Many founders begin with loose ideas: a rough direction, a problem they want to fix, or a general sense of who the customer might be.

And that’s completely fine.

Clarity isn’t important at the start. What matters early on is to have a process that helps you turn that uncertainty into a workable plan.

Over the past decade, I’ve helped hundreds of founders do just that. I began as a builder and programmer, but soon realized the bigger challenge wasn’t building products; it was helping people make sense of their business ideas. That question eventually became the foundation for Upmetrics.

In this blog, I’ve outlined the same steps I guide founders through when they want to move from scattered thoughts to a clear, practical business plan. The aim is simple: give you a structure you can rely on, no matter how early your idea is.

Let’s dive right in!

1) Define your core idea and value proposition

First of all, define the core idea of your business. Before you analyze markets and estimate costs, you need to clarify exactly what you’re building, who it’s really for, and what makes your approach a better fit than existing choices.

If you can’t answer that, the rest of your business planning process will stay shaky.

You don’t have to write amazing sentences; just straighten out your own thoughts. The more plain you are here, the more you can decide to make choices later, what to build, set a price, or even discuss it.

This is how I usually break it down when working with founders:

- What you offer: Don’t describe the features—describe the outcome. What actually changes for your customer after they use your product or service?

- Who it’s for: Be honest about who you’re really helping. You can always expand later, but you can’t be everything to everyone at the start.

- Why it’s better: Focus on the one thing that makes your approach stand out. Maybe it’s faster, simpler, or fits better into how people already work.

Look at Apple. Their value proposition is incredibly clear: Beautifully designed technology that just works. That’s it. They don’t lead with specs or discounts. Every product, store, and ad connects back to that one idea.

So, here’s a small trick I use when mentoring founders: Try to explain your idea to someone outside your industry in one plain sentence. If they get it right away, you have defined the core well enough to continue with the rest of the planning work.

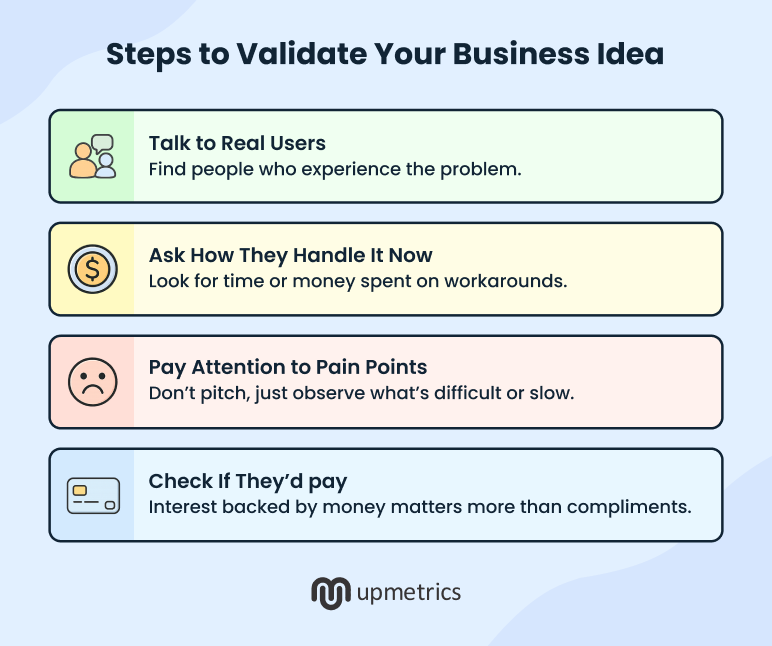

2) Testing if people actually want it

Your idea might sound great to you, but it only works when it reflects real demand. This is the point where I’ve seen many founders (including myself early on) assume too much. So, the question is simple:

“Do people actually want the product or service you plan to offer?”

The only way to know is to talk to them and evaluate the problem you aim to solve.

Most founders don’t pay attention to this part or ask for feedback from friends. This rarely gives accurate signals. But the real validation comes from people who face the problem daily and have no reason to sugarcoat their answers.

This is from my own experience: You will learn a lot more from ten real conversations with customers than a hundred survey. These conversations are your opportunity to hear what people really struggle with, what people pay for, and what they want to work better.

When you’ve those insights, refine your idea and adjust your early assumptions before you move forward in the planning process.

Keep in mind that now is better to make adjustments to your direction than to go out and rebuild your plan after launching something that does not match real demand.

3) Analyze and study the market you’re entering

Once you’ve tested your idea with real customers, the next step is to study the market you’re planning to step into. Every market already has its established players, common patterns, and noticeable gaps.

Here, I must say, your goal is to see the full picture: who dominates attention, where they’re strong, and where the space still feels underserved. This lets you build a business plan based on facts, not assumptions.

The following are the three practical angles to understand your market clearly:

Identify the key competitors

Find out who already has your customer’s trust. Study what they offer, how they position themselves, and how they price. Pay close attention to the standard expectations they have created. Why? Because your customers will compare you against those.

Understand customer pain points

Look for areas that feel slow, confusing, or inconvenient for customers. These frustrations often reveal where you need improvement. Improving something people already want often works better than introducing a completely new behavior.

Review customer spending patterns

Track where your target customers already spend and why. If they’re paying for partial fixes, you have space to build something better. But if your reachable market can’t support your break-even point and a fair margin within a year or so, rethink your scale or pricing.

Take Netflix, for example. When people were still renting DVDs from stores, Netflix noticed a steady increase in the number of customers willing to pay for mail-delivery rentals.

This trend showed that convenience was valued more than in-store browsing. That insight helped them build a subscription model and later shift to streaming.

That said, the better you know who your customers trust, what still annoys them, and how they make their decisions, the easier it is to fill the gap that has been left open by other people.

4) Figure out how you’ll make money

After understanding the market, map out the ways your business will actually make money. This gives you a clear explanation of how customers will pay you and what it will cost to deliver your products or services.

I think it’s a solid financial base for your plan before you move into detailed projections.

Begin by tracking the customer behavior: How are people already paying to get similar solutions? One-time buy, subscription, or pay-per-use? Before attempting to be innovative with pricing, stick to what is natural. Make it simple to the extent that you can describe it in a single sentence.

Focus on one main source of revenue first. Test it, refine it, and prove it works. Once you see traction, you can always expand into additional streams later.

Then, do a quick reality check with rough numbers. Even basic math can show if your idea makes financial sense:

If your price is $500, your gross margin is 60%, and your monthly fixed cost is $200,000, then your break-even point would be:

Break-even units = Fixed Costs ÷ (Price × Margin)

= 200,000 ÷ (500 × 0.6)

≈ 667 units per month

That is not an entire model, but it falls a-lightning on you.

Understanding how revenue, costs, and margins connect will make the rest of your planning far easier and far more accurate.

Turn your ideas into clear financial plans

Use our financial forecasting tool to build accurate projections

5) Define your strategic goals and positioning

Positioning refers to how you’d like people to think about your business: the position or space you rely on in your prospects’ and customers’ minds. It affects pricing, messaging, and who you target.

Here, you’ll need to address: Are you offering a premium product or a budget-friendly one? Are you serving a specific niche or a broad market?

You don’t have to appeal to everybody; you only need to stand out clearly to the right audience.

Once you know your positioning, define what success looks like in the first year. In other words, “What do you and your stakeholders want to do in year one?

Avoid saying something like “Grow fast,” as it’s intentionally vague and doesn’t help anyone other than the vendor winning a contract. Instead, you might set measurable and evaluative meaningful goals, such as:

- $100K in revenue or 500 active users

- 90% customer satisfaction or repeat purchase rate

- Launching successfully within one particular target market or segment

A clear position and well-defined goals give your business a steady direction, focus, and a realistic path to growth. Also, this makes the rest of your plan easier to build and evaluate.

6) Plan your operations and resource requirements

Now, figure out how your business will actually run—the people, tools, systems, and resources that keep things moving. A great idea won’t go anywhere if the operations behind it are weak.

After working with many startup founders, I would say that a few of them primarily focus on revenue or marketing, but overlook the day-to-day setup needed to serve customers. That’s what this stage is for—mapping the essentials so your plan is not just strategic, but workable.

The following are key factors to keep in mind when planning your operations:

People: Identify the essential roles first. An effective generalist can work with more than several specialist at an early stage. I usually recommend hiring where the work is recurring, high-impact, and not easily automated or outsourced.

Tools: Select low-cost, trusted software to run a project, accounting, customer relationship management, and customer support. The right tools are both time-saving and cost-effective, so you remain productive without increasing headcount unnecessarily.

Suppliers and Partners: In case your business is reliant on suppliers, manufacturers, or service providers, make sure you get reliable people early. Good relationships can make or break you into a smooth sail or a stagnant state.

Processes: Document how tasks are done, even the simple ones. Clear systems help maintain consistency and reduce confusion as your team expands.

In short, design operations that are lean, deliberate, and adaptable. Build only what’s needed to serve your customers effectively today—not what looks impressive on paper.

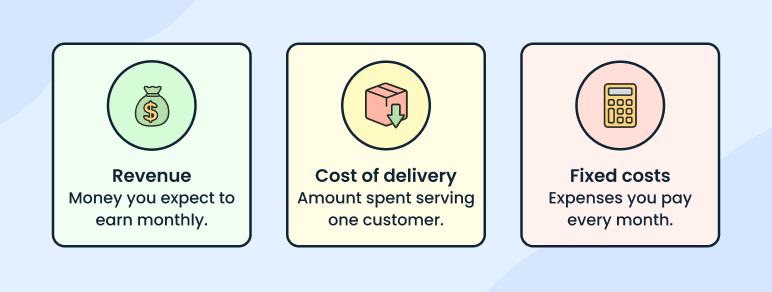

7) Make rough financials and cost estimates

Start simple. This step is about clarity, not precision. Write down three things: What you’ll earn, what it’ll cost to deliver your offerings, and what you’ll spend to keep the lights on. That’s all you need for now.

You can break this step into three parts (I personally use this when reviewing early plans):

- Revenue: Estimate how many customers you expect to reach each month and at what price. Rough numbers are fine at this stage.

- Cost of delivery: Calculate what it takes to serve one customer. Include materials, time, software fees, and the labor hours needed from your team or contractors.

- Fixed costs: Outline the expenses you pay no matter what, like rent, salaries, software subscriptions, or marketing.

Once you have these numbers, do a simple check. If your expected revenue cannot cover your fixed costs within a reasonable timeline, you may need to adjust your pricing, assumptions, or model.

Further, review your runway. Divide your available cash by your monthly burn rate to see how long you can operate with your current plan.

Avoid getting stuck perfecting spreadsheets. At this stage, you are looking for patterns, gaps, and early signals. Your first set of numbers will not be exact, but they will guide the questions you need to explore in the next steps of your business plan.

8) Plan how you’ll get early customers

As part of your business planning process, outline a simple approach for how you will reach your first set of customers.

You do not need a full marketing strategy at this stage. What you need is a simple, practical starting point that shows how people will first discover your product or service.

I suggest: You start by identifying where your target group already spends time. This could be specific online communities, industry groups, local networks, or social platforms they actively use. Choosing existing spaces keeps your early outreach efforts focused and manageable.

Next, test a few straightforward channels such as:

- Direct outreach

- Email or social posts

- Short campaigns

- Community discussions

- Local events

- Partnerships with people who already serve your audience

As you begin these small tests, pay close attention to what prompts interest and what creates hesitation. I’ve found that these early reactions often tell you more than any formal survey. This allows you to refine your message and understand what is important to them.

Moreover, you can use these early signals to prepare a more structured customer acquisition section of your final business plan.

9) Draft a comprehensive business plan

At this stage, bring everything you’ve worked on into a clear, practical business plan.

In reality, founders often ask, “How detailed should it be?” or “Do I need one if I’m not pitching investors yet?”

Well, the truth is: The plan is as much for you as it is for investors or lenders. It can help you make your ideas straight, identify gaps early, and realize how your idea can work in real life. No need to complicate it and get it graphical.

Begin by outlining the basic elements of a business plan: what you are building, who it serves, how it works, what resources it requires, and what success looks like in measurable terms. These become the foundation of your plan and help guide decisions as you move forward.

Next, arrange them based on your purpose.

If the plan is to get funding or a loan, then you include the financial projections and assumptions supported by the details your audience expects.

If the plan is for internal or operational use, you need to spend more time on the implementation steps, timelines, and roles.

I am not asking you to create it from scratch. Use a simple template or build it directly inside a business planning tool like Upmetrics. It walks you through each section and helps you turn your notes into a structured plan.

And remember that a business plan is not a one-time document. Every few months, you will need to revisit it to update your goals, refine assumptions, and adjust your focus as you learn more about your audience and market.

Struggling to Draft Your Business Plan?

Let Upmetrics AI Plan Generator turn your idea into a solid plan.

Plans starting from $14/month

Keep reviewing and updating your strategy

One thing that I have learned is that a business plan is not a one-time document. It should evolve with your business. Markets shift, customer behavior changes, and your priorities evolve as you learn more. That is why your plan should be reviewed and updated.

The cleverest founders do not recreate everything; they simply continue to improve what is already in place. It’s good to look at your business plan periodically after every few months.

Use each review to update your goals, refine your assumptions, and adjust the projections. It also helps you stay realistic about what is working, what needs attention, and where your next focus should be.

The habit can ensure that you leave behind the usual business plan mistakes, and ensure that your company remains stable, flexible, and on the way to growth.

Overall, a business plan grows with the business. Regular updates keep it relevant and help you make clearer decisions as you move forward.