Getting an SBA loan isn’t just about filling out forms or choosing the first bank you know.

It’s about finding a lender who can work with businesses like yours, can move faster than a DMV clerk on a Monday morning, and won’t leave you stuck chasing updates for weeks.

Now, not all SBA lenders are the same.

Some lenders only take on clients with five years of financials. Others specialize in startups or service businesses. Some move in 30 days. Others take 90. (Yes, they’re picky 🤷🏽♀️)

This guide breaks down the best SBA lenders for you. Read on to understand what’s best for you.

What is an SBA loan?

An SBA loan is a small business loan backed by the U.S. Small Business Administration. Here, you don’t borrow money directly from the government. Instead, you apply through a participating lender, and the SBA guarantees a portion of that loan.

If a borrower defaults, the SBA covers the guaranteed portion. This reduces the lender’s risk and helps businesses qualify for better terms, like lower interest rates and longer repayment periods.

Types of SBA loans

Depending on how you plan to use the money, these are the different types of SBA loans you can avail of:

- SBA 7(a) Loan: Offers up to $5 million for almost any business need—working capital, refinancing, equipment, or even acquiring another business

- SBA 504 Loan: Provides long-term, fixed-rate financing of up to $5 million for major fixed assets like real estate or heavy equipment

- SBA Microloan: SBA-funded intermediaries offer up to $50,000 to small businesses and select nonprofit childcare centers to launch and grow their business

No need to navigate complex SBA loan requirements on your own

Get matched with the right SBA lenders and secure your desired funding

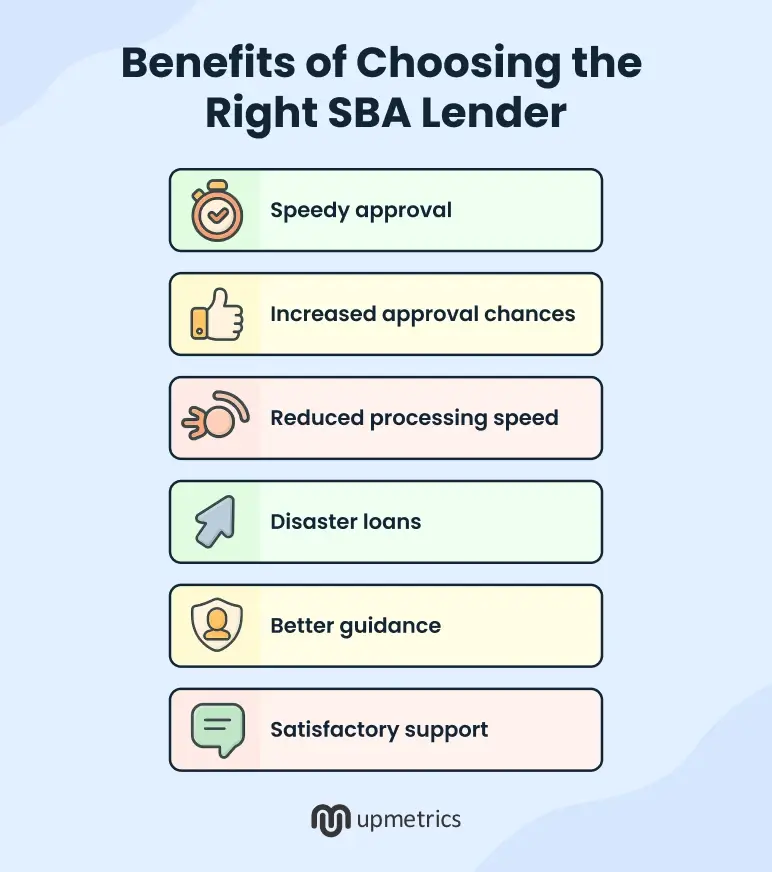

Why choosing the right SBA lender matters

Not all SBA-approved lenders are the same. In fact, choosing the right SBA lender can greatly impact your loan experience.

From making an application to getting approval (or rejection), here’s how lender selection plays an important role:

Speeds up the loan approval

High-volume SBA lenders usually have dedicated teams and faster systems. If they’re in the SBA’s Preferred Lender Program (PLP), they don’t need SBA approval on every loan, which means fewer delays and quicker decisions.

Increases the approval odds

Lenders set their own credit rules. Some want a score of 680 or higher, while others are flexible if the rest of your profile is strong. If your credit or business history isn’t perfect, picking the right lender can make the difference between an approval and a rejection.

Brings down the processing speed

SBA loans have a notoriously lengthy process, i.e., 2-3 months from funding application. For situations when you need quick access to liquidity, choosing a lender that prioritizes speed and automation can make a great difference.

Suitability with your industry and loan requirements

Some lenders focus on specific industries or loan sizes. That enables them to assess your application more quickly, ask the right questions, and expedite the process. But if your request falls outside their comfort zone, it can lead to delays or even rejection.

Customer service and guidance

SBA loans come with a lot of paperwork. A responsive lender who explains requirements and spots issues early can save you weeks. On the flip side, poor communication from lenders often leads to missing documents and unnecessary delays.

That said, when you find a lender that matches your strengths and requirements, it can ease the entire application and approval process.

Best SBA Lenders in 2026: Ranked & Reviewed

Let’s now evaluate the top SBA lenders of 2026. We have categorized them based on factors such as lending strength, friendliness to startups, processing speed, real estate expertise, and reputation so that you can zero down on your suitable choice.

1. Best overall SBA lenders

The best SBA lenders handle high volumes of loans, have a solid track record, and serve a wide range of businesses.

These are our overall top picks for the best SBA lenders:

Live Oak Bank

Live Oak Bank is one of the largest SBA lenders by dollar volume. For context, in FY 2024, Live Oak lent nearly $2.0 billion through the SBA 7(a) program

They specialize in higher-value loans, often supporting business acquisitions, real estate purchases, or expansion-heavy industries like healthcare and agriculture. As a preferred lender (PLP), they can process and close loans faster than many traditional banks.

Entrepreneurs often praise Live Oak’s streamlined digital application and knowledgeable loan officers for their ability to understand unique business models.

| Average loan size | $1.2 million |

| Approval time | Typically 3–4 weeks faster than non-PLP lenders |

| Industries served | Veterinary, pharmacy, healthcare, agriculture, and more |

| Notable features | Live Oak can approve loans without the SBA’s prior sign-off, meaning faster approvals |

Huntington National Bank

Huntington National Bank has been the nation’s top SBA 7(a) lender by number of loans for seven consecutive years. In fiscal year 2024, the bank approved over 7,500 SBA 7(a) loans, totaling approximately $1.5 billion in funding.

Huntington offers a range of SBA loan products, including SBA 7(a), SBA Express, and 504 loans. The SBA Express loans are designed for smaller amounts and feature an expedited review process, allowing quicker access to funds.

| Average loan size | $202,000 |

| Approval time | SBA Express loans can take up to 36 hours |

| Industries served | Retail or service local businesses |

| Notable features | “Lift Local Business” to support minority, women, and veteran-owned businesses with zero origination fees |

Newtek Small Business Finance (Newtek Bank)

Newtek Bank is ranked as the top SBA 7(a) lender by dollar volume in 2025, approving over $2 billion in loans across more than 3,100 transactions. They focus on established businesses with consistent revenue and at least two years of tax returns.

As a Preferred Lender Program (PLP) participant, Newtek can process SBA loans without prior SBA approval, expediting the funding process.

| Average loan size | $432,919 |

| Approval time | 3-4 weeks |

| Industries served | Healthcare, technology, and equipment financing |

| Notable features | Additional services like payment processing, payroll, and insurance |

ReadyCap Lending (Ready Capital)

Ready Capital is a nonbank SBA Preferred Lending Partner (PLP) and ranks among the top SBA 7(a) lenders by volume. They are known for their focus on commercial real estate and business acquisition loans, making them a popular choice for franchise buyers and property-heavy businesses.

Ready Capital’s flexible credit criteria and expedited processing cater to a broad range of borrowers. Their digital application process and national reach make them a strong option for businesses seeking SBA financing.

| Average loan size | $362,346 |

| Approval time | 2-4 weeks |

| Industries served | Franchises, assisted living, child care, dental services, and veterinary services |

| Notable features | Expedited processing for loans under $500K |

2. Best SBA lenders for startups

Securing an SBA loan as a startup (or very young business) is challenging – many lenders prefer at least 2 years in business.

However, a few founder-friendly lenders are willing to work with newer businesses and limited credit history.

Lendio

Lendio is an online loan marketplace that connects small business owners with a network of over 75 lenders, including banks, credit unions, and alternative financing companies. By submitting a single application, businesses can receive multiple loan offers tailored to their needs.

For SBA loans, Lendio usually requires at least two years in business, a 620+ credit score, and $8,000 in monthly revenue. Their application process is fast, and they only run a soft credit check during the initial match.

| Average loan size | Up to $5 Million |

| Approval time | 2-4 weeks to fund after approval |

| Industries served | 10-30 years |

| Notable features | 620+ |

Funding Circle

iBusiness Funding, now operating in place of Funding Circle U.S., offers SBA 7(a) loans tailored to small businesses seeking financing. They operate fully online and focus on giving small businesses easier access to SBA capital without the usual friction of big-bank processes. Their team is known for transparent communication and fast responses, which appeals to founders who want guidance without red tape.

| Average loan size | $30,000-$5 Million |

| Approval time | Up to 10 years |

| Industries served | 2-4 weeks |

| Notable features | 640+ |

Fundible

Fundible is a fintech lending platform that works with a wide network of lenders to offer SBA loans and alternative financing options. Unlike most banks, Fundible is open to newer businesses and borrowers with less-than-perfect credit.

For SBA loans, they generally look for businesses with $250K in annual revenue and at least one year in business.

Startups that fall short of these thresholds may still get matched with SBA microloan lenders or Community Advantage programs. The application is fully online and handled by a dedicated team that guides you through lender matches. If traditional banks have turned you down, Fundible is a solid next stop.

| Average loan size | Up to $10 Million |

| Approval time | 2-10 years |

| Industries served | 2-4 weeks |

| Notable features | 650+ |

Creditfy

Creditfy is a fintech lender that offers SBA loans and other financing options to small businesses. They are known for their lenient requirements, accepting businesses with as little as six months of operation and no revenue, provided the applicant has a personal credit score of at least 600.

While SBA loans typically require a demonstration of the ability to repay, Creditfy’s flexibility suggests they may consider startups in early stages, potentially pairing them with SBA microloan providers or lenders who accept strong personal guarantors.

| Average loan size | Up to $10 Million |

| Approval time | Up to 25 years |

| Industries served | 24-48 hours |

| Notable features | 650+ |

Although these lenders are startup-friendly, most of them require you to have some revenue or years in business to qualify.

For businesses with limited credit or revenue to support, consider applying for SBA Microloans or Community Advantage loans. These loans are specifically designed to serve new and underserved businesses.

3. Fastest SBA lenders

One of the biggest pain points with SBA loans is the time it takes. From loan application to approval and disbursal, the process takes around 60–90 days.

However, some lenders offer pretty quick SBA loan approvals. Like these fastest SBA lending options:

SmartBiz (online SBA loan marketplace)

SmartBiz is an online platform that connects small businesses with SBA-approved lenders to streamline the loan application process. SmartBiz pre-screens your application, packages it to SBA standards, and forwards it to a matched lender from its network of SBA Preferred Lenders.

This pre-underwriting cuts down delays and avoids common application mistakes. Many loans through SmartBiz are funded in as little as 30 to 45 days, which is nearly twice as fast as the typical SBA timeline.

SBA express lenders

Lenders with proficiency in SBA Express loan programs can dramatically speed up the approval process for smaller loan amounts. With SBA Express, the SBA issues a decision on its loan guarantee in just 36 hours, compared to the usual several weeks.

Banks like Huntington National Bank and Bank of America actively offer SBA Express options, often bundling them into working capital or line-of-credit solutions. These lenders are familiar with the Express program’s documentation and credit criteria, which means fewer delays and clearer communication.

The only caveat? Express loans are capped at $500,000.

Preferred lenders with in-house approval

Lenders in the SBA’s Preferred Lender Program (PLP) can make final credit decisions without sending the loan package to the SBA for approval. That alone can shave weeks off the timeline. Many of the top SBA lenders, including Live Oak Bank, Huntington, and Newtek, are PLP-approved, which helps explain their faster funding speeds.

PLP lenders have dedicated SBA teams and the authority to move without waiting on government sign-off. These banks take anywhere from 30-45 days to make a credit approval.

4. Best for 504 loans and real estate purchases

If your goal is to purchase real estate, buy heavy equipment, or finance major fixed assets, SBA 504 loans are likely your best bet.

The 504 program has a unique structure (bank + CDC partnership), and not every lender participates. Here’s a list of banks that do:

Banks with 504 expertise

SBA 504 loans are used to finance commercial real estate, heavy equipment, and long-term fixed assets. The structure is split three ways:

- 50% from a bank

- 40% from a Certified Development Company (CDC)

- 10% from the borrower.

The key to speed and good terms lies in picking a bank that regularly handles the 504 portion. They’ll know how to work with CDCs and structure the deal properly.

Here are some of the top banks with strong 504 lending programs:

| Banks (50% first mortgage lender) | Known for |

|---|---|

| Wells Fargo | Has a high-volume 504 lender nationwide |

| Bank of America | Actively participates in 504 for real estate and capital purchases |

| US Bank | Offers 504 loans across most U.S. markets |

| Chase Bank | Commonly funds 504 loans for commercial property |

| Live Oak Bank | Industry-specific 504 lending (e.g., healthcare, veterinary, etc.) |

| Celtic Bank | Fast 504 closings, especially for niche commercial assets |

Specialized 504 lenders (certified development companies)

Certified Development Companies (CDCs) are SBA-approved nonprofits that handle 40% of the 504 loan structure. They partner with banks to fund fixed asset purchases and support local economic growth.

While you don’t directly shop around for CDCs like you would banks, choosing one that’s active in your region and experienced with your type of project can make the process easier and faster.

Here are some of the top CDCs in the U.S. by volume and reputation:

| CDC name | Capital Access Group | Notable activity |

|---|---|---|

| TMC Financing | California, Nevada, Arizona | Approved $640M+ of 504 loans |

| Florida First Capital Finance Corp | Florida | Strong state partnership |

| Florida Business Development Corp | Florida | Longtime 504 lender with a deep lender network |

| Business finance capital | California | Deep ties with West Coast banks |

| Capital Access Group | Northern California | Specializes in small business property ownership projects |

Regional and community banks

Regional and community banks often punch above their weight when it comes to SBA 504 loans. Because the bank holds the senior lien (the safest part of the loan), 504 deals let them fund large commercial projects with relatively low risk. Many smaller banks also offer more personalized support, helping coordinate with CDCs, appraisers, and third-party reviewers.

If you already have a relationship with a local bank, it’s worth asking. They may move faster than national lenders and know how to push local paperwork through.

That said, with a 504, you stand to gain long-term, fixed-rate financing for major assets. Just be ready for a bit of extra paperwork (two loans instead of one) and involve the right partners.

5. Most trusted by entrepreneurs (highly-rated)

When you’re taking on a loan that could last 10 or 25 years, you want a lender you can trust.

So we dive deep, check for real user reviews, and bring you a list of top SBA lenders that the entrepreneurs rave about:

SmartBiz

SmartBiz is well known for its speedy approval process. It’s one of the most trusted SBA loan facilitators, where borrowers can get multiple quotes from different lenders instead of directly borrowing from SmartBiz.

Ratings: 4.6/5

Lendio

Lendio, the loan marketplace, shines in customer trust. Entrepreneurs love Lendio for their concierge-like service, wherein you get a dedicated funding manager to help with the process.

Ratings: 4.7/5

Live Oak Bank

Amongst the top SBA lenders for a reason, Live Oak Bank is known for its streamlined processes, exceptional support, and extensive reach.

Ratings: 4.6/5

Need help connecting with preferred SBA lenders?

How to choose the right SBA lender for your business

There are over 800 lenders participating in the SBA’s Lender Match program nationwide. This includes banks, credit unions, online platforms, and nonprofit lenders.

With so many options, it’s important to narrow down your choice based on your business profile and funding needs. Here’s how:

- Know the purpose: Decide exactly how much funding you need and what it’s for. Your use case, i.e., working capital, equipment, and real estate, will determine whether you need a 7(a), 504, or microloan

- Compare approval rates: Compare different lenders based on their systems, processes, approval rates, and the volume of loans they fund each year

- Check industry specialization: Narrow down your choices to lenders who specialize in or have a strong track record with clients in your industry—they will understand your business needs better than others

- Review loan officer experience: When working with a dedicated loan officer, consider their experience and the types of clients they’ve supported in the past

- Understand the fine print: Make sure you understand terms like lender fees, closing costs, funding timelines, and post-loan reporting requirements so you don’t overcommit in the contract

Though tiring, the effort you put into selecting the right lender can pay off in a smoother application and a more enjoyable borrowing experience.

Struggling to choose an SBA lender for your business?

Get Matched With Trusted SBA Lenders With Our Preferred Lender Network

SBA lender readiness checklist: What they want to see

Before you make a loan application, use this checklist to ensure your package includes everything a lender would need to make a decision.

- Business plan (with financial projections): Use an SBA business plan template to write a business plan that clearly outlines your funding needs, business strategies, experience, and financials.

- Personal and business credit history: If you’re applying for 7(a) loans, make sure that you have a personal FICO credit score of 650 or higher.

- Collateral and equity injection: While the SBA guarantee reduces the collateral requirement, for 7(a) loans above $500,000, a lender usually secures all available collateral, including personal assets if necessary

- Relevant experience and management capability: Demonstrate your experience in running a similar-scale business and introduce the experienced advisors or partners supporting your business

- Documentation and legal items: Have all your paperwork organized, including 3 years of personal & business tax returns and legal documents like business formation papers, leases, franchise agreements (if applicable), licenses & permits

The bottom line

Getting your SBA documents in place is just the first step. What makes the difference is how clearly you present your business, how well you understand your funding needs, and whether you’re matching with the right lender.

A rushed or unclear application will waste months of your time, and you might still not get a penny.

If you want help translating your business into lender-ready terms, Upmetrics has a perfect set of tools and services to support you.

- Use our SBA plan templates and AI-powered editor to build a strong business plan.

- Generate 10-year financial projections with clear visuals using our forecasting tool.

- Choose our SBA Lending Assistance to match with approved lenders

Supercharge your business planning and create a roadmap for your future.