Most business owners I’ve talked to have been sitting somewhere between “This is working” and “I want to expand” for months. What’s holding them back isn’t doubt.

It’s the fear of getting the execution wrong and damaging the business they’ve spent years building.

That fear is legitimate.

I’ve seen profitable businesses with real demand and genuine opportunity run into serious trouble during expansion. Not because the idea was wrong. But because they consider the planning as a formality rather than a decision to think through.

That’s why I built this guide. It walks you through whether the expansion makes sense, what it will cost, when it pays off, and what happens if things don’t go as expected.

But before that…

Is your business ready for expansion? (or is it not)

Not every business that wants to expand is actually ready to.

Most of the time, genuinely profitable businesses make this mistake, and it’s rarely about bad intentions. It’s about moving before the foundation is solid enough to support the weight of expansion.

Run through these six signals honestly before you commit:

- Your net profit has been consistent for 12 or more months, you have 3-6 months of operating expenses sitting in reserve, and your current debt load still leaves room for an expansion loan.

- You’re turning away customers regularly, not just during peak season. And that pattern has held across at least two consecutive quarters.

- Core operations are documented, and at least one person can handle daily decisions without calling you for every one of them.

- Your competitive advantage isn’t tied exclusively to your current location or existing relationships. It changes with the business.

- Your vendors can scale with you, and your technology and supply chain won’t buckle under increased demand.

- You can genuinely give this expansion 50% of your attention for the next 12 months without the existing business suffering for it.

If four or more of these apply, you’re in a good position to move forward. Just ensure that financial readiness and consistent demand are the two you can’t skip. The rest are important but flexible.

Ask yourself: Does the expansion make financial sense?

Here’s where I’d pause before moving forward. Those six signals tell you the business is operationally ready. What they don’t tell you is whether the financial timing is right, and that’s the part most owners skip.

There are really two numbers worth calculating here:

- Can you afford to start the expansion?

- Can your existing business carry the expansion’s costs long enough for the new location or product line to start paying for itself?

Most owners only calculate the first one. That second number matters more.

Every expansion runs at a loss before it breaks even. That monthly shortfall has to come from somewhere. If it comes from your existing business’s operating cash, a slow start at the new location doesn’t just hurt the expansion. It starts pulling the existing business down with it.

And that’s the risk worth understanding before you commit.

A good rule of thumb: Your reserves should cover at least 9 to 12 months of expansion operating costs, separate from what you need to keep the existing business healthy.

If that number isn’t there, you probably need more capital before you expand. You don’t need a better plan right now.

Do you need a separate plan for expansion? (or existing one is fine)

Once you’re confident the business is ready for expansion, the planning work ahead is more manageable than most owners expect.

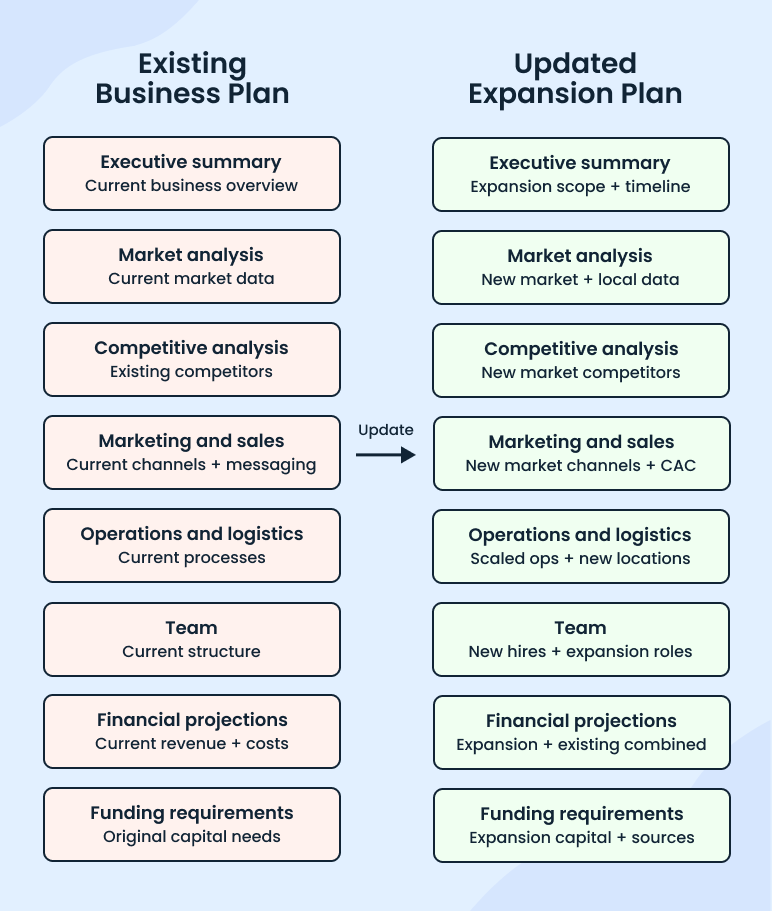

You don’t need a separate plan for expansion. The business plan sitting on your desktop, the one you wrote when you first launched, is already most of what an expansion plan requires. It just needs to be updated, not replaced.

The only situation where I’d recommend a separate plan is if the expansion is a completely different business entity or requires an entirely new strategy. Even Franchise expansions are the exception since franchisors typically require a standalone document for FDD compliance.

But that’s not the case for most small business owners.

How to use your existing plan to plan your expansion?

Your existing business plan is the baseline. It tells the story of where the business started, what the market looked like, what the financials were built around, and the operations you’ve put in place.

For expansion, that baseline becomes your reference point. No need to rewrite it.

Each section gets updated to reflect the bigger version of the business you’re building without losing the foundation that’s already there.

What should a business expansion plan include?

An expansion business plan needs to cover the new market you’re moving into, updated financial projections, the operational changes ahead, and how you’re funding it all.

But here’s what I always tell business owners: Understand who’s going to read it, because that shapes how you write every section.

Different readers come to this document with completely different questions:

- A lender wants confidence that the expansion pays for itself without putting the existing business at risk.

- An investor wants a credible growth opportunity worth backing and a team capable of executing it.

- Your internal team just wants to know what’s changing, what’s staying the same, and what you’re all working toward.

A solid business development strategy plan answers all three, regardless of who’s sitting across the table.

Now, let’s get clear on one thing: What kind of expansion are you actually planning for?

5 Types of expansion strategies for your business (structured comparison)

Of course, what you put in an expansion business plan depends entirely on how you’re expanding. Not every expansion looks the same.

A restaurant opening a second location and a SaaS company adding a new product line are both expanding. But they’re solving completely different problems, carrying completely different risks, and need completely different plans.

The strategy you pick shapes every section of your strategic expansion plan. So before you start updating anything, get clear on which direction you’re actually going.

Here are the five main expansion strategies:

1. Market penetration

This means expanding without really leaving your comfort zone. You’re growing revenue from the market you already operate in, same customers, same geography, just more of it.

A gym adding personal training packages to existing members is market penetration. Low risk, lower capital, and your business plan changes are relatively minimal.

2. Geographic expansion

You’re taking what works in your current location and opening up somewhere new. Let’s say a retail store is opening a second location across town, and a cleaning business is moving into a neighboring city.

The business model is proven. The challenge is replicating it without the owner being everywhere at once. A solid location strategy is what separates a well-chosen expansion market from an expensive mistake.

3. Product/service expansion

You’re adding new offerings for your existing customers. For example, an accounting firm adding tax planning services or a coffee shop adding a catering menu.

You already have the relationship. You’re just deepening it. Medium risk because you’re introducing something new, but your customer base is already there.

4. Diversification

This is the highest-risk move on this list. You’re entering a new market with a new product or service, which means you’re starting from scratch on two fronts simultaneously.

A restaurant chain launching a packaged grocery line sold in supermarkets is a classic example. I’d only recommend this if the other three strategies have genuinely run their course.

5. Acquisitions and partnerships

Buying another business or forming a formal partnership to accelerate growth. A marketing agency is acquiring a web development firm to offer full-service packages.

Acquisitions move faster than building from scratch, but require significantly more capital and due diligence. Partnerships carry less risk but less control.

Here’s how all five compare side by side:

| Strategy | Risk Level | Capital Required | Timeline | Best For |

| Market penetration | Low | Low to medium | 3 to 6 months | Businesses with strong local demand that haven’t fully captured their existing market. |

| Geographic expansion | Medium | Medium to high | 6 to 12 months | Businesses with a proven model ready to replicate |

| Product or service expansion | Medium | Low to medium | 3 to 9 months | Businesses with strong customer relationships and repeat buyers |

| Diversification | High | High | 12 to 24 months | Established businesses with strong cash reserves and risk appetite |

| Acquisitions and partnerships | Medium to high | High | 6 to 18 months | Businesses looking to grow faster than organic growth allows |

Once you know which strategy fits your situation, updating your business plan becomes a much more focused exercise. You’re not changing everything. You’re changing the right things.

Now it’s just a matter of knowing which sections to touch and how.

Strategy picked? Next step is the plan.

Let AI rewrite each section for your expansion

How to turn your business plan into an expansion plan (You don’t need a new one)

I’ll be honest, this is the part most owners either rush through or avoid entirely. But getting each section right is what separates a plan that holds up in front of a lender from one that raises more questions than it answers.

Here’s how to update each section of your existing business plan:

Revisit your executive summary

Most owners write the executive summary first. For an expansion plan, write it last.

Every other section needs to be updated before this one, because the executive summary is a reflection of everything that follows, not an introduction you write in advance.

Once the rest of the plan is updated, come back to this section and rewrite it to reflect the expansion specifically.

- What are you expanding into? Where and why now?

- How much will it cost? And what’s the expected return?

- What does the business look like 12 to 24 months from now if the expansion goes as planned?

One thing I always tell business owners at this stage: Lenders often decide whether to keep reading after the executive summary. If it doesn’t show the opportunity and the financial upside in the first half page, the rest of the plan may never get a second look.

Lead with the opportunity, follow with the numbers, close with why this business is positioned to execute it.

Update your market analysis

Your existing market analysis was written for the business you had at launch. But for expansion, it needs to cover the new market you’re entering, not just the one you already operate in.

If you’re expanding geographically, this means researching the new location specifically:

- Local demographics

- Foot traffic patterns

- Income levels

- Demand indicators specific to that area

National data doesn’t cut it here. The U.S. Census Bureau is one of the most underused free tools for this. You can pull local population data, income levels, and household spending patterns by zip code in minutes.

For instance, a coffee shop expanding from Portland to Phoenix is entering a completely different customer behavior and competitive environment.

If you’re adding a product or service, the market analysis needs to include customer research for that new offering. Answer:

- Who specifically is buying it?

- What are they currently using instead?

- Is there enough demand to justify the investment?

One thing I see owners often skip: Regulatory differences between markets. Licensing requirements, zoning laws, and employment regulations vary significantly from one state or city to another.

Revise your competitive analysis

Your existing competitive analysis mapped the competition in your current market. While expanding, that map changes, sometimes completely.

New market, new competitors. The businesses you’ve been competing against for years may have no presence in your expansion market at all. Or they may already dominate it.

Either way, you need to find out before you write this section, not after you’ve committed.

What I’d focus on here: Don’t just list who the competitors are in the new market. Understand specifically why customers choose them over alternatives and whether your competitive advantage actually holds up in that context.

A restaurant that wins on neighborhood loyalty and years of word-of-mouth doesn’t automatically carry that advantage into a new city.

One thing worth adding that most owners don’t think to include: What happens if your current competitors follow you into the new market?

If your expansion is successful enough to notice, they may. Acknowledging that scenario in your plan and having a response to it signals to lenders and investors that you’ve thought this through properly.

Adjust your marketing and sales strategy

Your existing marketing strategy was built around customers who already know you. In a new market, you’re starting from zero name recognition. That changes how you approach this section entirely.

The channels that work in your current location may not work in the expansion market. A business that grows through referrals and repeat customers in one city can’t rely on that in a new place.

Think about how you’re acquiring your first 50 customers in a place where nobody has heard of you yet.

If you’re expanding a product line rather than a location, the focus shifts to launch marketing:

- How are you introducing the new offering to existing customers?

- What does the sales process look like for something they haven’t bought from you before?

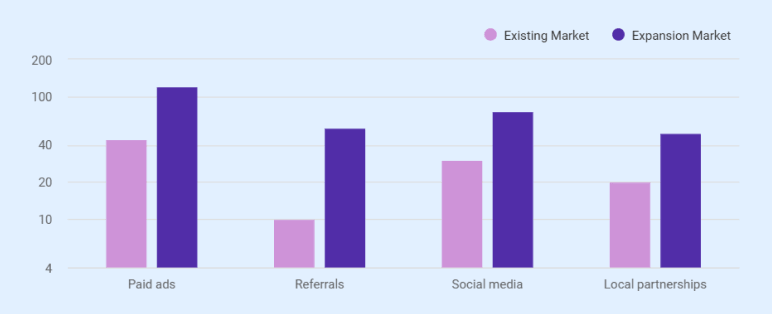

Something I find most owners underestimate: Customer acquisition costs in a new market are almost always higher than in an existing one.

The example below gives you a rough sense of how different the gap can be across channels, though your actual costs will vary depending on your industry and location.

Take the same coffee shop expanding from Portland to Phoenix. Here’s how customer acquisition costs compare across the main marketing channels:

| Channel | Existing Market (Portland) | Expansion Market (Phoenix) |

| Paid ads | $45 | $120 |

| Referrals | $10 | $55 |

| Social media | $30 | $75 |

| Local partnerships | $20 | $50 |

Budget for that here, not just in the financials. A lender who sees that you’ve accounted for the cost of building a customer base from scratch will take the plan more seriously than one that assumes growth happens organically.

Before finalizing this section, spend 30 minutes with a local business owner in the expansion market.

If required, SCORE.org connects you with free mentors who’ve operated in specific markets and industries. What works where you are now often doesn’t translate directly, and that conversation can save months of wasted budget.

Plan your operations and logistics

The operations plan is the section most owners underwrite in an expansion plan.

The financials get attention, the market analysis gets attention, but the mechanics of actually running a bigger business often get a paragraph when they need a page.

What changes here depends on your expansion type.

If you’re opening a new location, this section needs to cover the lease or build-out timeline, equipment requirements, and how you’re maintaining quality across two sites simultaneously. That last part is harder than it sounds.

Most quality control systems in small businesses are informal and owner-dependent. Expansion forces you to make them explicit.

If you’re adding a product or service, the focus shifts to production capacity and supplier relationships:

- Can your current vendors handle increased volume?

- Do your contracts allow for it?

In my experience, supplier capacity is one of the most overlooked checks in this process. Talk to your top vendors before you finalize anything. Finding out they can’t scale after you’ve committed is an expensive lesson.

Also, don’t forget to include technology systems in this section. The tools running your current business, inventory, point of sale, and scheduling were built for one location.

Before you expand, check whether they can handle two. Switching systems mid-expansion is expensive and disruptive.

Build your expansion team

The team section is where a lot of expansion plans fall apart in practice, not on paper. Owners write down the roles they need, hire for them after the expansion launches, and then spend the first six months doing two jobs at once.

The honest question to answer in this section is: Who runs the existing business while you’re focused on building the new one?

If the answer is “me,” that’s a problem worth solving before you expand, not after.

For a new location, think through the management structure specifically: Do you need a location manager? Or can you split your time between both sites?

I’d recommend hiring for that role before the expansion opens, not once it’s already struggling without leadership. That hire alone changes how the whole expansion runs.

For a product or service expansion, the hiring needs are different, but the principle is the same.

Figure out who owns the new offering day to day, who handles customer issues, and who reports to whom. Writing that structure down before you hire forces clarity that most teams skip until there’s a problem.

Create expansion financial projections

This is the most important update in your entire business expansion plan. Everything else builds the case. This section proves it.

The mistake I see most often here: Owners project expansion revenue using the same assumptions as their existing business. A new location or product line rarely performs at the same level in year one.

Build your projections separately from your existing business financials, and be conservative on the revenue side.

At least, your projections need to cover 12 to 24 months and include three things lenders look at first:

- Projected revenue from the expansion

- All expansion costs (broken into one-time and ongoing)

- A cash flow projection (for both the existing business and the new one)

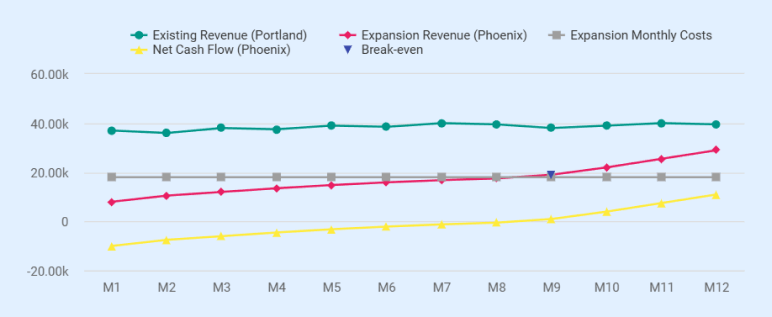

For better understanding, let’s use the same example: A coffee shop expanding from Portland to Phoenix. Before the Phoenix location opens, the one-time costs alone look like this:

One-time expansion costs (Phoenix location):

| Item | Cost |

| Lease deposit + first 3 months rent | $28,000 |

| Equipment and fit-out | $42,000 |

| Initial inventory | $6,000 |

| Pre-opening marketing | $4,000 |

| Staff hiring and training | $8,000 |

| Total one-time costs | $88,000 |

Most owners only account for these upfront costs and stop there. The ongoing monthly costs are what catch them off guard.

One number most owners leave out of this section is the break-even month, and that’s what lenders expect to see. Not the year, the specific month when expansion revenue starts covering its own costs.

It’s the important number that shows more financial literacy than three pages of projections.

Here’s what that looks like month by month for the same Portland to Phoenix coffee shop expansion:

12-month cash flow projection:

| Month | Existing Revenue (Portland) | Expansion Revenue (Phoenix) | Expansion Monthly Costs | Net Cash Flow (Phoenix) |

| Month 1 | $37,000 | $8,000 | $18,000 | -$10,000 |

| Month 2 | $36,000 | $10,500 | $18,000 | -$7,500 |

| Month 3 | $38,000 | $12,000 | $18,000 | -$6,000 |

| Month 4 | $37,500 | $13,500 | $18,000 | -$4,500 |

| Month 5 | $39,000 | $14,800 | $18,000 | -$3,200 |

| Month 6 | $38,500 | $15,900 | $18,000 | -$2,100 |

| Month 7 | $40,000 | $16,800 | $18,000 | -$1,200 |

| Month 8 | $39,500 | $17,500 | $18,000 | -$500 |

| Month 9 | $38,000 | $19,000 | $18,000 | +$1,000 |

| Month 10 | $39,000 | $22,000 | $18,000 | +$4,000 |

| Month 11 | $40,000 | $25,500 | $18,000 | +$7,500 |

| Month 12 | $39,500 | $29,000 | $18,000 | +$11,000 |

Month 9 is when the Phoenix location crosses break-even, generating $19,000 against $18,000 in monthly costs. What this doesn’t show is the full picture.

The net cash flow across all 12 months comes to -$11,500. Add that to the $88,000 in one-time startup costs, and the total first-year investment is approximately $99,500.

Monthly break-even is a milestone, not a finish line. That’s the number lenders actually want to see accounted for in your expansion plan.

Detail your funding requirements

This is the section that turns your expansion plan into a pitch document. Every section before this one builds the case. This section tells the reader what you need and exactly what you’re going to do with it.

Start with the total capital required. Break it into two buckets:

- One-time costs like build-out, equipment, and initial inventory

- Ongoing costs like rent, payroll, and marketing for the first 12 months.

Lenders want to see that you’ve thought beyond the launch costs. Then cover your funding sources.

Are you using an SBA loan, a line of credit, retained earnings, or a combination?

If you’re approaching a bank, I’d recommend checking the best SBA lenders before your first meeting.

Most lenders require at least 10% owner equity contribution, which is the SBA minimum per their standard operating guidelines, with some lenders requiring up to 20% depending on the loan type and your financial profile.

SBA.gov also has a clear breakdown of available loan programs and exactly what lenders require from your business plan before approving any application.

I would even recommend including a line-by-line breakdown of the use of funds. Not just the total number, but where every dollar goes specifically. It’s the first thing a lender asks for and the last thing most people prepare.

With all eight sections updated, there’s one more step before this plan is ready to present.

Read the plan straight through as a single document. And check whether every section supports the same expansion decision. If any section breaks that thread, revise it before moving forward.

Testing if your expansion makes financial sense

A well-written plan can still have weak numbers. Before you walk into a lender meeting or commit resources, it’s worth pressure-testing the financials specifically.

I know from experience that plans can read well, tell the same story, and still fall apart within the first year. Almost every time, the problem wasn’t the strategy. It was numbers that looked reasonable on paper but hadn’t been stress-tested against what could actually go wrong.

The Federal Reserve’s Small Business Credit Survey consistently highlights cash flow as one of the most common financial challenges small businesses face. And more than half of the firms had a plan but cited uneven cash flows as an ongoing issue.

That said, run these four financial tests against your projections to ensure the numbers are solid:

Break-even analysis

Calculate exactly when the expansion starts covering its own costs. The formula is straightforward:

Fixed costs ÷ (Revenue per unit − Variable cost per unit)

For most new locations, a realistic break-even timeline is 12 to 18 months, though this varies significantly by industry. If your numbers show longer than that, it doesn’t mean you don’t expand. It means you need more capital buffer going in.

Cash flow stress test

Project your cash flow for the first 12 months, assuming revenue comes in 30% slower than expected. Then ask: Can your existing business cover that shortfall without putting itself at risk?

If the answer is no, you need more capital before you expand, not a more optimistic revenue projection.

Scenario planning

Build three versions of your financial projections, but don’t treat them equally. Most owners spend 80% of their time on the best case and rush through the worst. I’d flip that.

Here’s how to define each scenario:

- Best case: Revenue hits projections, costs stay within budget.

- Expected case: Revenue comes in 15% below projections, costs run 10% over.

- Worst case: Revenue comes in 40% below projections, costs run 20% over, and launch is delayed by 3 months.

The worst case is where the real planning happens. Once you’ve built it, define what triggers a pivot or exit. Having that answer before you expand is what separates a plan from a real decision.

ROI timeline

When does the expansion pay back the total investment?

Payback timelines vary by expansion type. For most small business expansions, a realistic range is 2 to 4 years, though capital-intensive expansions like opening a new location often run closer to 3 to 5 years.

Anything beyond 5 years needs a strong strategic justification, not just optimism.

If your numbers pass all four tests, you have a financially sound expansion plan. If any test fails, go back to the financial projections section and adjust before moving forward.

Plan successful expansion through efficient planning

Now that you’ve gone through this guide, you know exactly what your expansion plan needs. But putting it all together is a different challenge entirely. Market research, financial plan, competitive analysis, operational details. They all need to connect.

Change one number, and suddenly you’re updating three different documents. It gets messy fast, and that’s usually where good plans stall.

That’s where Upmetrics makes a big difference. Its AI assistants help you draft and update every section of your expansion plan, from market analysis to operations plan and financial projections, all in one place, with less manual effort.

If you’re serious about getting your expansion off the ground, don’t let the business and financial planning process slow you down.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

What is an example of a business expansion?

How do I choose the right expansion strategy for my business?

I'm profitable, but not sure I have the cash for expansion. What should I do first?

How long does it take to create a business expansion plan?

What's the difference between a business growth plan and a business expansion plan?

How do I keep my team from getting overwhelmed during expansion?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more