Fashion still looks like one of the most attractive industries to enter. But size alone doesn’t make a market easy.

Most fashion stats tell you the market is huge. The harder thing they leave out is that almost none of that market is actually yours. Your real opportunity sits at the intersection of one category, one customer, and one or two channels you can actually run. If you get that intersection right, the trillion-dollar number doesn’t really matter. And if you get it wrong, even a perfect product won’t move.

So the real question we would be asking is, “Where does my brand fit in this market today?”

That’s what we’ve pulled together below: apparel and fashion industry statistics for 2026, covering market size, e-commerce, consumer behavior, tariffs and AI, sustainability and resale, and what it all means for founders like you.

TL;DR: fashion in 2026 at a glance

The fashion industry is still huge, but 2026 isn’t a simple “start a brand and ride the growth” kind of year. Here’s the quick read before you scroll:

- The global apparel market is on track to hit about $1.92 trillion this year, with the US making up roughly $373 billion of it (the biggest country-level market in the world). (Statista)

- Online is still the lane to watch. Global fashion e-commerce is heading for about $957 billion in 2026, growing nearly twice as fast as the overall apparel market. (Statista)

- Ask any fashion executive what’s keeping them up at night, and you’ll probably hear one word: tariffs. 76% of them call it the #1 issue of 2026. (McKinsey/BoF State of Fashion 2026)

- And AI isn’t a side conversation anymore. McKinsey projects generative AI could add $150-275 billion in profit to the fashion, apparel, and luxury sectors over the next 3-5 years. (McKinsey)

Apparel industry statistics: Market size and growth in 2026

If you’re writing a fashion business plan in 2026, these are the numbers to defend before you talk about your niche, pricing, or growth strategy. The pace has changed. McKinsey’s State of Fashion 2026 reads bleaker than anything since 2022, and the trade map has been redrawn enough that your sourcing and tariff exposure now hinge on which country your manufacturer sits in.

- Global apparel growth has slowed to about 2.7% year over year in 2026, and the US market is moving even slower at 1.9%. (Statista)

- 46% of fashion executives expect industry conditions to worsen in 2026, up from 39% in 2025. (McKinsey/BoF State of Fashion 2026)

- China’s share of US apparel imports has fallen by roughly one-third since 2019, with Cambodia, Vietnam, and Bangladesh picking up much of the slack. (McKinsey/BoF State of Fashion 2026)

- Greater China is now closing in on the US as the largest fashion market globally, a shift Statista’s analysts flagged years before tariffs put it on the front page. (Statista)

- 25% of fashion executives expect conditions to improve in 2026, up from 20% in 2025, signaling a small but growing camp of leaders who see opportunity in the slowdown. (McKinsey/BoF State of Fashion 2026)

- “Challenging” has overtaken “uncertain” as the word executives use most to describe the industry in 2026, after years of treating volatility as a temporary condition. (McKinsey/BoF State of Fashion 2026)

- Personal luxury goods spending declined roughly 1–3% in 2025 to about €358 billion, the segment’s weakest year since the post-pandemic period, with a projected return to 3–5% growth in 2026 as US, European, and Middle Eastern markets recover. (Bain-Altagamma Luxury Study 2025)

- US apparel inflation has accelerated sharply in early 2026, with apparel CPI running 4–5% year-over-year against a headline CPI of 2.4–4.2%, as tariff costs that retailers absorbed through 2025 finally flow through to consumers. (BLS Consumer Price Index)

- Within athleisure, premium and performance lines are projected to grow at 10.45% CAGR through 2031, outpacing mass-market segments by roughly 3-4 percentage points as consumers prioritize fewer, higher-quality pieces. (Mordor Intelligence Athleisure Market Report 2026)

- Lululemon plans to expand its China store base from 100 to 220 by the end of 2026, while entering India in late 2026 via a franchise partnership with Tata CLiQ—both moves signal premium athleisure brands prioritizing emerging-market entry as US growth slows. (Arizton Sportswear Market Report 2026)

Fashion e-commerce and social commerce

If the overall fashion market is growing slowly, the online slice isn’t. It’s where the growth is, where the competition is, and where most first-time fashion founders are now expected to build the brand from day one rather than as a “channel.”

Here’s what the online side of fashion looks like in numbers.

- Global fashion e-commerce revenue is projected to reach about $957 billion in 2026, on its way to $1.16 trillion by 2030. (Statista)

- The global social commerce market is projected to reach close to $1 trillion in 2026. (Research and Markets)

- AR-powered virtual try-on has cut return rates for adopting fashion brands by 40–50% on average, with live shopping in fashion converting at 10% versus 30–35% for standard fashion e-commerce. (Coresight Research 2026, via Easy App Ecom)

- NRF estimates 19.3% of online sales will be returned in 2025, with apparel among the most exposed categories. (NRF 2025 Retail Returns Landscape)

- US social commerce sales are projected to cross $100 billion for the first time in 2026, an 18% jump over 2025. (eMarketer)

- TikTok Shop generated about $15.8 billion in US sales in 2025, more than double the prior year, and is projected to hit over $23 billion in 2026. (eMarketer)

- US livestream e-commerce sales grew nearly 50% in 2025 to $14.64 billion, with the US live shopping market projected to reach $55 billion by 2028 as creator-led streams convert at 9–30% compared with 2–3% for standard e-commerce. (eMarketer livestream commerce insights 2026)

- About 67% of US consumers buy through social media at least once a month, with apparel and accessories the single largest social commerce category. (SellersCommerce)

- TikTok Shop captured 18.2% of total US social commerce in 2025, while Instagram Shopping converts at 2.1% versus TikTok Shop’s 4.7%—a 2.6x gap that’s reshaping where fashion brands invest their creator and ad budgets. (eMarketer 2026 forecast, via SQ Magazine)

- The fashion industry has some of the highest revenue-per-visit figures in e-commerce, with activewear at $3.29, active footwear at $2.74, and handbags and luggage at $2.73 per visit. (Shopify Fashion E-commerce Report 2026)

- Online retail is growing 3x faster than overall athleisure (11.36% CAGR vs ~3-4% for the broader category), making digital channels the primary distribution mode for new athleisure entrants by 2031. (Mordor Intelligence Athleisure Market Report 2026)

The fashion startups we’ve seen launch well in 2026 build the whole brand around it, and assume from day one that customers will arrive informed, comparison-shopped, and ready to leave if anything feels off. If you want the broader online retail picture beyond fashion, our roundup of 80+ e-commerce industry statistics covers conversion benchmarks, channel splits, and category breakdowns worth modeling against.

Who’s buying: consumer behavior and spending

The 2026 fashion consumer has gotten sharper than the version from even two years ago. They compare across more brands, sit on purchases longer, dig into reviews, and quietly judge whether the price actually matches what they’re getting.

A nice-looking product doesn’t carry the weight it used to if the fit, quality, return policy, or reason to trust the brand isn’t obvious. Gen Z, in particular, doesn’t move through a neat funnel anymore. They discover, validate, compare, save, ask, and come back, often across five or six touchpoints before they ever click buy.

- US households spent an average of $2,001 on apparel and services in 2024, down from $2,041 in 2023, even as total household spending rose nearly 2%. That’s about $167 a month, and the dip points to a more cautious US consumer. (BLS Consumer Expenditure Survey 2024)

- Nearly half of global consumers (45%) now use AI during their buying journey, and shopping-related generative AI use grew 35% between February and November 2025, as discovery, research, and purchase compress into a single nonlinear loop across social feeds, AI chatbots, retailer apps, and in-store experiences. (eMarketer 2026 path-to-purchase analysis)

- 73% of US Gen Z say social media is their main source for learning about new products, and Gen Z is 42% more likely than older generations to buy holiday gifts through social media. It’s a sign that an algorithm-driven loop is replacing the traditional discovery-to-purchase funnel. (eMarketer 2026 forecast, via SQ Magazine)

- Buy Now, Pay Later accounts for about 6% of US e-commerce value in 2025 and is forecast to grow at 13% annually through 2030, with fashion, beauty, and lifestyle categories driving the highest adoption. (Worldpay Global Payments Report 2026)

- Around 60% of consumers say they’ll seek more affordable options like resale if prices keep rising. Sustainability isn’t a vague brand value to this customer; it’s a price and value calculation. (McKinsey/BoF State of Fashion 2026)

- 82% of consumers now say free returns are a major factor when shopping online, up from 76% the year before, and Gen Z averages 7.7 online returns a year, more than any other generation. (NRF 2025 Retail Returns Landscape)

- 51% of Gen Z consumers say they bracket purchases, buying multiple sizes of the same item with the plan to return what doesn’t fit, which is the biggest driver of fit-related returns in apparel. (NRF 2025 Retail Returns Landscape)

- 76% of consumers say they’re more likely to choose a return option that offers an instant refund or exchange, putting pressure on small brands to match what Amazon and ASOS already offer. (NRF 2025 Retail Returns Landscape)

- 9% of all retail returns are now classified as fraudulent, ranging from empty box returns to wardrobing to counterfeit swaps, a cost that hits apparel especially hard. (NRF 2025 Retail Returns Landscape)

- Fashion influencer marketing alone was worth $6.82 billion in 2024 and is projected to reach $39.72 billion by 2030, growing at 33.8% CAGR, among the fastest-growing channel investments in the entire marketing landscape. (Grand View Research Fashion Influencer Marketing Market Report)

The 2026 fashion consumer isn’t just younger or more digital. They’re more careful, more research-driven, more influenced by social proof, and more aware of trade-offs. The brands that understand this will sell.

The forces reshaping fashion in 2026 (Tariffs, AI, supply chain)

Ask a fashion executive what makes 2026 difficult, and the answer isn’t softer demand or online competition. It’s the pressure sitting underneath the business: tariffs eating into margins, sourcing costs climbing, supply chains rerouting, and AI moving from “explore later” to “ship this quarter.”

The two forces worth founder-level attention are tariffs (because they hit unit economics directly) and generative AI (because it’s the rare lever where a small brand can move as fast as a big one). Supply chain pressure sits underneath both.

Tariffs and trade

- US apparel and footwear tariffs spiked from around 13% in early 2025 to 54% in April, then settled at a 36% weighted average by mid-October, well above historical norms. (McKinsey/BoF State of Fashion 2026)

- Tariffs have raised first costs on apparel and leather goods by roughly 35%, according to McKinsey, which is a hit no amount of marketing efficiency can recover on its own. (McKinsey/BoF State of Fashion 2026)

- 45% of fashion executives now name sourcing costs as the single most pressured part of their economic model, followed by pricing and inventory management. (McKinsey/BoF State of Fashion 2026)

- US imports from Cambodia have risen 42% since 2019, while imports from China have fallen 30%, showing how decisively brands are rerouting sourcing away from tariff-exposed origins. (McKinsey/BoF State of Fashion 2026)

Generative AI

- 92% of fashion organizations plan to increase their generative AI investment in 2026, even as overall budgets get tighter. (McKinsey/BoF State of Fashion 2026)

- 35% of fashion executives already use generative AI for customer service, image creation, copywriting, or product discovery, and that share is growing fast. (McKinsey/BoF State of Fashion 2026)

- Shopping-related searches on generative AI platforms grew about 4,700% between 2024 and 2025, which is starting to reshape how people discover products before they ever land on a brand site. (McKinsey/BoF State of Fashion 2026)

- 85% of US retailers are now deploying AI to detect and prevent returns fraud, one of the more measurable ways AI is already paying for itself in apparel. (NRF 2025 Retail Returns Landscape)

- Fashion executives now identify AI and digital capabilities as the single biggest opportunity for the industry in 2026, ahead of product differentiation, sustainability, and customer service. Up to 90% of AI initiatives, however, still fail to scale beyond the pilot phase. (McKinsey/BoF State of Fashion 2026)

- Only about 1% of companies across industries describe their gen AI implementations as fully mature, which means the 92% of fashion brands planning to invest are still mostly experimenting. That gap is a real opening for fast-moving small brands willing to ship before the giants do. (McKinsey “Superagency in the Workplace”)

- Almost half of all consumers, about 48%, now use AI tools at some point during their shopping journey, with apparel and accessories the second-most popular category for AI-assisted research. (Shopify Fashion E-commerce Report)

Supply chain pressure

- 60% of large US fashion companies sourced from 10 or more countries in 2025, up from 45-55% in 2022 and 2023, as brands deliberately spread risk across more suppliers and geographies. (USFIA Fashion Industry Benchmarking Study)

- Inditex, the parent company of the world’s biggest fashion player Zara, now makes over half its volume in nearby markets to the EU, reflecting how seriously the big players are taking nearshoring to offset tariff risk and lead-time. (Strategy& Fashion Retail Outlook 2026)

- According to Vogue Business, there are four forces on top of one another shaping 2026 supply chains: Tariffs, Climate disruption (floods and droughts affect raw materials), changing sourcing maps, and a new wave of due diligence and traceability laws. (Vogue Business)

Counterfeits and IP risk

- Global trade in counterfeit goods was valued at approximately $467 billion in 2021, accounting for 2.3% of total global imports, with clothing, footwear, and leather goods collectively making up 62% of all seized counterfeit shipments worldwide. (OECD-EUIPO Mapping Global Trade in Fakes 2025)

- Around 65% of counterfeit goods seizures globally now involve small parcels and mail shipments, reflecting how counterfeiters exploit cross-border e-commerce and direct-to-consumer logistics to bypass traditional bulk-shipping enforcement. (OECD-EUIPO Mapping Global Trade in Fakes 2025)

Avoid basing your business plan on the lowest possible price for your products. Build it on real supplier quotes, current tariff exposure, freight assumptions, realistic return rates, and a second sourcing option in case your first one breaks.

Tariffs and AI are pulling fashion in opposite directions. One is making the business more expensive to run. The other is making parts of it cheaper to operate than they’ve ever been.

The brands we’ve seen handle 2026 well are the ones treating both as line items in the model, not as background conditions to react to later. For the wider context on what’s reshaping retail at large, see our breakdown of the top retail industry trends for 2026.

Sustainability, resale, and the circular economy

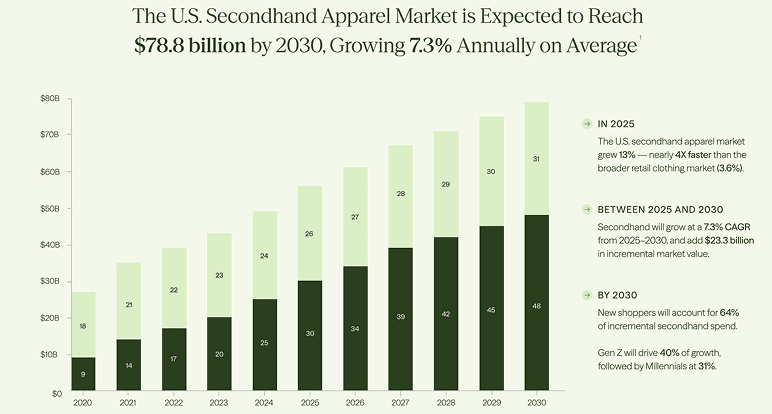

Sustainability stopped being a brand-values conversation around the time global secondhand crossed $289 billion in 2026. Resale isn’t a side hustle anymore. It’s a category, growing at roughly twice the rate of the broader apparel market. (ThredUp 2026 Resale Report)

- The US secondhand market grew 13% in 2025, nearly four times faster than the broader retail clothing market at 3.6%, and is set to reach $78.8 billion by 2030. (ThredUp 2026 Resale Report)

- Gen Z and Millennials will drive 71% of resale market growth through 2030, with 62% of Gen Z having shopped secondhand in 2025. (ThredUp 2026 Resale Report)

- 48% of people now use AI tools when shopping second-hand, and 46% use social media, content creators, or in-person shopping when purchasing second-hand products. (ThredUp 2026 Resale Report)

- Textile production accounts for an estimated 2–8% of global greenhouse gas emissions and is one of the largest industrial water users in the world, drawing the equivalent of 86 million Olympic-sized swimming pools a year. About 60% of clothing material is made from plastic-based fibers, and washing synthetic clothes releases roughly 500,000 tonnes of microfibres into the ocean every year, the equivalent of almost three billion polyester tops. (UNEP)

- Less than 1% of clothing material is recycled back into new clothing globally, which is why most “circular” claims still need careful scrutiny before they make it into a brand story. (Ellen MacArthur Foundation)

- The EU’s revised Waste Framework Directive came into force in October 2025, introducing common rules for extended producer responsibility (EPR) on textiles. In plain terms, brands selling into Europe are now on the hook for what happens to their products after the customer is done with them. If you sell only into the US, this doesn’t apply to you yet, but it’s a strong signal of where US state-level rules (California’s SB 707 textile EPR law starts taking effect in 2030) are heading. (European Commission)

- 36% of US retailers now view resale as a hedge against inventory and supply chain volatility, with 72% of consumers saying rising prices are directly affecting their apparel spending and 27% planning to increase their secondhand purchases as a result. (ThredUp 2026 Resale Report, via Retail TouchPoints)

- 60% of customers now say resale value is a key factor when buying new apparel (a 13-percentage-point jump year-over-year), and 49% of younger consumers have already stopped buying low-quality items because they can’t be resold. (ThredUp 2026 Resale Report, via Retail Brew)

- Luxury watch resale is forecast to capture 35–40% of the global watch market by 2030, with secondhand already accounting for 28% of luxury fashion wardrobes overall and 32% of Gen Z wardrobes globally (rising to 66% in the US). (BCG x Vestiaire Collective: Resale’s Next Chapter (October 2025))

- The global sneaker resale market is projected to reach $30 billion by 2030, growing at a roughly 15% CAGR from a $6 billion base in 2019, with Nike and Jordan models accounting for nearly 70% of the secondary market’s total value. (Hype Proxies / Industry Research 2026)

Employment and the biggest fashion companies

Fashion’s employment shape is lopsided. The bulk of the workforce sits in production (mostly Asian, mostly female), while a much smaller pool of creative, design, and corporate roles lives in the US and Europe. For early-stage founders, that’s why most lean teams run on freelancers and contractors rather than in-house staff.

The revenue side is even more concentrated. A handful of global groups dominate sales, supplier access, and shelf space, and they’re the brands investors and lenders will quietly benchmark your plan against.

- The median annual wage for fashion designers in the United States was $80,690 in May 2024, with employment projected to grow just 2% from 2024 to 2034 and about 2,300 openings each year on average. (US Bureau of Labor Statistics)

- About three-quarters of US fashion designers are women, with the largest concentration of jobs based in New York. (BLS Labor Force Statistics from the Current Population Survey)

- The US has approximately 72,800 people employed in the apparel manufacturing sector as of May 2026, down from a peak of nearly 1 million in the 1990s, with most production now in Asia and Latin America. (BLS / FRED Apparel Manufacturing Employment)

- LVMH alone employs more than 211,000 people globally, nearly three times the entire US apparel manufacturing workforce of around 72,800. One luxury group now has more headcount than every American clothing factory combined, which is the clearest single picture of how concentrated fashion has become at the top. (LVMH 2025 Annual Results)

- The global sneaker market reached approximately $99-104 billion in 2025 and is projected to grow to $137-160 billion by 2034, with North America holding ~30-38% of the market and Asia-Pacific the fastest-growing region. (Grand View Research Sneakers Market Report 2026)

- Nike and Adidas together control approximately 57% of the global sneaker market in 2025, with Nike’s footwear sales reaching ~$33 billion and Adidas at ~$13 billion. For new footwear brands, that concentration is the structural reality before any product decision gets made. (IMARC Group Sneaker Market Report 2026)

What these numbers mean for fashion founders

We curated this resource for founders building in the fashion industry, and for those thinking over whether or not this is the right market to enter in 2026. The numbers show definitely a big market, but (honestly) not a very easy one to enter.

- Growth has been slower

- Tariffs are rising amidst a geopolitical crisis

- Return rates are increasing

- Social commerce pressure’s there

- AI is leading the discovery

- The resale market is growing like never before

This all changes how the industry has operated so far, and how fashion brands survive. For active and aspiring founders, the takeaway is simple:

- Pick a narrow (niche) lane before chasing the whole market

- Build around social discovery; a website is just not enough in 2026.

- Price with tariffs, returns, freight, and supplier risk included.

- Treat resale, sustainability, and AI as business choices. (Don’t ignore)

A strong plan should connect your category, customer, sourcing model, sales channel, and margin assumptions. That is what’d turn these statistics into a real business decision.

Conclusion

Fashion in 2026 isn’t short on opportunity. It’s short on easy assumptions. The market is still large, but growth is slower. Digital channels are stronger, but more crowded. Resale, sustainability, tariffs, and AI aren’t side topics anymore. They shape how a fashion business gets priced, sold, sourced, and planned.

The question you opened this guide with (“Where does my brand fit in this market today?”) isn’t one a stat sheet can answer for you. It’s the one you’ll answer when you turn these numbers into a real plan.

If you want to keep tracking the industry on your own between roundups like this one, our list of free and paid sources of industry reports is the same one we use to refresh these pieces.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

What is the current global market value of the fashion industry?

Which age group is most interested in fashion?

What are the most popular fashion categories among consumers?

What are the most popular fashion brands globally?

How many people work in the fashion industry?

Upmetrics

Upmetrics is the #1 business planning software that helps entrepreneurs and business owners create investment-ready business plans using AI. We regularly share business planning insights on our blog. Check out the Upmetrics blog for such interesting reads. Read more