Business Plan Software![]()

Plan, Launch, and Grow your Business

Navigate the roadmap to success with our all-in-one business planning software that combines actionable planning, real-time forecasting, and insightful reporting.

15-Day Money BackGuarantee

15-Day Money BackGuarantee

Why Upmetrics?

Collaborative Planning

Team up for success. Our collaborative features allow you to work together with partners or advisors in real time, ensuring everyone is on the same page.

Data-Driven Insights

Make informed decisions with our comprehensive data analysis tools. Get real-time financial forecasts to ensure your business strategy is backed by solid numbers.

User-Friendly Interface

Navigate the planning process effortlessly. Our platform is designed for easy entry, making the creation of your business plan as straightforward as possible.

Exceptional Support on Demand

Whenever you need assistance, Our support team is ready to help. With direct access to our team any questions or hurdles you encounter are quickly resolved.

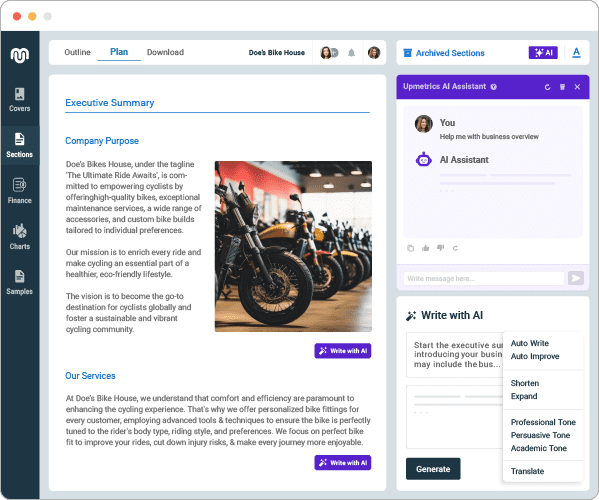

AI-Powered Business Planning

Turn your entrepreneurial ideas into a solid business plan with our AI Business Plan Generator. Our tool ensures that every aspect of your plan is comprehensive, data-driven, and tailored to your unique business needs.

Learn more about AI PlanningNo Writer's Block: AI-Powered Content Generation

Let our AI write compelling business plan sections for you. Simply provide your business details and watch as professional content is generated instantly.

Step-by-Step Guidance to Professional Planning

No business planning experience needed. Our guided process walks you through every section with tips, examples, and industry-specific suggestions.

Collaborate and Share Effortlessly

Invite stakeholders, advisors, and team members to review and contribute to your plan in real-time.

I had a wonderful experience, I was able to cut down the time it takes me to write a business plan by more than half.

More than business plan software

Get started with Upmetrics today and experience the power of AI-driven business planning.

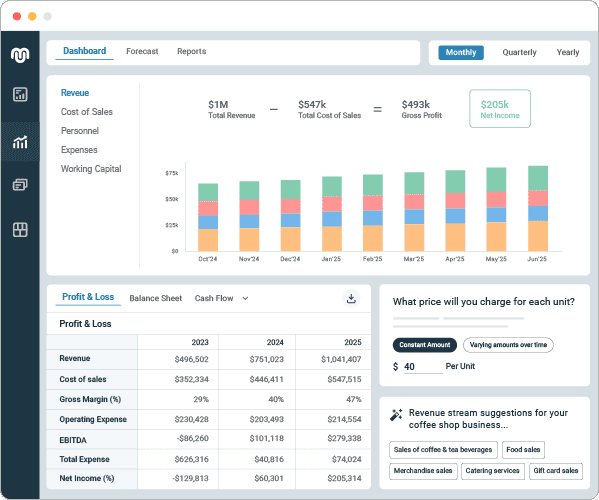

Financial Forecasting & Reporting

Effortlessly create detailed financial projections without the need for complex spreadsheets. Our tool simplifies financial planning, making it accessible and accurate.

Learn more about Financial ForecastingAutomatic Financials

Our automatic financials and AI-powered tools generate projections based on your inputs, saving you hours of manual calculation.

Dashboard and Reporting

Navigate your financial landscape with an intuitive dashboard that presents key metrics, trends, and insights at a glance.

Financial Charts and Graphs

Enhance your business plan with professional charts and graphs that make your financial data compelling and easy to understand.

The seamless integration between business plan and forecasting. When rapidly iterating on a business plan, financial forecasts update automatically.

Empower Your Financial Planning

Build your forecast in minutes, backed by our 15 Day no-questions-asked money-back guarantee.

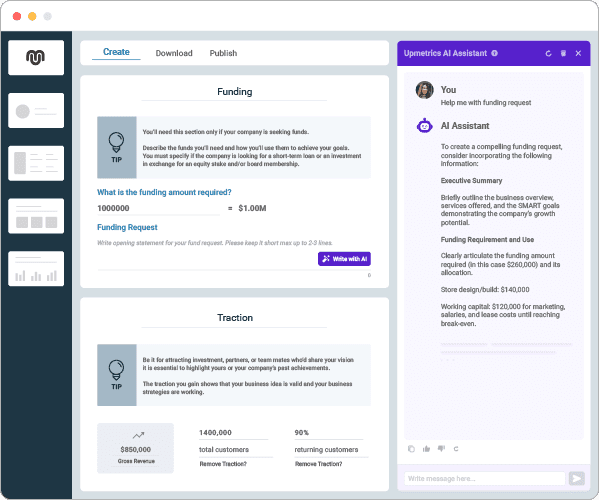

Pitch Deck Builder

Create a standout pitch deck with our AI Pitch Deck Generator. Our tool ensures that your deck is professional, compelling, and investor-ready.

Learn more about Pitch Deck BuilderGenerate Your Deck with AI

Leverage our AI to automatically create pitch deck slides from your business plan data — professional and compelling in minutes.

One-Click Presentation

Ready to present? Deliver your pitch directly from Upmetrics with a clean, distraction-free presentation mode.

Share and Download with Ease

Easily share your pitch deck via link or download as PDF. Perfect for investor meetings, grant applications, and team reviews.

This web-app simplifies the heavy lifting of thinking/planning of writing a business plan. It's easy to use and the AI features are amazing.

Elevate Your Pitch Today

Get started with our AI Pitch Deck Generator and turn your business plan into an investor-ready presentation.

Loved by forward-thinking entrepreneurs and business owners

Check out what our customers have to say about their experience with Upmetrics.

“I had a wonderful experience, I was able to cut down the time it takes me to write a business plan because the layout was already done and the AI feature was also really helpful.”

Athena R.

Mobile Notary and Paralegal Services

“Having complete control over our business plan has been instrumental in being able to raise funds from investors. Upmetrics is an invaluable product that keeps getting better.”

Jason Lorje

Founder & CEO at Agmondo

“Hands down, the best business planning software I have ever used. It is extremely easy to use, it's intuitive, incorporates AI, guides you through it step by step and it's extremely easy for others to collaborate.”

Cindy Kennedy

CEO at Metabolic Terrain Omics

“Drafting impactful and clear business plans is not easy. Navigating complex spreadsheets, creating financial projections, and generating and publishing financial reports take up a lot of a founder's time.”

Deepak Dhanak

Founder at DocuX

“people are impressed! You made my dreams come true on paper fast! AI help and in response were amazing. It's awesome.”

Darin Leonardson

President and CEO, Transformed Culinary Solutions

“I loved the financial modeling capabilities of Upmetrics as they are exceptional and easy to use & understand. It simplifies the often complex process of creating financial projections and forecasts.”

Vaibhav Kamble

Founder at CloudOptime

“I had a wonderful experience, I was able to cut down the time it takes me to write a business plan because the layout was already done and the AI feature was also really helpful.”

Athena R.

Mobile Notary and Paralegal Services

“Having complete control over our business plan has been instrumental in being able to raise funds from investors. Upmetrics is an invaluable product that keeps getting better.”

Jason Lorje

Founder & CEO at Agmondo

“Hands down, the best business planning software I have ever used. It is extremely easy to use, it's intuitive, incorporates AI, guides you through it step by step and it's extremely easy for others to collaborate.”

Cindy Kennedy

CEO at Metabolic Terrain Omics

“Drafting impactful and clear business plans is not easy. Navigating complex spreadsheets, creating financial projections, and generating and publishing financial reports take up a lot of a founder's time.”

Deepak Dhanak

Founder at DocuX

“people are impressed! You made my dreams come true on paper fast! AI help and in response were amazing. It's awesome.”

Darin Leonardson

President and CEO, Transformed Culinary Solutions

“I loved the financial modeling capabilities of Upmetrics as they are exceptional and easy to use & understand. It simplifies the often complex process of creating financial projections and forecasts.”

Vaibhav Kamble

Founder at CloudOptime

Every Feature You Need To Convert A Great Business Idea Into A Reality

Collaborative Workspaces

Team up in real-time with partners and advisors. Share your plan, get feedback, and iterate together in one unified workspace.

Interactive Financial Dashboards

Visualize your financial health with interactive dashboards. Track revenue, expenses, cash flow, and key metrics at a glance.

Customizable Templates

Choose from a range of customizable templates that suit your industry and business model, making plan creation faster and easier.

Business Model Templates

Select from templates like BMC, Lean Canvas, and SWOT analysis to structure your business model and validate your strategy.

Stunning Cover Pages

Create an impactful first impression with a selection of professionally designed cover pages for your business plan.

World Class Support

Experience dedicated assistance with our world-class support team, available to guide you through every step of your planning journey.

Upmetrics helps the world’s most innovative business owners plan better, daily

More than 110K entrepreneurs have used Upmetrics from securing funding to launching their ventures, read compelling case studies.

“The Upmetrics was crucial in building my fashion brand. Their business planning tools streamlined our planning process, We have prepared a business plan that becomes a roadmap for starting and launching our business.”

Business Owner at sarahdonofrio.com

Upmetrics Makes Business Planning Easy For

Our solutions work perfectly for any business planning use case & almost any team size

Secure Funding, Loans & Grants

Craft plans that attract and secure financial backing.

Starting & Launching a Business

Navigate from startup ideas to successful operations.

Validate Your Business Idea

Evaluate and refine your business ideas effectively.

E2 Visa Business Plan

Create a business plan to support your E2 - Visa.

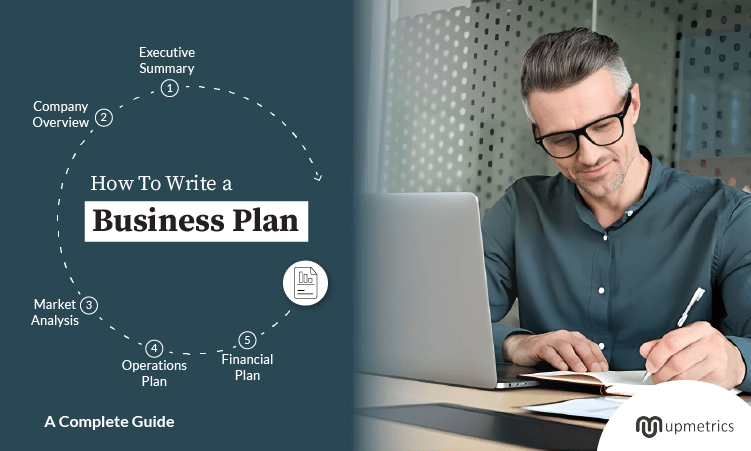

Give A Head Start To Your Business With 400+ Business Plan Templates

We have created a library of sample business plans to help you get started with your writing.

Featured In

Master Business Planning With These Resources

Advice, tools and tips curated by experts to help entrepreneurs plan & grow their businesses.

Write your business plans 2x faster with Upmetrics

- No risk

- Cancel at any time

- 15 Day money back guarantee