I remember sitting in my home office at midnight, staring at a spreadsheet that showed three months of steady growth. The business looked fine on screen. My personal bank account was nearly empty, throwing low-balance alerts I’d stopped reading.

My co-founder asked me that week: “So when do we actually start paying ourselves?” I had no answer. I just assumed the right moment would announce itself somehow.

Most founders get stuck exactly here, fed on vague advice like “pay yourself when you can afford it.” That’s useless. It doesn’t tell you what “afford” looks like when your revenue fluctuates month to month, and your expenses keep shifting.

What I eventually learned is that the timing has nothing to do with hitting a number on your dashboard. It’s about building enough financial clarity to know what your business can actually sustain and planning for your salary before you feel ready to take it. That’s the framework I’m sharing here.

Fact: Your salary is a business expense (not a reward)

There’s a certain kind of founder story that gets a lot of LinkedIn applause: “I didn’t pay myself for two years.” It sounds like discipline and commitment. Most of the time, it’s just bad financial planning wearing a noble costume.

Here’s what that story leaves out: the two years of Sunday anxiety. The moment you start resenting your own business because it takes everything and gives you nothing back. The way you start making desperate decisions, chasing bad clients, and avoiding necessary expenses because you’re financially underwater and emotionally exhausted.

That’s not sacrifice. That’s burnout.

I’ve seen founders hit month eighteen of zero salary and start quietly hoping the business fails so they can just stop. Not because the business was bad. Because they never built themselves into the equation, and eventually the math caught up with them personally.

Peter Thiel once argued that a low CEO salary signals mission-driven leadership. That’s a reasonable take for a VC-backed founder with personal savings and investor support. It has almost nothing to do with a bootstrapped small business owner trying to keep the lights on at home while building something real.

The data reflects this honestly. According to Pilot’s 2025 founder compensation report, average founder salaries dropped 43% in a single year, and roughly 60% of founders earn under $100K annually. A lot of that isn’t a noble sacrifice; it’s the founders who simply never built their own salary into the plan.

Your salary isn’t a reward you unlock after hitting a milestone. It’s a business expense, the same as rent, payroll, or software. If it’s not in your financial plan, you’re not modeling a real business; you’re modeling a version of it where you work for free indefinitely.

The question was never if you should pay yourself. It’s always been when and how much.

When to pay yourself from your business

Most founders ask, “When can I pay myself?” and expect a revenue number as the answer. There isn’t one. The answer is a set of conditions, and when all five are true at the same time, you’re ready.

Here’s what I look for.

Positive cash flow for 2 to 3 consecutive months

One profitable month doesn’t tell you much. It could be a seasonal spike, a one-time client, or just a good week stretched across four.

Two to three months in a row start showing a pattern. That pattern is what you’re actually planning against, not a single good month that felt like momentum.

Watch for this: if your cash flow is positive but only because you delayed paying a vendor or held off on a necessary expense, that doesn’t count. Clean positive cash flow means all obligations are met and money is still coming in.

Three months of runway left after your salary is added

This is the one most founders skip, and it’s the most important one on this list.

Don’t check your runway and then add your salary. Check your runway with your salary already sitting inside the projection as a line item. Those are two very different numbers.

If adding your salary drops the runway below three months, you’re not ready yet. The business needs that cushion for slow months, unexpected expenses, and the kind of surprises that show up in every business’s second year.

Everyone else is paid (employees, vendors, obligations)

Employees, vendors, contractors, software subscriptions, and tax obligations. All of it settled before you take anything.

This isn’t just an ethical position; it’s a practical one. A vendor who isn’t getting paid will stop delivering. An employee who’s waiting on a paycheck will start looking elsewhere. Those problems cost more to fix than a delayed salary draw.

If you’re in a position where paying yourself means someone else waits, that’s the answer. You’re not ready yet.

You can forecast the next 6 months with confidence

Not perfectly, no forecast ever is. But there’s a real difference between a projection built on actual data and one built on hope.

If your next six months of revenue feel genuinely uncertain, a new market, an untested product, or inconsistent clients that uncertainty is the thing to resolve first. A salary decision made without forward visibility isn’t a plan. It’s a guess with consequences.

The goal isn’t a perfect forecast. It’s enough visibility to know that a modest monthly draw won’t put you underwater by Q3.

You’ve raised funding and have room to grow

If investors are involved, the calculus changes completely. A reasonable founder salary isn’t just acceptable, it’s expected.

A burned-out founder making desperate decisions because they can’t pay their rent is a far bigger risk to your investors than a modest salary on the books. According to Pilot’s 2025 compensation report, the average founder salary sits at $75K annually. That’s not a target; it’s a floor that most funded founders should be working toward.

Taking zero salary when you have funding isn’t a discipline signal. It’s usually a sign that your financial plan isn’t complete enough to model your own compensation yet.

How much should you pay yourself? (Bootstrapped vs. funded)

Most founders I’ve talked to either guess or they Google “average founder salary,” land on a number that sounds reasonable, and go with it. Neither of those is a plan.

The number you pick should come from your business, not from someone else’s benchmark. Here’s how I actually think about it.

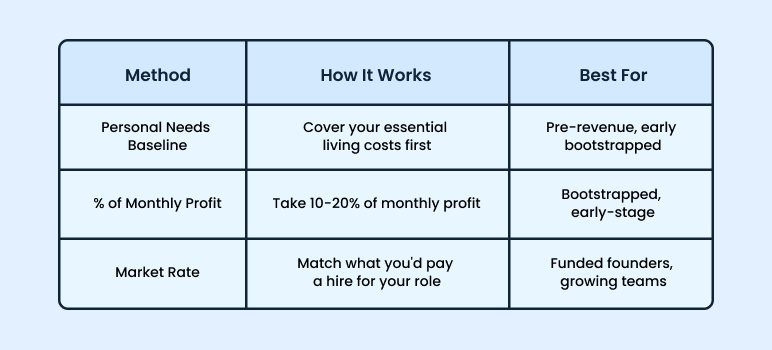

Start with what you need to survive

Before anything else, figure out your personal floor. Rent, food, insurance, basic living expenses. Add it up.

That number matters because paying yourself below it creates a slow financial stress that bleeds into every decision you make about the business. If the business can’t cover your floor yet, that’s not a reason to keep waiting; it’s a target to build toward in your forecast.

Then look at what the business can actually support

Take your monthly profit after covering all operating expenses. In my experience, a reasonable starting draw is 10-20% of monthly profit.

The U.S. Chamber of Commerce describes this as a cash-flow-based approach, where your pay flexes up in good months and pulls back in slow ones, instead of locking in a fixed amount that the business can’t always carry. That math also tells you, honestly, whether you’re ready to start at all.

Finally, sanity-check against your market rate

Ask yourself: if I had to hire someone to do everything I do in this business, what would that cost?

You don’t need to hit that number now. But it tells you what direction you’re heading and gives you something to benchmark against as the business grows.

Your business model shifts this, too. Service businesses usually see revenue earlier, so the cash flow picture becomes clear sooner. Product companies run longer before revenue arrives, which makes it more important to forecast your salary from day one, not add it once things pick up.

Solo operators have a different problem. Without a team salary to benchmark against, the personal floor calculation is your clearest anchor. Start there.

For context, Pilot’s 2025 compensation report puts the average founder salary at $75K annually. That’s not a target; plenty of early-stage founders start well below that. It’s just useful to know where most people land.

What happens if you need to pause your salary?

It happens more than founders admit. You start paying yourself, something shifts in the business, and suddenly that salary line feels like a liability instead of a plan.

That’s not failure. That’s cash flow doing what cash flow does.

The worst thing you can do is quietly stop and pretend it didn’t happen. The second worst is panicking and cutting everything without a plan to restart.

When you need to pause, do three things:

First, document the decision. Write down why you’re pausing, what the current numbers look like, and what needs to change before you restart. This keeps it deliberate rather than reactive.

Second, set a specific resume trigger. Not “when things get better.” Something concrete, like “when monthly revenue stays above $X for two consecutive months.” That number goes into your financial plan.

Third, check your projections. A salary pause is often a signal that your original forecast had gaps. It’s worth revisiting your financial projection mistakes before you model the restart.

The goal is to treat the pause the same way you treated the start as a deliberate financial decision, not an emotional one.

| Pause If… | Resume When… |

| Cash drops below 3 months of runway | Runway is back above 3 months after salary is modeled in |

| Revenue misses forecast for 2+ months | Revenue meets or exceeds forecast for 2-3 consecutive months |

| A large unexpected expense hits | The expense is absorbed, and cash flow stabilizes |

| You’re funding payroll from reserves | All obligations are covered from operating revenue |

If a large purchase is what triggered the pause, planning that purchase differently next time is worth reading about. Here’s how to budget for big buys without hitting your runway.

Salary vs. owner’s draw (alternate option)

Most founders don’t realize there are two completely different ways to pay yourself, and which one you use isn’t a preference; it’s determined by how your business is structured.

Getting this wrong doesn’t just create accounting headaches. It can create a tax problem you don’t see coming until filing season.

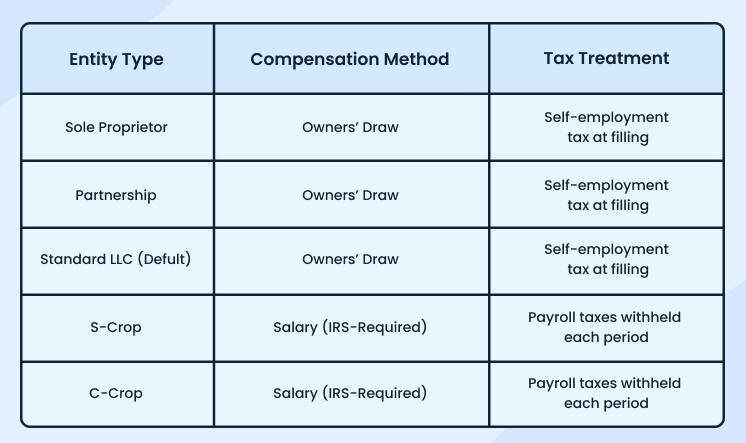

The core difference:

A salary is a fixed, regular payment that runs through payroll. Taxes are withheld upfront: federal income tax, Social Security, and Medicare. It’s predictable, structured, and required for certain business types.

An owner’s draw is a withdrawal from business profits. No payroll taxes withheld upfront, but you’ll pay self-employment taxes when you file. It’s more flexible but also less structured.

Which one applies to you:

If you’re a sole proprietor, a partnership, or a standard LLC, you take an owner’s draw. You’re not considered an employee of your own business, so a traditional salary doesn’t apply.

If you’re an S-Corp or C-Corp, you’re legally an employee of your business. The IRS requires S-Corp owners to pay themselves a “reasonable salary” before taking any distributions, and ignoring this is one of the more common and costly mistakes founders make. The IRS guidance on paying yourself breaks this down clearly by entity type.

The method matters less than understanding which one you’re supposed to be using. If you’re not sure, that’s the first thing to clarify with your accountant before you take anything.

The bottom line

There’s no sign that comes. No month where everything feels stable enough, safe enough, ready enough. Waiting for that moment kept me unpaid longer than it should have, and the business didn’t benefit from it either.

What finally changed things wasn’t a revenue milestone. It was building enough visibility into my finances to make the call with confidence instead of just hoping the timing would sort itself out.

Your salary belongs in your plan from day one. Not as a reward you earn after hitting a milestone, but as a real expense the business needs to carry, the same as rent, payroll, or software. The sooner you treat it that way, the more honest your numbers become.

Start small. Put it on the books. Know which method applies to your structure, know your signals, and review the number every quarter. And stop treating unpaid months as proof of commitment. They’re just months; your plan wasn’t complete enough to account for you.

If you want to see what your business actually looks like with your salary modeled in from the start, Upmetrics’ AI-powered business plan generator can help you build that picture before you commit to a number.

Build the plan. Include your salary. Then follow it.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

How much should I pay myself as a new business owner?

What's the difference between a salary and an owner's draw?

Can I pay myself if my business isn't profitable yet?

What if I started paying myself and now need to stop?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more