Buying a franchise is exciting until you see the total investment cost. $300,000. $500,000. Sometimes more.

And if you’ve never owned a business before, that number can feel out of reach.

So you start researching financing and immediately hit a wall: government acronyms, lender requirements, eligibility checklists. An hour later, you’re no closer to an answer.

Sounds overwhelming?

Let me save you the hours of research. In this guide, I’ll walk you through SBA loan types, eligibility requirements, and the application process so you know exactly how to move forward.

Can you get an SBA loan for a franchise?

Yes, absolutely. You can get an SBA loan to purchase or expand a franchise. In fact, SBA loans are one of the most common ways people finance a franchise purchase in the US.

About 20% of all SBA loans go to franchise businesses each year. That includes first-time buyers, career-changers, and people with no prior business ownership.

The reason SBA loans work so well for franchises comes down to how it works:

The SBA doesn’t actually lend you the money. Banks and credit unions do. The SBA guarantees 75-85% of your loan, which lowers the lender’s risk and gets you better rates and longer repayment terms than a conventional business loan.

The key condition is that your franchise brand must be listed in the SBA Franchise Directory. If it’s on that list, you’re eligible to apply for SBA financing. If it’s not, your franchisor needs to get the brand approved before applying.

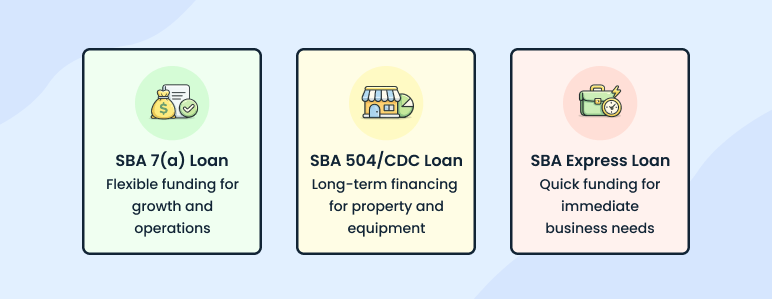

Types of SBA loans for franchises: 7(a) vs. 504 vs. Express

Most first-time franchise buyers walk into a lender conversation knowing they want an “SBA loan” without realizing there are three completely different programs. Each one is built for a different purpose.

Picking the wrong one can limit what you can spend the money on or slow your timeline by months.

SBA 7(a) loan

This is the most common SBA loan for franchise purchases, and the one most lenders will recommend first. You can borrow up to $5,000,000, with repayment terms that vary by use:

- 7 years for working capital

- 10 years for equipment

- Up to 25 years for real estate

The 7(a) loan covers almost everything a franchise opening requires: the franchise fee, buildout costs, equipment, initial inventory, and working capital. That flexibility is why it’s the default choice for most buyers.

Rates are variable, tied to the prime rate plus a lender spread. As of 2026, most borrowers see effective rates between 10.5% and 13.5%, depending on loan size and term.

Can you use an SBA loan to pay franchise fees?

This is one of the most common questions I hear, and the answer is: it depends on the lender.

Most lenders require franchise fees to be paid before SBA financing closes. However, in some cases, an SBA 7(a) loan can include franchise fees as part of the total acquisition cost.

The safest approach is to ask your lender directly during the pre-qualification conversation. Don’t assume it’s covered, and don’t assume it isn’t.

SBA 504/CDC loan

The 504 loan is built specifically for major fixed assets: commercial real estate and heavy equipment. If you’re buying the building your franchise will operate in, or investing in expensive machinery, this is worth a serious look.

The structure is a three-way split:

- 40% comes from a Certified Development Company (CDC)

- 50% from your bank

- 10% from you as the borrower

The fixed rate is one of its biggest advantages, especially in a variable-rate environment.

But there’s a limitation. You cannot use 504 funds for working capital or franchise fees. You’ll also need to create or retain at least one job for every $75,000 borrowed. The threshold is $120,000 for small manufacturers.

SBA express loan

If speed matters and your total investment is under $500,000, the Express loan is worth considering. It funds in 30-45 days versus the 60-90 days you’ll wait on a standard 7(a), and the paperwork requirements are lighter.

The tradeoff is a lower cap and slightly higher rates. Because the SBA only guarantees 50% of Express loans compared to 75-85% for a standard 7(a). That lower guarantee means more risk for the lender, which gets priced into your rate.

I’d recommend this for working capital needs, smaller franchise brands, or situations where closing quickly is critical.

Here’s a side-by-side comparison of SBA franchise loan types:

| Category | SBA 7(a) | SBA 504/CDC | SBA Express |

| Max amount | $5,000,000 | $5,500,000 | $500,000 |

| Terms | 7-25 yrs | 10-25 yrs | Up to 10 yrs |

| Rate type | Variable | Fixed | Variable |

| Best for | Most franchise purchases | Real estate, heavy equipment | Smaller investments, working capital |

| Speed | 60-90 days | 60-90 days | 30-45 days |

| Down payment | 10-20% | 10% | 10% |

The SBA franchise directory: how to check if your franchise qualifies?

As of August 1, 2025, your franchise brand must be listed in the SBA franchise directory to qualify for any SBA-backed loan.

So, check this directory before you apply. It takes two minutes and tells you everything about your eligibility upfront. Here’s exactly how to check:

- Go to the SBA Franchise Directory

- Search your franchise brand by name

- If it appears that your brand is pre-approved, and you’re eligible to apply

- If it doesn’t appear, see the next step below

The directory exists because the SBA requires every franchise brand to be reviewed and approved before a loan can be issued against it.

It’s updated every two weeks, so it reflects the current approval status of thousands of franchise brands across the US.

What if your franchise isn’t listed?

If your brand isn’t in the directory, your franchisor needs to submit two documents to the SBA for review:

- Franchise Disclosure Document (FDD)

- Signed franchise agreement

Both go directly to [email protected]. Once submitted, the review can take anywhere from a few weeks to several months.

The SBA’s main concern during that review is control. If the franchise agreement gives the franchisor excessive control over how you run the business, the SBA may reject the listing.

The agreement needs to reflect genuine business ownership, not something closer to an employment arrangement.

SBA franchise loan requirements: what you need to qualify?

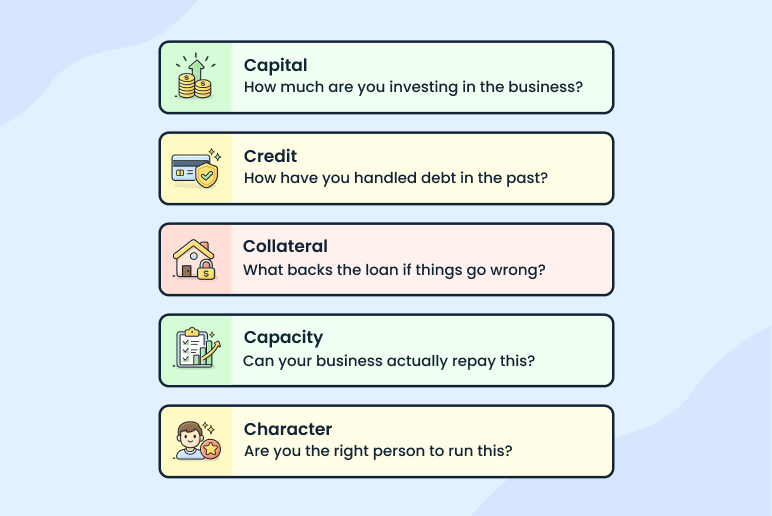

Lenders don’t approve SBA franchise loans based on gut feeling. They run your application through five factors. In the industry, these are called the 5 C’s.

Think of them as the five questions every lender is trying to answer about you.

Capital

This is your down payment, and the amount depends on what you’re buying. For an existing franchise with proven revenue, lenders typically ask for 10-20% of the total investment.

For a brand new location with no operating history, expect 20-30%. The more you put into the business, the more confident a lender feels.

Credit

Most SBA lenders want a personal credit score of 680 or above. Some will work with 650+ if other parts of your application are strong.

Lenders pull both your personal credit and your SBSS (Small Business Scoring Service) score. This combines personal and business credit into one number. A lower score doesn’t automatically disqualify you, but it puts more pressure on everything else.

If your score isn’t where you want it, check out this guide on getting an SBA loan with bad credit before you apply.

Collateral

SBA loans are more flexible on collateral than conventional bank loans. For loans under $25,000, collateral isn’t always required. Between $25,000 and $350,000, lenders follow their own collateral policies, so requirements vary.

For loans above $350,000, lenders look at both business assets like equipment and fixtures, and personal assets. Don’t let this factor alone stop you from applying.

Capacity

This is about your ability to repay the loan. Can your business generate enough revenue to repay the loan?

Lenders typically look for a Debt Service Coverage Ratio (DSCR) of at least 1.25, meaning your business needs to generate $1.25 for every $1.00 of debt payment.

To demonstrate this, you’ll need 24-month cash flow projections, a complete business plan, and any existing personal income you have coming in. This is where a well-built business plan makes a real difference.

Character

This covers your personal background, work experience, and a basic criminal history check. Having prior experience in the industry you’re franchising into genuinely helps your case.

Most lenders prefer two or more years of relevant experience. And yes, completing the franchisor’s official training program counts. It shows the lender you’ve invested time in understanding the business before asking for money.

How much down payment do you need for an SBA franchise loan?

For most people researching franchise financing, this is the question that matters most. The down payment is usually the number that determines whether you’re ready to apply now or need more time to save.

The general range is 10% to 30% of your total investment. But that range looks very different depending on what you’re buying.

When you buy an existing franchise unit, you’re buying something with a history. There are already tax returns, sales records, and a customer base in place. A lender can look at those numbers and make a confident decision.

(And that confidence translates into a lower down payment, typically 10-20%.)

Opening a brand new franchise location is a different situation entirely. You’re asking a lender to bet on projections, not performance. That’s a harder ask.

To offset that risk, they require you to put in at least 20-30% of the total project cost from your own funds.

Here’s what it actually means in real dollars:

| Scenario | Total investment | Down payment (%) | Down payment ($) | Loan type |

| Buying an existing franchise with revenue | $250,000 | 10-20% | $25,000-$50,000 | SBA 7(a) |

| Opening a new franchise location | $500,000 | 20-30% | $100,000-$150,000 | SBA 7(a) |

| Smaller franchise, working capital need | $200,000 | 10% | $20,000 | SBA Express |

| Real estate + equipment purchase | $1,000,000 | 10% | $100,000 | SBA 504 |

What is the 20% rule for SBA?

The 20% rule is the SBA’s minimum equity injection requirement for startup businesses. When opening a new franchise location, you must put in at least 20% of the total project cost from your own funds before the loan can close.

The reasoning is simple. The SBA wants to see that you have a real financial commitment to the business, not just borrowed money.

A borrower who has put in 20% of their own cash is far less likely to walk away when things get tough than someone with nothing personally at stake.

For existing franchise locations with documented revenue, this requirement often drops to 10-15% because top SBA lenders are working with real performance data rather than projections alone.

What if you’re short on the down payment?

Two options come up regularly in this situation.

(1) ROBS (Rollover for Business Startups)

It lets you use existing 401(k) retirement savings as your down payment without triggering early withdrawal penalties or adding more debt to your plate. It’s a legitimate strategy.

But it puts your retirement savings at risk if the business struggles. And it requires your business to be structured as a C-corporation. If you’re planning to operate as an LLC or S-corp, ROBS won’t work for your situation.

(2) Home equity line of credit

If you own a home with meaningful equity, some buyers use that to bridge the gap. Again, the risk is real: you’re putting your home on the line for your franchise.

Neither option is right nor wrong. Both deserve a conversation with a financial advisor before you commit.

How to apply for an SBA franchise loan (step by step)?

Now that you have your down payment figured out, the next question is: What does the actual process look like?

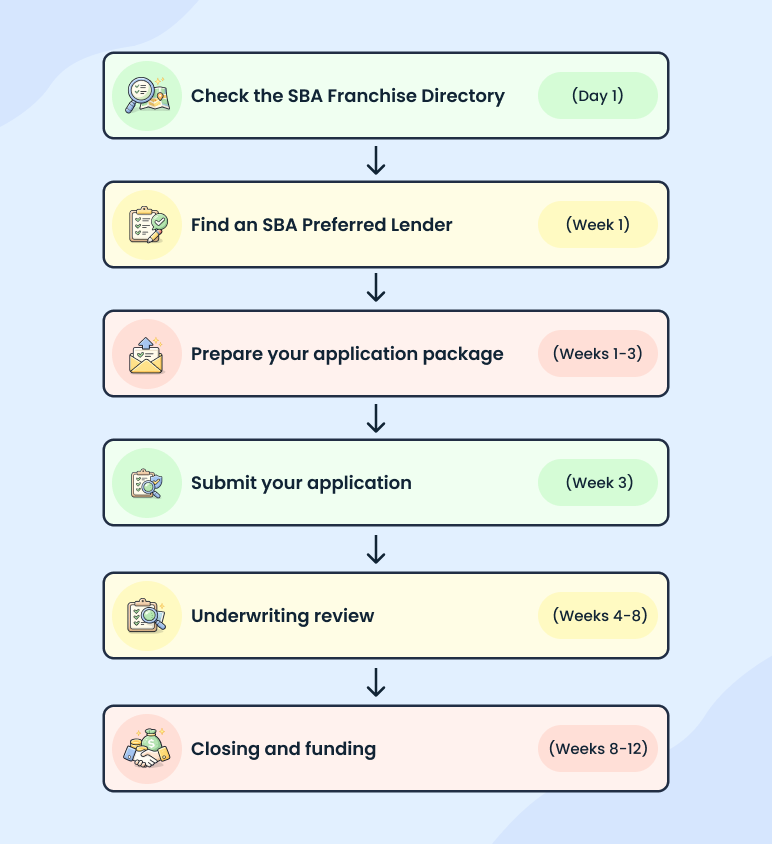

Applying for an SBA franchise loan isn’t complicated, but it does have more steps than a standard bank loan. Here are the six clear steps, from start to funding:

Step 1: Check the SBA franchise directory (Day 1)

First of all, confirm your franchise brand is listed in the SBA Franchise Directory. If it’s there, you’re ready to move.

If it’s not, contact your franchisor immediately and ask them to initiate the approval process. Everything else depends on this step.

Step 2: Find an SBA preferred lender (Week 1)

Not all SBA lenders work the same way. Choose a Preferred Lending Program (PLP) lender. These lenders approve SBA loans entirely in-house, cutting underwriting time from up to 90 days down to roughly 14 days.

Use the SBA Lender Match tool to find PLP lenders near you. Choose your lender before you start preparing paperwork, not after.

Step 3: Prepare your application package (Weeks 1-3)

This is where most of the work happens. You’ll need:

- A complete franchise business plan with 24-month cash flow projections

- Personal and business tax returns from the last 2-3 years

- The Franchise Disclosure Document from your franchisor

- A personal financial statement

- A resume showing relevant work experience

You don’t need an existing business or years of business tax returns to qualify. Lenders focus more on your personal finances, experience, and how strong your plan looks.

A complete package moves through underwriting significantly faster than one with missing documents.

Step 4: Submit your application (Week 3)

Your lender will guide you through the formal submission process. Before you hand anything over, go through your package one more time.

Incomplete applications are one of the most common reasons for delays. And fixing gaps after submission costs you weeks.

Step 5: Underwriting review (Weeks 4-8)

With a PLP lender, underwriting takes roughly 14 days. Non-PLP lenders route your application through the SBA directly, which can take up to 90 days. Choosing a PLP lender has the biggest impact on your overall timeline.

Step 6: Closing and funding (Weeks 8-12)

Once approved, you’ll need to submit the proof of your down payment, signed lease documents, and any remaining paperwork. Funds are released at closing, and you’re ready to move forward.

SBA loans vs. other franchise financing options

SBA loans are the most common starting point for franchise financing. But they’re not the only option. Before you apply, it’s worth knowing and evaluating what else is on the table.

| Option | Rate range | Down payment | Repayment terms | Speed | Best for |

|---|---|---|---|---|---|

| SBA 7(a) | 10.5-13.5% | 10-20% | Up to 25 years | 2-4 months | Most first-time franchise buyers |

| Conventional bank loan | 7-12% | 20-40% | 5-10 years | 30-60 days | Established borrowers with strong credit |

| 401(k)/ROBS | No interest | Varies | No repayment | 3-4 weeks | Buyers with significant retirement savings |

| Franchisor financing | Varies | Varies | Varies | Fast | Brands with in-house financing programs |

| Equipment financing | 8-20% | 0-20% | 2-7 years | 2-4 weeks | Equipment-heavy franchise models |

SBA 7(a) gives you the lowest down payment requirement and longest repayment terms available to first-time buyers. The tradeoff is time. The process takes 2-4 months, and the paperwork is more involved than any other option.

Conventional bank loans are faster and sometimes cheaper in terms of interest rate. But they require 20-40% down and stricter credit qualifications. Without the SBA guarantee, banks carry more risk and set the bar higher to compensate.

ROBS is a genuinely useful option if you have a healthy 401(k). You use your own retirement savings, pay no interest, and take on no additional debt. The risk is: if the business doesn’t work out, that’s your retirement on the line.

Franchisor financing exists for certain brands and is worth asking about directly. Terms vary widely and aren’t always competitive. But some programs are genuinely useful for covering specific gaps like the initial franchise fee.

For most first-time buyers, the SBA 7(a) remains the strongest option. Lower barrier to entry, longer repayment terms, and a process that’s well-established and predictable.

2026 SBA policy changes that affect franchise financing

If you’ve been researching SBA franchise loans using articles from 2023 or 2024, a lot of what you read no longer applies. The SBA made significant policy changes in 2025-2026 that directly affect how franchise loans are processed.

Effective June 1, 2025, the SBA implemented SOP 50 10 8, a major overhaul that replaced the flexible “do what you do” lending approach with stricter, consistent standards.

If you’re applying this year, here’s what changed and what it means for you as a franchise buyer:

- The SBA Franchise Directory is mandatory again. Your brand must be listed before any lender can process your loan. It was eliminated in 2023, but a $397 million deficit in the 7(a) program brought it back.

- Any franchise brand without the new franchisor certification will be removed from the directory by June 30, 2026. If your brand gets removed, you lose SBA loan eligibility entirely. Check the status early.

- The small loan threshold dropped from $500,000 to $350,000. If your total investment is above $350K, expect stricter documentation requirements and a longer review timeline.

- The minimum SBSS score for small 7(a) loans increased from 155 to 165. The SBSS combines your personal and business credit into one score. If you were borderline under the old threshold, check your score first.

- A 10% equity injection is now required for all startup loans and ownership transfers. You need to bring real cash to the table. Seller notes only count if they’re on full standby for the entire loan term with zero payments.

In addition, if you’re buying an existing franchise and the seller retains any equity, even 1%, they must personally guarantee your loan for two years. This changes how most acquisition deals get structured.

With these stricter requirements, a well-prepared application is more important than ever.

Build a strong franchise business plan and get approved

Getting your SBA loan approved comes down to one thing: Convincing the lender you can repay the money. Your franchise business plan is what does that job.

A weak plan is one of the most common reasons SBA applications get denied or delayed. It doesn’t give lenders enough confidence in your ability. But a strong plan gives a lender everything they need to make a confident decision.

Here’s what lenders specifically want to see:

- Compelling executive summary

- Territory market analysis

- 24 months of monthly cash flow projections

- A pro-forma balance sheet

- Your management team & background

Most first-time buyers underestimate how long this takes to put together properly. Researching your territory using FDD data, building projections around the franchise model, and structuring the narrative, it adds up quickly.

And if you’re juggling a job or a family on top of it, a blank document can sit untouched for weeks.

If building all of this from scratch sounds like a lot, the Upmetrics franchise business plan template makes a real difference. It gives you a ready-made structure and creates your projections automatically as you fill in your numbers.

And if you want to move even faster, the Upmetrics AI plan generator can get you to a lender-ready draft in a fraction of the time.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.