Most first-time entrepreneurs don’t know this exists, and honestly, that’s the whole problem.

There are nearly 1,000 Small Business Development Centers across the US offering free, one-on-one business consulting. Business plans, loan prep, market research, and financial projections covered. No fees, no income requirements, no catch. The same guidance that would cost you $75 to $200 an hour from a private consultant? Available to you right now, at no cost.

In this piece, I’ll walk you through what SBDCs are, what they actually help with, and how to get the most out of your first visit.

What is a Small Business Development Center (SBDC)?

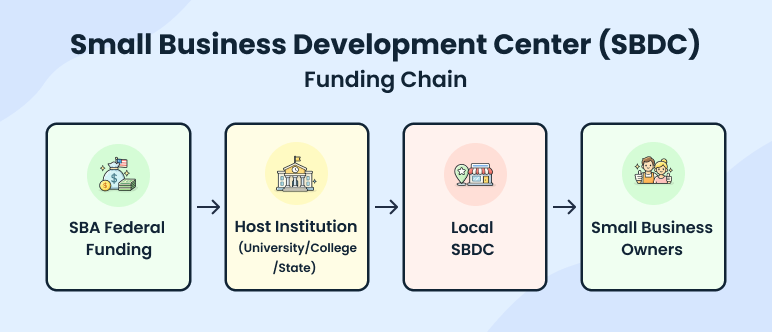

An SBDC is a free business advising center funded by the US Small Business Administration and hosted by local universities, colleges, or state agencies. There are nearly 1,000 of them across all 50 states and US territories, and most people have never heard of them.

Here’s how it works. The SBA provides federal funding, a local university matches it and hosts the center, and local advisors use that support to help small business owners like you directly.

That structure is why it’s free. Nobody is charging you because the government and your local institution have already covered it.

Each center is staffed by paid advisors, often supported by volunteers from banks, trade associations, and SCORE. As one of the SBA’s key resource partners, SBDCs are designed to deliver free one-on-one advising at the local level, through people embedded in your own business community, not a distant government office.

How is SBDC different from the SBA or SCORE?

The SBA is the federal agency that funds and oversees the SBDC program. Your SBDC is the actual office you walk into, with real advisors you sit down with.

For one-on-one business advising, your SBDC is where you go, not the SBA directly.

SCORE is a separate SBA partner that uses volunteer mentors, mostly retired executives. SBDCs have paid professional staff who go deeper on technical help, like loan packages and financial projections. Both are free. Both are useful. I’d say use whichever fits what you need right now.

What does an SBDC actually help you with?

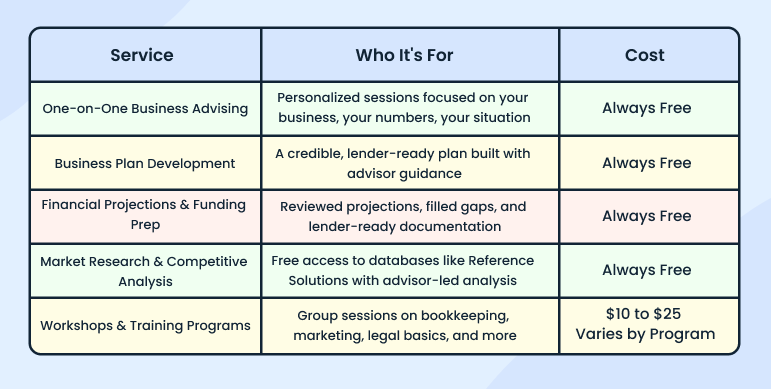

Here are the core SBDC services available at most centers. Whether you’re pre-launch or already operating, these are the areas where small business development center services make the biggest difference.

1) One-on-One business advising

It’s not a class, and it’s not a webinar. You sit down with an actual advisor, tell them where you’re at, and they help you work through it. Everything is specific to you, your business, your numbers, your situation. Unlike paying a consultant who bills by the hour, your SBDC advisor has no incentive other than helping you move forward.

2) Business plan development

This is where the SBDC business plan becomes invaluable. Most people either skip the plan entirely or write one that doesn’t hold up under scrutiny. SBDC advisors have reviewed hundreds of them. They know exactly where the weak spots are, and they’ll work through your section by section until it actually tells a credible story.

3) Financial projections and funding prep

This is where a lot of applications fall apart, not because the business is bad, but because the numbers don’t tell a clear story. Your advisor will go through your projections with you, fill the gaps, and make sure you’re not walking into a lender meeting underprepared.

4) Market research and competitive analysis

Here’s one people don’t expect. Many SBDCs give you free access to research databases like Reference Solutions (formerly ReferenceUSA), the kind that cost serious money to access on your own. In a typical session, your advisor pulls industry reports, competitor data, and customer demographics specific to your market and walks you through what it means for your business.

5) Workshops and training programs

Outside of one-on-one advising, most centers run group sessions on things like bookkeeping, marketing, and legal basics. Some are free. A few have a small fee. But the content is always practical, built for people actually running businesses, not studying them.

Now that you know what SBDCs offer, the next question most people ask is whether any of it actually costs anything.

Is SBDC help really free? (What’s the catch?)

SBDC free consulting covers everything from business plans to market research. Here’s the full breakdown:

As I mentioned earlier, the funding model is what makes this possible. The SBA covers it at the federal level, your state or local government matches it, and the host institution fills the rest. That’s what keeps small business free consulting available to you at no cost.

And just to be clear, this isn’t charity. SBDCs are a public resource, the same way a public library is. You’ve already contributed to it through taxes. You’re just using what’s available to you.

Who is it actually for: New businesses or existing ones?

Short answer: almost everyone. SBDCs are open to any US citizen or legal resident who owns or plans to start a for-profit small business. You don’t need to be registered yet or have a certain revenue level.

It doesn’t matter if you’re still in the idea stage, have been running for ten years, or fall somewhere in between. If you can’t afford a private consultant, that’s exactly who this program was built for.

The only businesses SBDCs don’t serve are large corporations, publicly traded companies, and nonprofits. If you’re a for-profit small business owner or aspiring entrepreneur, you’re in.

Special programs for specific groups:

Women-owned businesses can access programs through Women’s Business Centers (WBCs), veteran-owned businesses through Veterans Business Outreach Centers (VBOCs), and minority-owned businesses may qualify for support with the SBA’s 8(a) program, which opens doors to government contracting. Ask your local center what’s available for your situation.

If you’re working on a research-based startup, some SBDCs also run SBDC FAST programs specifically for SBIR and STTR grant applicants.

Most centers will ask you to fill out a short intake form before your first meeting. It’s not a barrier. It just helps them match you with the right advisor.

How do SBDCs help with business plans and funding?

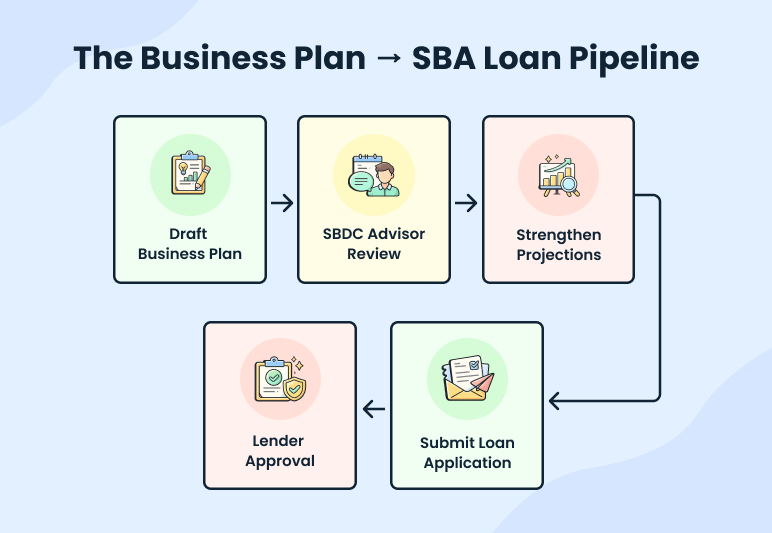

One of the most common fixable reasons entrepreneurs get turned down for SBA loans is a weak business plan.

Most first-time founders write a plan that shows strong profits and wonder why the bank still says no. Here’s why: lenders don’t fund based on profit. They fund based on cash flow, because that’s the only thing that proves you can actually repay the debt.

An SBDC advisor knows how to look at your numbers through the eyes of a risk-averse lender. They catch the cash flow gaps you’d never think to look for and help you fix them before a bank ever sees the plan.

They go through your plan the way a lender does. Are your revenue assumptions realistic? Does your cash flow show you can service the debt? Are your management credentials presented in a way that builds confidence?

SBDC advisors are often former bankers or deeply connected to local lenders. They know exactly which local bank is currently aggressive in funding certain industries and which ones are pulling back.

They can act as a matchmaker. More importantly, they know the specific red flags that will get a business plan rejected by an underwriter. Having an advisor review a loan package before it goes to the bank drastically increases the chances of approval.

There’s also something called loan packaging. That’s the process of gathering every document a lender needs and making sure it all tells one coherent story. A lot of applications get rejected simply because something is missing or formatted incorrectly.

For startups, this gets tricky. You have no historical revenue, so your projections have to do all the work. SBDC advisors are used to building realistic first-year forecasts from scratch. That’s one of the most valuable things they do for early-stage businesses.

I’d recommend showing up with a first draft already in progress. That way, your advisor doesn’t have to waste time teaching you basic formatting. Instead, they can spend the entire session doing what they do best: stress-testing your cash flow.

Use Upmetrics’ business plan software to structure your first draft before you walk in, and their financial projection templates are a solid starting point if the numbers feel overwhelming.

If you’re specifically targeting an SBA loan, your advisor will help you meet the exact documentation standard lenders expect. They can also point you toward SBA-approved lenders in your area or help you explore SBA loan options if your credit isn’t perfect.

When your plan is ready, your SBDC advisor can refer you directly to SBA-approved lenders, CDFIs, and microloan programs in your area. It’s not just advising. It’s a referral network.

How to find your local SBDC (and what to do first)

Finding your center takes about a minute. Head to AmericasSBDC.org, drop in your zip code, and your nearest location comes up. Call or email them, tell them what you’re working on, and book your first appointment.

That’s the easy part. What actually moves the needle is what you do before you walk in.

What to bring to your first SBDC meeting

A business summary or idea outline. Even a few bullet points on your phone is enough. Your advisor needs something to react to, so give them that.

Any financials you already have. Messy spreadsheets, rough estimates, old bank statements. Bring whatever exists. Don’t wait until the numbers look presentable.

Your specific questions. Are you trying to figure out loan readiness? Get your business plan reviewed? Work on your marketing? Know what you’re walking into so the session doesn’t drift.

Your advisor will point you in the right direction and catch things you missed. But nobody is going to build this for you. That part is on you.

How does the SBDC process actually work?

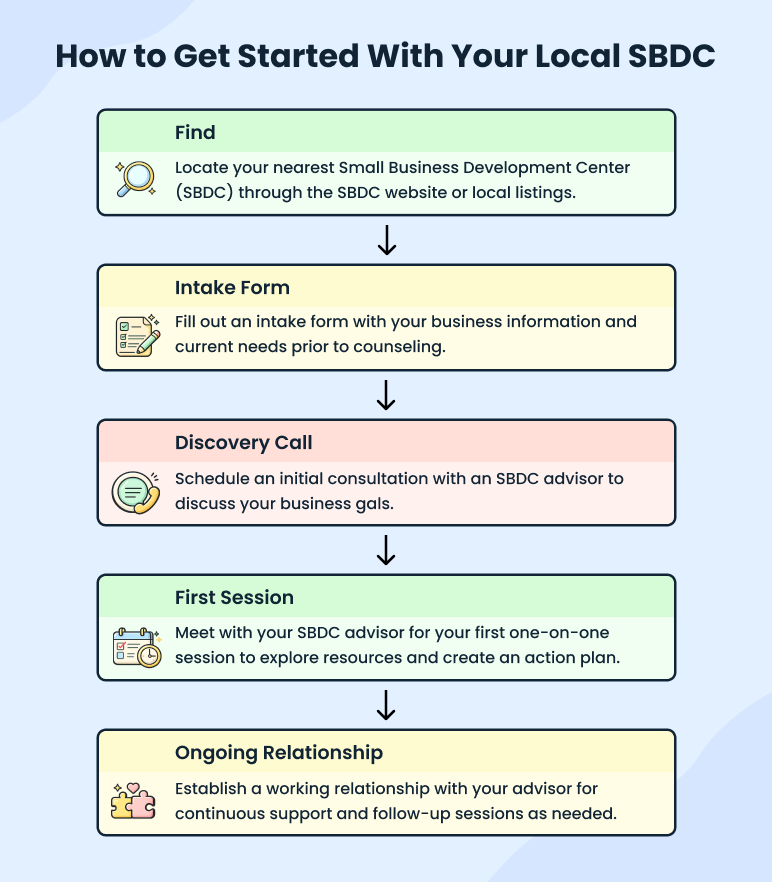

Most people who’ve heard of SBDCs never actually make an appointment. They’re not sure what to expect. Here’s exactly what happens from the intake form to the first session.

- Find your nearest center. Use the America’s SBDC locator, enter your zip code, and you’ll see every center in your area with contact details, hours, and services.

- Fill out a short intake form. Basic information about where you’re at, what your business is or will be, and what you need help with. This isn’t a screening process. It just helps them match you with the right advisor.

- Wait for a discovery call. Someone from the center will reach out to schedule your first session. They’ll ask a few questions about your priorities so your advisor can show up prepared.

- Your first session. Usually an hour, in person or on video. You walk through your situation, your challenges, what you’re trying to figure out. Your advisor gives you initial feedback and maps out the next steps together with you.

- An ongoing relationship. This isn’t a one-time thing. Most SBDC clients meet with their advisor multiple times over months. The relationship builds as your business does.

Conclusion

SBDCs are one of the most underused free resources available to small business owners in the US. In the last year alone, SBDCs assisted over 317,000 businesses, helped create more than 80,000 jobs, and secured $6.6 billion in capital. For every dollar of public funding invested, the program delivers a 10x return. Nearly 1,000 centers, staffed by real business experts, are sitting there waiting for you to show up.

SBDCs are one of the most underused free resources available to small business owners in the US. In the last year alone, SBDCs assisted over 317,000 businesses, helped create more than 80,000 jobs, and secured $6.6 billion in capital. For every dollar of public funding invested, the program delivers a 10x return.

So is it worth it? Honestly, I can’t think of a reason not to go.

You’re not paying anything. You’re not committing to anything. You’re sitting down with someone who has actually built businesses, knows what lenders want, and gets paid to help you figure this out. The only way you lose is by not showing up.

The entrepreneurs I’ve seen get the most out of it are the ones who come in with something already started. Build your business plan with Upmetrics before your first meeting, walk in with a draft, and let your advisor take it from there.

Nearly 1,000 centers are out there waiting. Find yours and get something on the calendar.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.