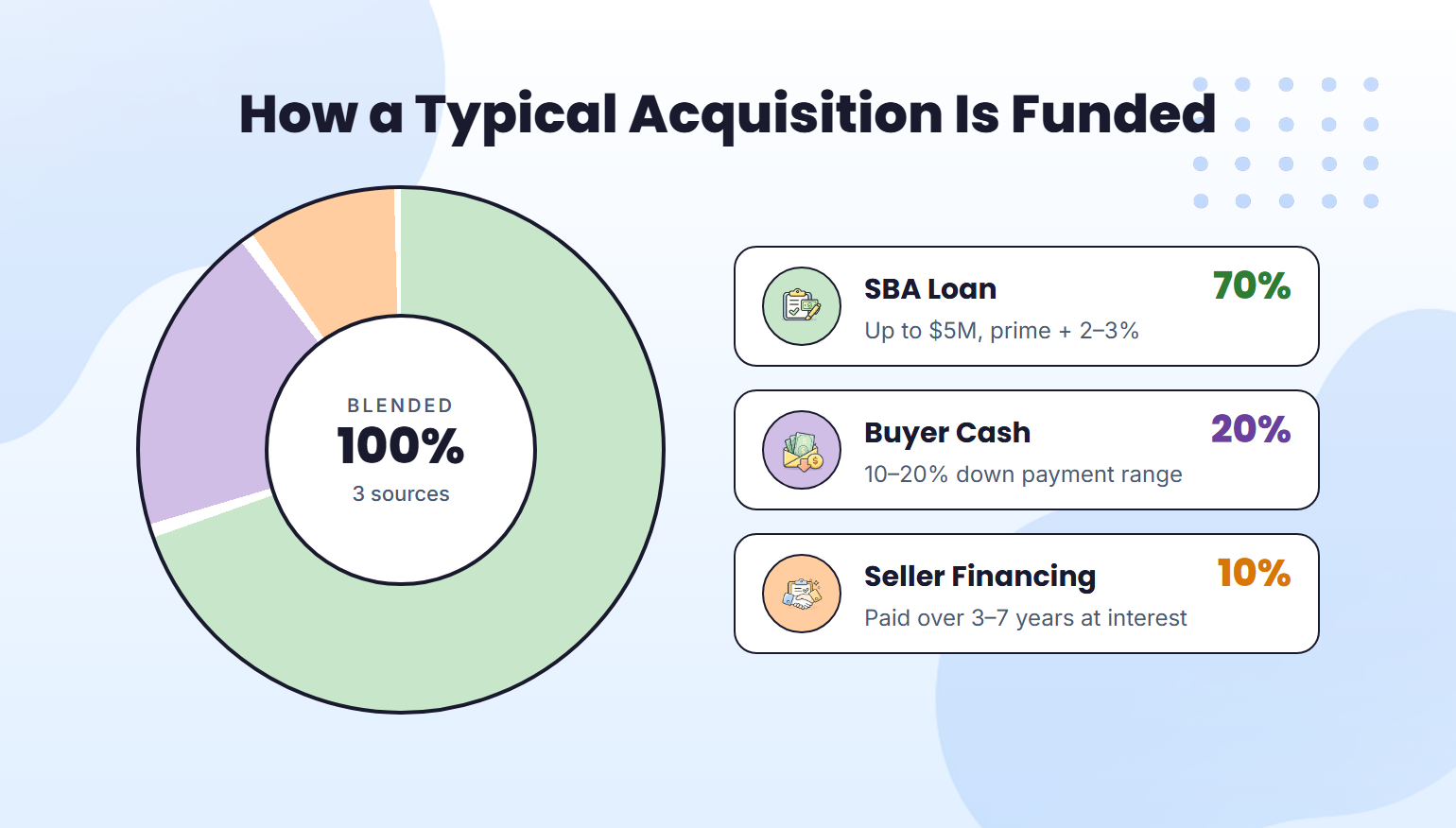

Most buyers don’t pay cash for a business; rather finance it. Once the numbers make sense, the next question is how the deal gets funded. Understanding your funding options early gives you more leverage in the negotiation and affects everything from your monthly cash flow to how much cash you put in upfront.

There are three primary options worth knowing.

SBA loans for business acquisition

SBA 7(a) loans are the most common financing option for buying a small business. They allow financing up to $5 million with down payments as low as 10-20%, and interest rates tied to the prime rate plus a small margin, currently in the range of prime + 2-3%.

The key requirement is involvement. SBA expects you to actively run the business, and lenders require a business plan showing how the business will perform after acquisition. If you want a passive investment, this isn’t the right vehicle.

For a detailed breakdown of eligibility and the application process, read our guide on SBA loans to buy a business.

Do you need a business plan for SBA financing?

Yes, and sooner than most buyers expect. Lenders require a business plan before approving financing. They want to see how the business will operate post-transition, how risks will be managed, and how the loan will be repaid.

Even without a loan, I’d recommend writing one. A business plan for buying a business forces clarity around projections, operations, and growth strategy before you commit to the deal.

Seller financing

First-time buyers underestimate how common seller financing is. The seller, rather than taking the full amount at closing, is paid in installments, usually over a period of 3-7 years at a specified rate of interest. This reduces your upfront cash requirement and keeps the seller invested in a smooth transition.

This is also how buying a business with little to no money becomes possible. A deal structured with seller financing combined with earnouts can significantly reduce, or in some cases eliminate, the cash needed at closing, particularly when the business has stable and predictable cash flow.

Conventional loans and investor partnerships

Conventional bank loans are another option, but they typically require stronger financials and higher down payments of 20-30%. Investor partnerships can also work, where one party provides capital and the other runs the business day to day.

In practice, most deals use a combination. It spreads risk across all parties and makes deals easier to close.

Can you buy a business with no money down?

Rarely, but it’s possible. Usually, buyers assume they need a large cash down payment. The reality is that deal structure can reduce, or in some cases eliminate, the cash needed at closing.

Three structures make this work:

- 100% seller financing: The seller acts as the lender, and you pay them over time. This works when the seller is motivated, and the business has stable, predictable cash flow.

- SBA loan + seller note: SBA loans require 10-20% down, but that gap can sometimes be covered by seller financing.

- Earnout agreement: You pay part of the purchase price from future revenue after the sale. This ties the seller’s payout to actual performance and reduces your upfront cash requirement significantly.

Zero-money deals are the exception, not the rule. But knowing these structures exist gives you real leverage in any negotiation.

Before you apply for SBA financing

Build the acquisition plan your lender expects

Step 7: Negotiate and close the deal

The aim now is to strike a deal that captures the true value of the business and cushions you against the dangers that may not always present themselves on the surface.

The process moves in three steps.

Letter of intent (LOI)

The LOI is an informal letter indicating the essential conditions: price of purchase, structure, timeframe, and conditions. It sets the direction for the deal without locking either side in legally.

Purchase agreement

This is the binding contract that defines exactly what’s being bought and under what terms. Key areas to negotiate:

- Purchase price and structure (cash, financing, or earnouts)

- What’s included in the sale (assets, inventory, customer lists, brand)

- Non-compete clause (prevents the seller from opening a competing business)

- Transition period (how long the seller stays to train and support)

Typically, small business deals are structured as asset purchases, not stock purchases. This lets you acquire selected assets without inheriting unknown liabilities tied to the business entity. According to the SBA, understanding the legal structure of the deal is one of the most important steps in any acquisition.

Before finalizing terms, I’d also recommend revisiting your target market assumptions. The type of customer base you are getting must be the same as the market that you intend to serve in the transition.

Closing

Closing is where everything becomes official. The purchase price is wired or delivered via certified funds, and both parties sign the bill of sale and assignment documents transferring ownership of assets, contracts, and intellectual property.

At the same time, any lease assignments or UCC-1 filings are completed to ensure a clean title transfer. Once everything is signed and funds are confirmed, the seller hands over keys, login credentials, vendor contacts, and operational access.

The timeline from LOI to closing typically runs 30-90 days. SBA-financed deals tend to run longer due to the loan approval process.

Before you get to this point, hire a business attorney. The purchase agreement defines long-term obligations, and small details can carry significant financial consequences.

How long does it take to buy a business?

Usually, deals take 3-12 months from first search to closing. Here’s how that typically breaks down:

| Phase | Timeline | What happens |

| Search | 1-3 months | Define criteria, browse listings, and shortlist candidates |

| Evaluate & Value | 1-2 months | Initial conversations, financial review, and valuation |

| Due Diligence & Financing | 1-3 months | Deep-dive verification, loan application, business plan |

| Negotiate & Close | 1-2 months | LOI, purchase agreement, closing documents |

| Total | 3-12 months |

SBA-financed deals run toward the longer end. Cash deals and smaller acquisitions can close faster. The biggest variable is usually financing.

Step 8: Plan your transition

Getting the deal to a close is a milestone, but not the finish line. The initial 90 days will dictate whether the business will continue its momentum or begin to lose it, and the choices you make in the first 90 days will be the way the rest of it is going to be.

The point is that you do not need to alter everything, but stabilize, comprehend, and improve afterward.

There are three priorities to focus on immediately.

- Retain key employees: they understand how the business is actually operating, and losing them early leaves gaps that may be difficult to fill.

- Maintain customer relationships: even a single hiccup in the flow of service or communication can give rise to churn at a rate that you could not anticipate.

- Learn the operations thoroughly: what appears easy on the surface frequently has dependencies manifested only in day-to-day use.

This is where the seller’s transition period earns its value. Most deals include 30-90 days of seller support, where they stay involved to train you, introduce key contacts, and explain how things actually work. I’d recommend using it every day.

A simple 90-day plan helps structure this phase:

- Days 1-14: Observe and learn. Don’t make changes yet.

- Days 15-30: Meet key employees, suppliers, and customers.

- Days 31-90: Start making gradual improvements based on what you’ve learned.

A useful framework here is the 70/30 rule from SCORE: spend 70% of your focus on improvements you can make to the business, and 30% on understanding what the seller has already done with it. It keeps progress moving without disrupting what’s already working.

Conclusion

Buying a business is a significant decision, but with a clear process, it becomes manageable. Determine your standards, locate the right deal, assess it fairly, do due diligence, raise funds, and seal the deal on terms that favor you.

The biggest mistake first-time buyers make isn’t paying too much; it’s not having a process to follow. Now you do.

Start with Step 1 and work through each stage in order. If you need help building the business plan that SBA lenders require, Upmetrics’ business plan builder walks you through the entire acquisition plan, from financial projections to operational strategy, so you’re ready before you ever walk into a lender’s office.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

Can you buy a business with no money?

How much does it cost to buy a small business?

Is buying an existing business a good idea?

Do I need a business plan to buy a business?

How long does it take to buy an existing business?

How much is a business worth with $100,000 in sales?

Joe Onderko

Joe Onderko is a manufacturing and business management expert with over 35 years of experience in operations, product development, and leadership. He’s worked with global companies in the consumer products, automotive, and industrial sectors, helping them modernize operations, improve efficiency, and grow stronger. He also writes about manufacturing, leadership, and smart business strategy. Read more