Veterans own more than 2.5 million small businesses in the United States and employ nearly 6 million people.

If you’re a veteran planning to start or grow a business, you’ve probably searched for funding options and hit the same wall everyone does: the VA doesn’t offer business loans.

That’s where the SBA comes in. SBA loans for veterans are issued by banks but backed by the government, which makes them easier to qualify for than traditional loans.

Veterans also get real advantages like reduced or waived fees, longer repayment terms, and access to lenders who understand your background.

This guide covers the 5 SBA loan programs available to veterans, the eligibility requirements you need to meet, the step-by-step application process, and the extra resources most veterans don’t know exist.

Why is the SBA loan (and not the VA) the best option for a veteran?

A lot of veterans start by searching for business loans on VA.gov. You won’t find any. The VA handles home loans, disability compensation, and healthcare, but they don’t offer business loans at all. For that, you need the SBA.

And SBA loans are the best option for one simple and practical reason: they make borrowing easier and cheaper.

Private lenders and alternative financing options may charge up to 18% to 24% in interest. While SBA loans are issued by banks, they are backed by the government.

This reduces the lender’s risk, so you get better terms than a typical business loan:

- Lower down payments

- Longer repayment periods (up to 25 years for real estate)

- More flexible credit requirements

Veterans also get extra benefits. Through the Veterans Advantage program, you may pay reduced or zero upfront fees, which can save thousands at closing.

5 Types of SBA loans you can apply for as a veteran

The SBA doesn’t offer just one loan. There are five different programs for veterans, each built for a different stage of business and funding need.

The right one depends on:

- How far along your business is

- How much money you need

- How fast you need it

Here’s a full breakdown of all five programs available to veterans, including the one most guides leave out entirely.

| Loan Type | Max Amount | Interest Rate Range | Best For | Veteran-Specific Benefit |

| SBA 7(a) | $5,000,000 | Prime + 2.75% to 4.75% (variable) | Established businesses needing working capital, equipment, or real estate | 50% reduction on upfront guaranty fee |

| SBA Express | $500,000 | Prime + 4.5% to 6.5% | Businesses needing faster approval and smaller loan amounts | 0% upfront guaranty fee |

| SBA Microloan | $50,000 (avg. ~$13,000) | 6% to 9% | Startups and early-stage businesses with limited credit history | Access to nonprofit intermediaries with veteran-focused programs |

| Community Advantage | $350,000 | Prime + up to 6% | Veterans in underserved or rural communities | Mission-based lenders focused on underserved borrowers |

| Military Reservist Economic Injury Disaster Loan (MREIDL) | $2,000,000 | 4% fixed (8% if credit available elsewhere) | Businesses affected by active-duty call-up of owner or key employee | Designed for reservists and National Guard members |

Which loan should you choose?

For real estate or large working capital: The SBA 7(a) works best if your credit score is above 680. It goes up to $5 million and gives you up to 25 years to pay it back if you’re buying property.

For speed: SBA Express gets you an answer in 36 hours and funding in about 20 days. It caps at $500,000, and the rates are a bit higher, but you don’t pay any upfront fees as a veteran.

For new businesses: Microloans and Community Advantage loans are easier to get if your credit is around 620 to 680. You can’t borrow as much, but they work with nonprofit lenders who get veteran-owned businesses.

For reservists and Guard members: MREIDL is built for you if an active-duty call-up hurts your business. You can get up to $2 million at a fixed 4% rate.

Bigger loans take longer and need better credit. Smaller loans move faster but don’t go as high. Express loans fund in three weeks, but regular 7(a) loans take two to three months and usually have lower rates.

Most lenders want your credit score above 620. Don’t just pick the biggest loan amount. Pick the one that fits where your business is right now.

Veterans advantage program: Fee waivers and discounts

Beyond the loan programs themselves, veterans get a clear cost advantage through the SBA’s Veterans Advantage program. This benefit reduces or eliminates the upfront guaranty fee, one of the highest additional costs of an SBA loan.

In addition, the Veterans Advantage program can save veterans thousands in upfront fees. The table below shows the exact breakdown:

| Category | SBA Express Loan | SBA 7(a) Loan (General) | Example: $350,000 SBA 7(a) |

| Standard Borrower Fee | 2% – 3.5% | 2% – 3.5% | $7,875 |

| Veteran Benefit | 100% fee waived | 50% reduction | 50% reduction |

| Fee Paid by Veteran | 0% | 1% – 1.75% | $3,938 |

| Savings | Full fee saved | 50% savings | $3,937 |

To qualify, your business must be at least 51% owned by an eligible individual:

- Veterans

- Service-disabled veterans

- Active-duty members in transition programs

- National Guard or Reserve members

- Spouses and widowed spouses of service members

The best part is that this benefit is automatic. There’s no separate application. As long as your lender knows your eligibility, the reduced fee is applied during the loan process.

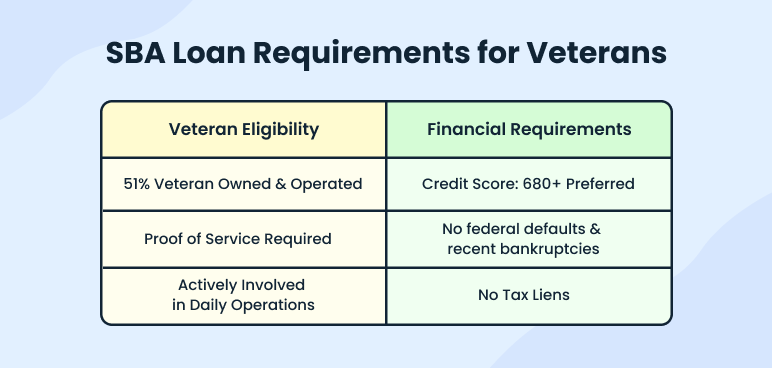

Do you qualify? SBA loan requirements for veterans

Eligibility for an SBA veteran loan isn’t complicated, but it is specific. The requirements fall into two buckets: proving your veteran status and proving your business can handle the debt.

I’ve seen applications stall because someone had the financials in order but was missing a single document on the veteran side — usually a DD214 or proof of service-disabled status. Getting both right before you apply saves weeks.

Business ownership requirement

Your business must be at least 51% owned and controlled by an eligible veteran. Ownership on paper isn’t enough. You need to be actively involved in managing the business day to day.

If you’re a silent majority owner with someone else running operations, that raises questions during underwriting. Lenders want to see that the veteran is making decisions and driving the business.

Financial requirements

Lenders evaluate your credit, your cash flow, and your ability to repay. For most SBA 7(a) loans, lenders look for a credit score of at least 680, though some will work with scores as low as 620 depending on the strength of the rest of your application. If your credit score is a concern, it’s worth reading up on how to approach an SBA loan with bad credit before you apply.

Beyond credit, lenders want to see a clean federal record:

- No existing federal debt in default

- No recent bankruptcies without clear resolution

- No active tax liens

These aren’t negotiable. Full SBA loan requirements provide a detailed view of the complete financial picture if you want to go deeper.

What documents do you need?

| Veteran Documents | Business Documents | Financial Documents |

| DD Form 214 (Certificate of Release or Discharge from Active Duty) | Business license and registration | Personal tax returns (2–3 years) |

| VA disability rating letter (if service-disabled) | Articles of incorporation or LLC operating agreement | Personal financial statement |

| Proof of Reservist or National Guard status (if applicable) | Business tax returns (2–3 years for established businesses) | Business bank statements (3–6 months) |

| — | — | Profit and loss statement, cash flow, and balance sheet |

Missing even one of these can delay your application by weeks. Get everything together before you reach out to lenders.

Let AI draft your SBA business plan in minutes

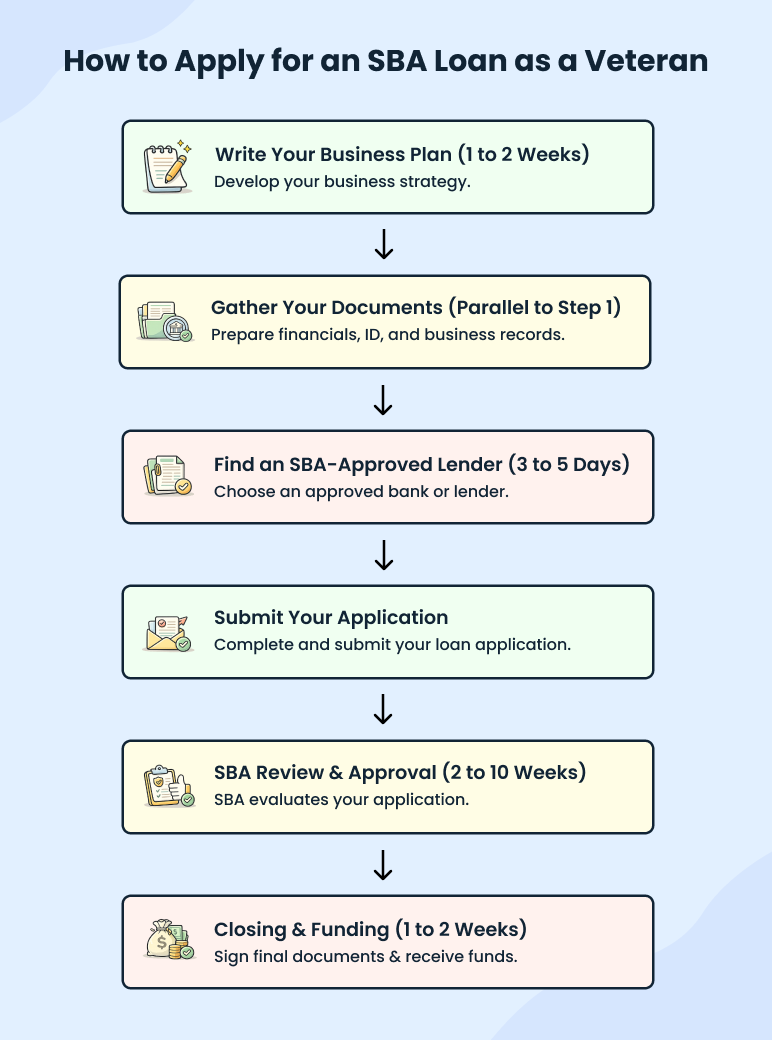

How to apply for an SBA loan as a veteran

We already know the SBA loan process is long and sometimes complex. A standard 7(a) loan takes 30 to 90 days from application to funding. SBA Express moves quicker, with a 36-hour SBA response and funding in roughly 20 days. How prepared you are going in determines where you land in that range.

Step 1: Write your business plan (1 to 2 weeks)

Lenders need an executive summary, market analysis, and 12 months of projections in your SBA business plan.

Step 2: Gather your documents (parallel to Step 1)

DD214, tax returns, bank statements, personal financial details, and any licenses.

Step 3: Find an SBA-approved lender (3 to 5 days)

Use SBA Lender Match and reach out to 2–3 lenders.

Step 4: Submit your application

Your lender puts together Form 1919, your business plan, financials, and paperwork.

Step 5: SBA review and approval (2 to 10 weeks)

Stay responsive if they ask for more details.

Step 6: Closing and funding (1 to 2 weeks)

Sign documents and receive funds within 5–10 days.

What extra benefits do disabled veterans get (loan options)

The SBA loan programs for veterans discussed above apply to all military forces, but if you have a service-connected disability, you get additional advantages that go beyond standard SBA benefits.

The biggest advantage is certification. By registering as a Service-Disabled Veteran-Owned Small Business (SDVOSB) through the SBA’s VetCert program, you become eligible for federal contracting opportunities.

The government has a goal to award at least 3% of all federal contract dollars to SDVOSBs, which creates a steady pipeline of revenue opportunities alongside your loan funding.

Registration takes place at veterans.certify.sba.gov (VetCert). You’ll need:

- DD-214

- VA disability determination letter

- Proof of business ownership

For loans, disabled veterans get the same deal as other veterans — no upfront fees on Express loans, half off on 7(a) loans. Your disability rating doesn’t change the loan terms or make approval easier, but SDVOSB certification helps. Lenders see it as proof that you can land government contracts.

You also get training through programs like the Service-Disabled Veteran Entrepreneurship Training Program (SDVETP) and VBOCs. They help you build a real business, not just get a loan.

Your disability rating does not directly change loan approval criteria, but it strengthens your eligibility for certifications, contracts, and support programs that can improve your overall business stability.

SBA resources and training programs for veteran entrepreneurs

Getting a loan is step one. Building a business that pays it back is harder. The SBA runs free training programs for veterans. Most don’t know they’re out there. Here’s what you can use:

- Boots to Business: For active-duty members getting out. Covers business basics, planning, and funding.

- Boots to Business Reboot: Same thing as B2B, but for veterans who already got out, no matter when you served.

- V-WISE: For women veterans. Training and mentorship to start and grow businesses.

- Veterans Business Outreach Centers (VBOCs): Free help with business plans, operations, and funding questions. They’re all over the country.

- SCORE: Pairs you with people who ran businesses before. Real advice from people who did it. Free.

- Small Business Development Centers (SBDCs): Local advisors who help with planning and running your business. Also free.

Find the nearest VBOC or SBDC at sba.gov/local-assistance. For SCORE mentors, go to score.org/veterans.

How a strong business plan helps you get approved for an SBA loan

Whether you’re pursuing an SBA loan, a grant, or another funding path, one thing doesn’t change. You need a solid, clearly written business plan. SBA lenders expect it, and the quality of that document often determines whether your application moves forward at all.

Lenders aren’t just looking at your idea. They want to see you understand your business. Your executive summary should explain what you do and how you make money. Your market analysis needs to show demand and prove you know your competitors.

The financials are where most applications either hold up or fall apart. Lenders want cash flow projections, a profit and loss statement, and a balance sheet that prove you can pay the loan back.

A lot of applications get rejected not because the business concept is bad, but because the plan is vague or the numbers don’t add up. Lenders are looking for realistic projections, a clear strategy, and evidence that the people running the business can actually pull it off.

Tools like Upmetrics can help organize a plan using SBA-ready templates with built-in financial forecasting, which cuts down on guesswork and presents the business in a format lenders are already familiar with.

Conclusion

The SBA has built a genuinely strong set of programs for veterans: reduced fees, favorable loan terms, free counseling, and training resources that most borrowers don’t have access to. Whether you’re launching a new business or growing an existing one, these advantages are real and worth the effort it takes to access them.

The application process requires preparation, but nothing here is beyond your reach. Start by understanding your SBA loan requirements and revisit what an SBA loan actually involves if you need a refresher.

When you’re ready to build the business plan your lender will require, Upmetrics has SBA-ready templates and financial forecasting tools to help you put together a plan worth approving.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.