Writing a business plan sounds intimidating for about a dozen reasons, but I only want to pick one of them today, which is getting the whole thing down on paper in the right order.

Most founders already have the idea in their head, clear as day. The problem is that the idea (the offer, the market, the numbers, the team, the operations, the funding ask) arrives all at once.

Without structure, it turns into a long note, which is not what anyone would want. That’s the gap a business plan outline fills. It gives the whole plan a backbone before you start adding details. Even the parts you’re unsure about become easier to see. That’s how important it is.

So that’s the plan here. I’ll walk you through the outline I’d actually use, section by section, and help you choose the right format before you draft.

What is a business plan outline?

A business plan outline, sometimes just called a business outline, is a section-by-section structure that shows what your plan should include before you start writing it.

It tells you where each part goes, from the executive summary through the financial plan and any funding details. It doesn’t write the plan for you. It just gives everything a clear order, so you’re not figuring out structure and content at the same time.

One thing worth clearing up: “outline,” “template,” and “sample” aren’t the same.

- A business plan outline shows you the sections and what each should cover.

- A business plan template gives you a fill-in document to write in.

- A sample business plan shows you what a finished plan looks like.

So before we build one, here’s why it’s worth your time.

Why use a business plan outline?

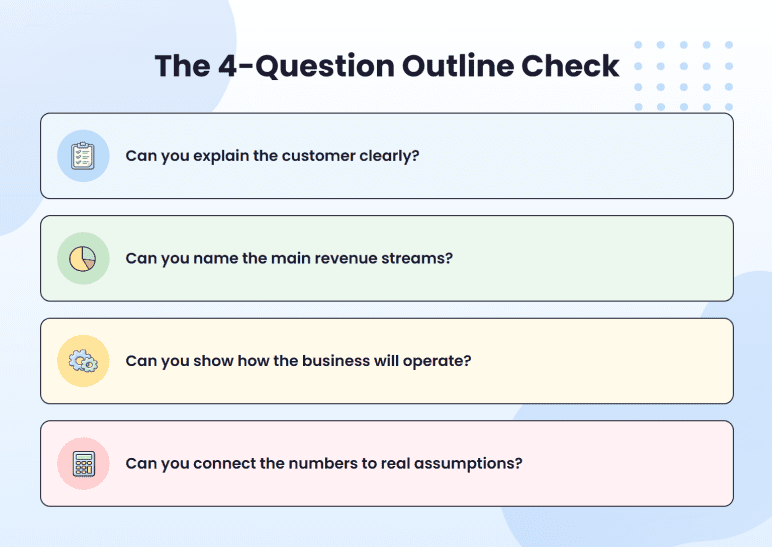

A business plan outline is useful because it helps you catch weak spots before they become full paragraphs.

That matters more than it sounds. If your target market is vague, your whole market analysis comes out vague. If your pricing has no logic behind it, your financial projections read like guesses. Catch that in a one-line outline entry, and you’ve saved yourself rewriting three pages later.

So before you draft, use the outline to pressure-test four things:

There’s a second payoff when someone else has to read the plan. Lenders, investors, and partners all skim in a familiar order; they expect the standard sections to sit exactly where they always sit.

The SBA even lays out that expected section order, so an outline that follows it makes your plan instantly familiar to the people reviewing it. A clean structure is easier to review and a lot harder to misread, which counts for plenty when someone’s deciding whether to back you.

Before you fill in a single section, you need to know how much plan you’re actually building, and that comes down to format.

Which business plan format fits your business?

Before you start writing, ask one question: Who is going to read this?

That answer decides the format. A lender does not need the same plan as a cofounder. An investor does not read it the same way you do. And if you’re still testing the idea, a 25-page plan may be too much too soon.

Here’s the simple way to choose:

| Format | Best for | Length | What it includes | When to use it |

| Traditional business plan | SBA loans, bank funding, investors, and complex businesses | Usually 15-25 pages, depending on complexity | Full outline with company, market, operations, team, financials, funding, and appendix | Use this when someone outside the business will judge the plan |

| Lean business plan | Early-stage founders testing an idea | 1-3 pages | Problem, solution, customer, channels, costs, revenue streams, and key assumptions | Use this when the idea is still changing |

| One-page business plan | Internal planning, cofounder discussions, quick strategy notes | 1 page | A short summary of the business model, goals, market, offer, and numbers | Use this when you need clarity, not a formal document |

This guide focuses on the traditional business plan outline because it’s the safest default when funding or any outside reader is involved. If you need something lighter, the same sections compress into a lean or one-page version, and our breakdown of the types of business plans walks through when each one makes sense.

Once you’ve picked the format, here’s what goes into each section of a traditional business plan.

What sections should you include in a business plan outline?

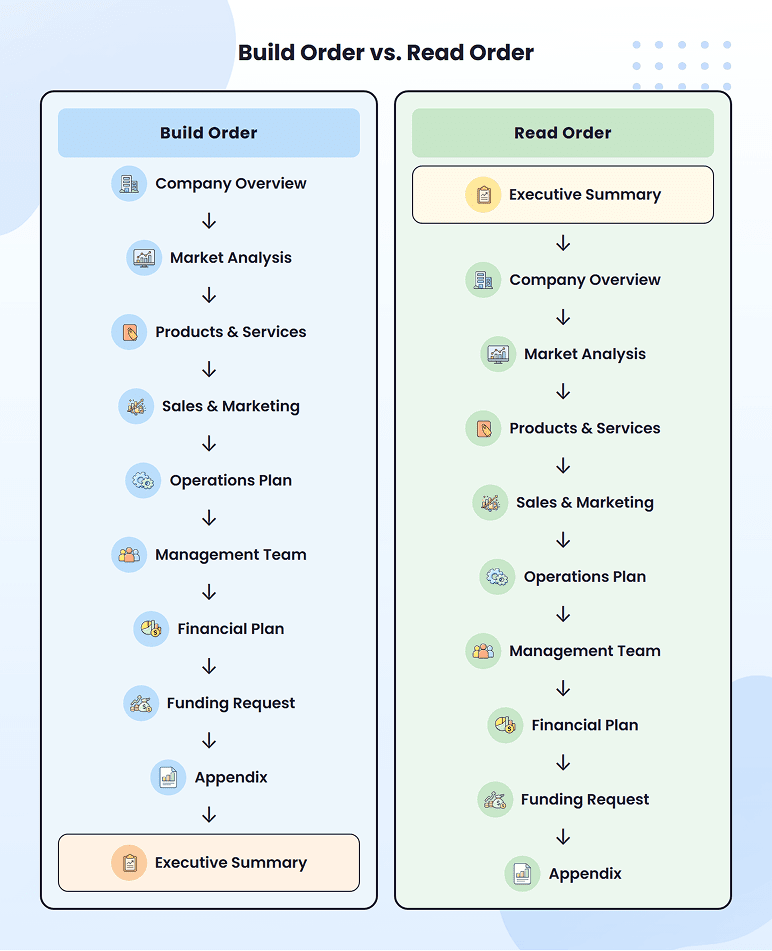

I’ll let you in on a small trick that’s saved me a ton of rework: build the outline in order, but write the executive summary last.

Now let’s go section by section, in the order your reader sees them. (If you want the deeper version of the actual writing process, our complete guide on how to write a business plan walks through it, start to finish.)

We’ll start with the executive summary, the part they read first, even though, as I said, it’s the one you write last.

The funding request is the one section I treat as optional: I include it when I’m raising money and skip it when the plan’s just for a cofounder and me.

With the order sorted, let me show you what I’d put in each section.

1) Executive summary

The executive summary comes first in the finished plan, but as I said, I write it last, once the rest is clear enough to summarize.

Its whole job is to give the short version. If a lender reads only these one or two pages, they should still walk away knowing what the business does, who it serves, how it makes money, why it’ll work, and what you’re asking for.

Here’s what I make sure it covers:

- Business description: what the business does, where it operates, and who it serves.

- Problem and solution: the customer problem and how your product or service solves it.

- Target market: the main customer group and the size or demand behind the opportunity.

- Products or services: the core offer and what makes it different.

- Traction: early proof, like sales, paying customers, signed letters of intent, a waitlist, partnerships, or pilot results.

- Financial snapshot: revenue model, key costs, profit expectations, and basic projections.

- Funding need: how much you need, if any, and how you’ll use it.

Let me make this concrete with an example I’ll carry through the rest of the plan.

Say you’re opening a specialty coffee shop near campus in Eugene, Oregon. Here’s how that executive summary reads:

A campus-adjacent espresso bar solving the “no good coffee on this block” problem, targeting students and nearby office workers, earning through in-store sales and catering, with $120,000 requested for buildout and equipment.

That’s the whole summary. Everything after it is just a detail. You can add a short mission, vision, or values line if it helps explain why the business exists, but keep it to a line. The summary is where you make the reader want to keep going, and if you’d rather not build it from a blank page, Upmetric’s free business plan template gives you the structure to fill in.

2) Company overview

The executive summary gave the short version. This is where you have to lay out the basic facts: what the business is, where it operates, who owns it, how it’s structured, and what stage it’s at. I keep it factual by including:

- Business name and concept: what the business does, in plain language.

- Location: where it operates and why that spot makes sense.

- Legal structure: sole proprietorship, partnership, corporation, or LLC.

- Ownership: who owns the business and who makes the major decisions.

- Business stage: pre-launch, newly opened, growing, or already established.

- Mission or purpose: if you used a mission line in the summary, this is where it gets a full sentence or two.

- Key facts: founding year, employee count, facility size, early revenue, anything that adds context.

For the Eugene coffee shop, this section covers the shop’s name, the campus-adjacent lease, the owner’s background (say, ten years working in specialty coffee), the LLC setup, and why that block, with heavy student and office-worker foot traffic and no quality coffee nearby, supports the concept.

Once you get this right, the reader has the full context they need before the market and financial sections make their case.

3) Market analysis

Market analysis answers whether there is enough demand for this business to make sense.

Some drafts say something like “the coffee industry is growing,” which tells a lender exactly nothing. So I suggest getting specific and local instead. “There are thousands of students within a five-minute walk, and nothing on this block sells quality coffee past mid-afternoon” is something a lender can actually weigh.

A strong market analysis usually covers:

- Industry context: local market size, growth, and the main forces at play, not national fluff.

- Target market: the exact customer groups you’ll serve.

- Customer need: the habit or buying reason that creates demand.

- Market size: the total market, the slice you can realistically reach nearby, and the share you expect to win.

- Entry barriers: rent, permits, staffing, supplier access, customer loyalty, whatever makes the market hard to crack.

For the Eugene shop, the target is students, faculty, and office workers within walking distance. The real work is the competitor scan, and that reads far better as a table than a paragraph:

| Competitor | Type | What they offer | The gap they leave |

| Campus dining cafés | Indirect | Cheap drip coffee on meal plans | No espresso, mediocre quality, and close early |

| Independent café, 3 blocks away | Direct | Good specialty espresso | Too far for a 10-minute class break |

| Convenience stores | Indirect | $1 self-serve coffee | No quality, nowhere to sit |

| Delivery apps | Indirect | Convenience | Fees, wait times, no place to hang out |

That table is the whole argument. There’s demand on this block, and nobody walkable is serving it well. The point isn’t to prove everyone drinks coffee but to show that enough of the right people, right here, will buy from you.

4) Products and services

Now, what are you actually selling, and why would anyone pay for it?

Anybody can list what they sell. What a lender wants to see is which offers carry the business and which are just nice to have, because that’s what tells them where the revenue really comes from.

So instead of cataloging everything, I sort the menu by the job each item does:

- The drivers. The high-volume, everyday sales the whole model leans on. For the coffee shop, that’s espresso drinks and brewed coffee, bought by the same people several times a week.

- The margin-makers. Lower volume, but each sale is worth more. Pastries and grab-and-go food, where the markup beats a $4 latte.

- The ticket-raisers. Things that lift the size of an average order or smooth out slow hours, like small catering runs for nearby offices.

For each one, I note the basics a reader will ask about anyway: the price, whether it’s available now or still planned, and any proof it works (early sales, a tasting event, a signed catering client). If something’s genuinely hard to copy, a roaster relationship, a signature blend, a prime lease, that goes here too, because it’s part of why the offer holds up.

Sort it this way, and the section answers the real question on its own: the offer is clear, it’s priced, people want it, and you can actually deliver it.

5) Sales and marketing strategies

How will customers find you, buy from you, and come back? That’s the whole section.

Most plans answer it with a vague “we’ll use social media and word of mouth.” A lender reads that as “hasn’t thought about it.” What they want is a channel plan with numbers attached, so let me show you what that looks like with the coffee shop.

Say the opening month runs like this:

- A Google Business Profile and local SEO put the shop in front of roughly 4,000 people searching “coffee near campus.“

- Campus flyers and a student-group partnership reach another 3,000 students directly.

- Local Instagram and an opening-week discount pull in maybe 1,000 more.

That’s about 8,000 people who hear about the shop. If 5% try it that month, that’s 400 first visits. If a third of them become regulars, you’ve got 130 repeat customers by the end of month one, the foundation the revenue forecast is built on.

Those numbers don’t have to be perfect. The point is that they exist. When you can show the path from “people hear about us” to “people buy, then buy again,” and roughly what each channel costs to get there, the marketing section stops being a wish list and starts being a forecast a lender can follow.

6) Operations plan

The operations plan shows how the business actually runs day to day and how it delivers everything the earlier sections promised.

It’s the piece that makes the plan work, the one that brings the concept to life. A marketing section can claim hundreds of customers a month, but this is where you show the business can produce and deliver for all of them, shift after shift. It’s the difference between a good idea and a business that can execute.

Here’s what I’d cover:

- Location and facilities: where you operate, the space and layout, the rent, and why the spot makes sense.

- Daily workflow: how an order moves from request to done.

- Staffing: who’s working, which shifts, what they cost, and when you’ll hire.

- Equipment and tech: the machines, software, or vehicles the work runs on.

- Suppliers: who you buy from, how often, on what terms, and a backup if one falls through.

- Quality control: how you keep output consistent as volume climbs.

The part I’d dig into hardest is whatever gets stretched first when things get busy. Every business has one, a retailer might be keeping stock on the shelves, a service business might be staffing at peak hours. Find yours now, on paper, while fixing it costs nothing.

7) Management team

The management team section shows who’s running the business and why they’re the right people to pull it off.

I keep this one short but specific. A lender doesn’t want a full resume for everyone; they want to know who owns the big responsibilities and whether the team can actually deliver the plan.

A strong management team section usually covers:

- Owner and key people: names, roles, ownership share, and the one or two managers, partners, or advisors who matter.

- Relevant experience: the past roles, industry time, or results that connect directly to this business, not a full work history.

- Who owns what: who’s responsible for operations, sales, money, and hiring, so nothing falls through the cracks.

- Hiring gaps: the roles you still need to fill and when you plan to fill them.

- Structure: a simple org chart or a line on who reports to whom.

For the Eugene coffee shop, that’s the owner’s ten years in specialty coffee, a shift lead, a couple of part-time baristas, and an outside bookkeeper handling the numbers, with food-safety and vendor know-how noted where it sits.

The job of this section is simple: show the business isn’t just a good idea, it’s a good idea with people who can run it.

8) Financial plan

The financial plan shows whether the business actually works on paper.

This is where I connect the idea to real numbers: how it makes money,/blog/write-financial-section-startup-business-plan what it costs to run, when it breaks even, and whether it can repay a loan or fund its own growth. A lender will spend more time here than anywhere else, so it has to hold together.

A strong financial plan usually includes:

- Startup costs: the one-time costs to open the doors.

- Sales forecast: expected revenue by product, channel, or customer type.

- Revenue assumptions: the logic behind the forecast, pricing, volume, capacity, and conversion.

- Cost projections: fixed and variable costs, payroll, rent, inventory, and marketing.

- Cash flow projection: how cash moves in and out each month.

- Income statement and balance sheet: profit and loss, plus assets, liabilities, and equity.

- Break-even analysis: the point where revenue covers costs.

- Key ratios: gross margin, net margin, and debt-service coverage lenders check.

The trick is that every number ties back to something earlier in the plan. Take the coffee shop’s $120,000 request; it shouldn’t be a round guess. It should break down:

| Startup cost | Amount |

| Espresso machines and equipment | $45,000 |

| Buildout and furnishings | $40,000 |

| Initial inventory (beans, milk, supplies) | $8,000 |

| Permits, licenses, and legal | $7,000 |

| Working capital (first 3 months) | $20,000 |

| Total funding request | $120,000 |

The sales forecast is based on those ~130 steady customers for the first month, plus walk-ins, who typically pay about $6 per transaction. When a lender can trace the ask to a cost breakdown and the revenue to a customer count, the plan reads as real instead of hopeful.

The goal is to have numbers that are believable, connected, and easy to check.

9) Funding request (Optional)

Only include funding request section if you’re actually asking for outside money. If the plan is just for you and a cofounder, skip it; there’s nothing to request.

If you are raising, this is where you tell a lender or investor how much you need, what type of funding you want, and how you’ll use it. Don’t make the reader hunt for the figure. Put the total right up top, in the first line or two.

A strong funding request usually covers:

- The amount and type: the exact figure, and whether it’s a loan, a line of credit, equity investment, or your own contribution.

- Use of funds: what the money buys, tied to your startup costs rather than re-listed from scratch.

- Timeline: when you need it and what it unlocks.

- Repayment or return: how you’ll pay back a loan, or how an investor eventually sees a return.

- Future needs: whether you expect to raise again later, so there are no surprises.

For the Eugene shop, the ask is the $120,000 from the startup-cost breakdown above, requested as an SBA-backed term loan, with repayment coming from operating cash flow once the shop clears break-even. Instead of re-listing where the money goes, the request just points the reader back to that table and shows how the loan gets repaid.

The whole point is an ask that’s specific, reasonable, and lines up cleanly with the financial plan a lender just read.

10) Appendix

The appendix runs on one rule: nothing goes in here unless it backs up something you already said.

It’s the easy section, but that rule is what keeps it from becoming a junk drawer. A lender questions your rent assumption? The lease draft is here. They doubt your equipment costs? The supplier quotes are here. Every attachment exists to answer a “prove it” before the reader even asks, such as the detailed financial tables, legal documents, supplier quotes, a sample menu, founder resumes, and your data sources.

For the Eugene shop, that’s the lease, the equipment and supplier quotes, the menu, the permit checklist, and the full financials behind section eight.

So keep the main plan clean and let the appendix carry the receipts. And if you’re unsure how a complete plan fits together end to end, a library of sample business plans is the fastest way to see the whole thing in context before you build your own.

Start preparing your business plan with AI

Once the outline’s ready, the real work is turning those notes into a full draft, section by section.

You can write each part by hand, or speed it up with an AI tool like Upmetrics’ business plan generator, which drafts each section in order from the structure you’ve built. Either way, I’d review the result closely. AI gets you a fast first version, but the assumptions, the numbers, and the funding ask are yours to verify; those are the parts a lender will test.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

What is the basic outline of a business plan?

Can I write a business plan myself?

Do I need a business plan outline if I'm just starting a small business?

Are there any free business plan outline template available for a business plan?

Upmetrics

Upmetrics is the #1 business planning software that helps entrepreneurs and business owners create investment-ready business plans using AI. We regularly share business planning insights on our blog. Check out the Upmetrics blog for such interesting reads. Read more