If you’ve never written a business plan before, the hardest part isn’t filling in the sections. It’s knowing whether what you wrote is actually any good. You pick a template, finish the draft, and it looks reasonable enough to send off. (Hope for the best, as there’s no real way to verify it.)

Meanwhile, the lender or investor is not reading your plan front to back. They scan a few specific sections and decide in the first few minutes whether the rest is worth their time.

So when a plan gets rejected, it’s not because the business idea is weak. It’s a few common business plan mistakes sitting right where they looked.

That’s why I’ve put together this article on the 13 planning mistakes you should avoid to get funded.

Mistake #1: No clear purpose for the plan

A few weak business plans I’ve come across aren’t badly written. They’re just unclear about who they’re for.

When a plan is trying to serve a lender, an investor, and your own team all at once, it ends up doing none of them well. Because each reader is asking a different question.

Your own team wants to know what to do on a daily basis. A lender wants to know if you can repay the loan. An investor wants to know if this can grow or become huge. The same document can’t answer all three at once.

Almost every first-time founder makes this mistake. You want the plan to “work for anyone who reads it,” so you try to cover all bases. But a reader evaluating with one lens finds the plan doesn’t fit either. And it helps no one.

So pick your main reader before you write anything. Keep them in mind as you go.

- For a lender or SBA loan officer, start with cash flow, debt coverage, and collateral.

- For an investor, focus on growth potential and market size.

- For yourself or your team (internal business plan), cover goals, operations, and each person’s responsibilities.

If you need versions for more than one audience, my advice is to start with the lender plan and adapt from there, since it’s the most demanding of the three.

Mistake #2: Weak or generic executive summary

The executive summary is the one section a lender or investor will definitely read. If it doesn’t make your case on the first page, the rest of the plan usually doesn’t get a look.

A lot of weak summaries spend the first 200 words on the founder’s origin story before the reader has any idea what the business actually does or how much money you’re asking for. By the time you get to the part that matters, they’ve already moved on.

A strong summary works the other way around. It’s not an introduction, it’s a one-page pitch. It should cover these five things:

- The problem (what gap exists in the market)

- Solution (what your business does about it)

- Market (who specifically you’re serving)

- Traction (what’s already working)

- Funding ask (exactly how much money you need & what for)

That’s the whole thing. No founder story, no adjectives, no padding.

Mistake #3: Vague or undefined target market

The target market section in many first-time drafts says something like “anyone who needs better software” or “small business owners across the US.”

That kind of vague targeting affects the rest of your plan. You set prices without knowing what the buyer will pay. You write marketing copy that could be about any business. You project revenue from a market size you can’t back up.

There’s a real cost to leaving it vague. A recent CB Insights report found that 43% of failed startups shut down due to poor product-market fit (they built something the market didn’t need). The target market section is exactly where a lender checks whether you’ve answered that question or you’re still guessing.

Founders usually know this already. They just don’t do it, because the second you write down a specific customer, it feels like you’re shutting the door on everyone else.

A narrow market on paper doesn’t shrink your business. It shows the lender you’ve thought about who you’re starting with. And it helps you/your team make informed decisions about pricing, marketing, and where to spend your first dollars.

Take these two, for example. “Small business owners” are doing zero work. “US-based SaaS founders with 5-25 employees raising a seed round” tells the lender exactly who you’ll price for, market to, and go up against.

So pick the smallest version of your customer that’s still a real business. The wider market comes later.

Mistake #4: Ignoring your competitors

“We don’t have any competitors,” or “Our main competitor is outdated,” is one of the most common ways a plan loses credibility. It tells the reader you’ve already decided the competition doesn’t matter, which is the fastest way to look like a first-time founder.

Many plans do include a competitor section. But the problem is what’s in it.

Founders name two or three obvious players, point out one weakness in each (their pricing is high, their UX is dated, their support is slow), and conclude the market is wide open. That’s not analysis. That’s dismissal.

Here’s what a credible competitor section covers:

- Direct competitors (businesses selling something similar to similar customers)

- Indirect competitors (different products that solve the same problem)

- The status quo (what your customer is doing right now without you. Often the biggest competitor, almost always the one founders skip)

For each one, write three things: Their real price, what their customers complain about, and one specific reason a customer would choose you.

You can do that kind of research by reading 1-2 star reviews of your closest competitors on Trustpilot, Yelp, or G2. Look for complaints that come up more than once. Those are the unmet needs your plan should promise to fix.

Then call 5-10 people in your target market and ask what they use now, what they really switched to, and what would make them switch.

If that sounds like a lot, there’s a structured way to do it. Check how to validate the business idea, and follow the steps there.

Mistake #5: Unrealistic financial projections

Your financial projections are where lenders verify that you understand your own business. Either the numbers tie to real operating decisions (customers per week, price per customer, marketing spend) or they’re a guess that looks like a forecast. Lenders spot the difference fast.

The Kansas City Fed’s Q4 2025 lending survey found that around 72% of banks cited borrower financials as the top reason they denied a loan, more than any other factor.

The most common failure mode is the “hockey stick” forecast: Revenue stays flat in Year 1, then shoots up sharply in Years 2 and 3, with no increase in costs, staff, or marketing to explain the jump.

In a credible forecast, every number comes from a real operating decision: Cleaners hired, homes cleaned, marketing spend. Costs grow with revenue.

Beyond the hockey-stick shape, three things lenders look for on every forecast:

- Gross margins in line with your industry. Cleaning services run 35-45%, SaaS 70-85%, and restaurants 60-70%. Margins meaningfully above your industry’s norm tell the lender you forgot a cost (usually labor).

- Costs scaling alongside revenue. Headcount, suppliers, and marketing grow as revenue grows. Real businesses don’t quintuple revenue with two people and a $400/month ad budget.

- Every revenue line backed by buyers, price, and channel. “5,000 customers × $100 × email + retargeting” is a forecast. “$500K in Year 2” is a guess.

So build projections from the ground up. Start with how many customers you can realistically serve in a week, multiply by your price, and let revenue come out at the end. Then check your numbers against the industry benchmarking before you submit.

Mistake #6: Mismatched financial statements

Three financial statements that don’t agree with each other will sink a plan faster than missing one entirely. I’ve seen startup founders include all three (P&L, cash flow, balance sheet). The problem is that they get built in isolation, so the numbers don’t tie back to each other.

A lender opens your financial section to check whether the three tell the same story. Two specific checks happen first:

- Net income on your P&L should flow into retained earnings on your balance sheet. If your P&L shows $80K in profit, but retained earnings don’t move by that amount (minus owner draws), one of the numbers is wrong

- Ending cash on your cash flow statement should equal cash on your balance sheet. If they don’t match, you’ve either made a math error or skipped a transaction

If the numbers don’t match, lenders assume you either messed up the math or made the numbers up. Neither gets a loan approved.

The three statements only work as a set because each one answers a different question:

- P&L: Are you making money? (Revenue minus costs over the year)

- Cash flow: Can you pay your bills next month? (Timing of money in and out)

- Balance sheet: What do you own, and what do you owe? (Snapshot of assets and liabilities at one point in time)

A founder who generates them separately (without cross-checking) almost always ends up with three documents that don’t agree. The fix is to build them together, treating each one as a check on the others. Most of the cash flow problems lenders catch start exactly here.

If you run a subscription business, lenders will also want to see your churn and retention numbers, not just your monthly recurring revenue. Without those, MRR is a number on a page rather than a trend they can trust.

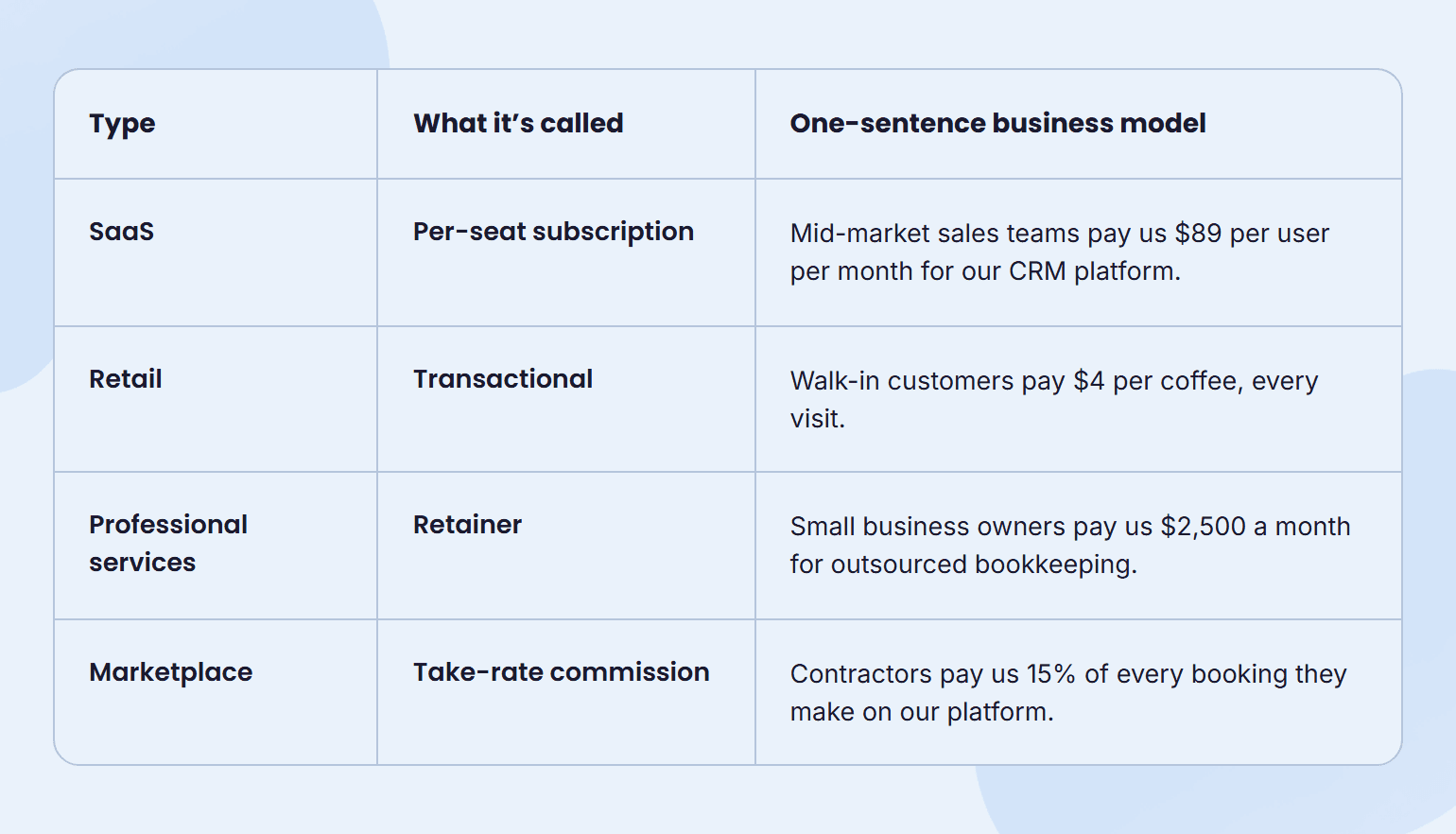

Mistake #7: No clear business model

It’s easy to mix up three things that aren’t the same: The product, the value proposition, and the business model.

The product is what you sell. The value proposition is why someone would want it. The business model is the actual money side: Who pays you, how much, and how often.

That last one is the part that usually gets skipped, and it’s also the part lenders read first. A quick way to check yours is to write it as a single sentence:

[Customer] pays us [$X] for [outcome] every [interval]

It sounds simple, but the sentence forces you to be specific in a way some plans never are. Here’s what it looks like when it’s done well, across four common business types.

Many first-time founders don’t actively pick a model. They copy whatever their nearest competitor is doing and inherit a model that may not even fit their customer.

If you can’t fill in the blanks for your own business, the lender has no math to check. The one-sentence model is the math: Customers × price × frequency = revenue. Without it, the financials are guesswork.

Mistake #8: No traction or milestones

A clear model gets you to the conversation. Traction is what proves the model is already working. The trap some founders fall into is confusing activity with traction.

How many investor meetings you took, how many features you shipped, how many LinkedIn followers you have, none of that is traction.

Traction is evidence that someone other than you and your team has moved toward your business with intent or money:

- 30 customer interviews

- 200-person waitlist

- Two letters of intent

- A paid pilot

- Recurring revenue

Even one or two of those is more credible than launched revenue without proof that anyone will buy a second time.

The other half of this is milestones. Milestones are traction in the future tense: A timeline of particular things you’ll prove in the next 12 to 18 months. “Hire two cleaners and reach $20K monthly revenue by Month 6” is a milestone. “Grow the business and become profitable” is not.

Specific, dated, measurable, tied directly to the funding the loan or investment will pay for. That’s what lenders check against six months in if you get funded.

Mistake #9: Missing or weak team section

The team section isn’t a resume. It’s the lender’s check on whether the people in the plan can deliver it. That means relevant experience beats impressive credentials every time.

A Harvard MBA running their first cleaning service is a weaker signal than a 10-year cleaning business operator running their second one.

If it’s just you, say so. The trick is to show you’ve thought about what’s missing.

“I’ll run operations and sales for the first 12 months. Once we cross $25K monthly revenue, I’ll bring on a part-time bookkeeper and a second cleaner, both already identified.” That’s a credible plan. “I’ll wear all the hats” is not.

List your key roles to fill, the milestone that triggers each hire, and a rough budget.

If you have co-founders or advisors, two lines per person on what they’re doing and why their background matches. This shows you’re already thinking ahead.

Mistake #10: Inconsistent numbers across sections

A $2M revenue target in your executive summary and a $3M target in your financial projections will end a meeting before it starts.

I’ve watched plans rejected over smaller mismatches. Lenders aren’t reading your plan to look for typos, but the second they spot one, every other number suddenly looks shaky, and now they’re checking. They almost always find more.

There are three spots where it tends to slip:

- Your revenue target in the executive summary doesn’t match the one in your projections.

- The headcount in your team section doesn’t match the salary line in your financials.

- The market size you cite in the market section is different from the one in the competitor section.

My advice to fix this is straightforward: Keep your core numbers in one spreadsheet or document, and pull every section from there. Build your financials first, lock in the big numbers, then go back and update the rest of the plan to match.

Mistake #11: Wrong length — too long or too short

There’s no perfect page count, but there’s definitely a wrong one.

From my experience, the working range that really gets funded is 15 to 25 pages for an SBA or bank loan plan, 10 to 15 slides for an investor deck, and 1 to 2 pages for an internal one-pager.

Going much beyond 25 pages doesn’t make your plan more credible. It just signals you couldn’t decide what was important.

If yours is on the long side, the answer isn’t trimming the main plan. It’s moving things to the appendix. Full resumes, facility layouts, market research reports, and detailed product specs all belong back there, with a quick reference in the main plan so a lender can find it if they want to.

What if your plan is too short, though? That’s the trickier one to fix. A short plan doesn’t mean you wrote tightly. It usually means a section is missing.

Before you cut anything from a long plan or call a short one finished, see if your plan covers the seven essentials: executive summary, business model, market and competitor research, team, financials, traction, and milestones.

If all seven are there, you can decide what to trim. If any are missing, the answer is to write, not to cut.

Mistake #12: No external review before submitting

Once you’ve spent 20+ hours on your own plan, your brain stops reading what’s on the page and starts reading what you meant. Someone else looking at it for 20 minutes will spot things you walked past 50 times.

So, whom you ask to review matters. Your spouse, your accountant, or a supportive friend will tell you it looks great. That’s not the feedback you need.

The best reviewers are the ones with no stake in your business and some experience with the kind of plan you’re writing. Here are the two good free options:

- SCORE mentors, who are retired executives volunteering their time

- Consultants at your local Small Business Development Center (SBDC)

Another founder who’s already gone through the same kind of funding application also works, as long as they’re honest with you.

Send the plan with four specific questions: What was the first thing you didn’t understand? What’s missing that a lender would expect? What part felt unrealistic? What do you think I’m asking for, in one sentence?

You’ll learn more from those four answers than from another weekend of editing your own draft.

Mistake #13: Treating the plan as a one-time document

The truth is, nobody opens their business plan after the loan gets approved. The folder gets closed, and the plan sits there for two years.

But your plan is the only document comparing what you said you’d do when you got the money to what you’re actually doing six months in. Your business will drift from the plan. That’s normal. The point is catching the gap while it’s still small.

There’s also a practical reason to revisit it. Many SBA loan agreements include reporting requirements, and some banks ask for periodic check-ins. If you haven’t touched your plan since signing day, you’ve got nothing to send.

A 60-minute review every 90 days is enough. Open the plan and run through three quick checks: numbers vs. forecast, milestones hit or missed, and any big assumptions that have changed.

That’s it. You’re not rewriting the plan. You’re catching where reality has drifted, while you still have time to fix it.

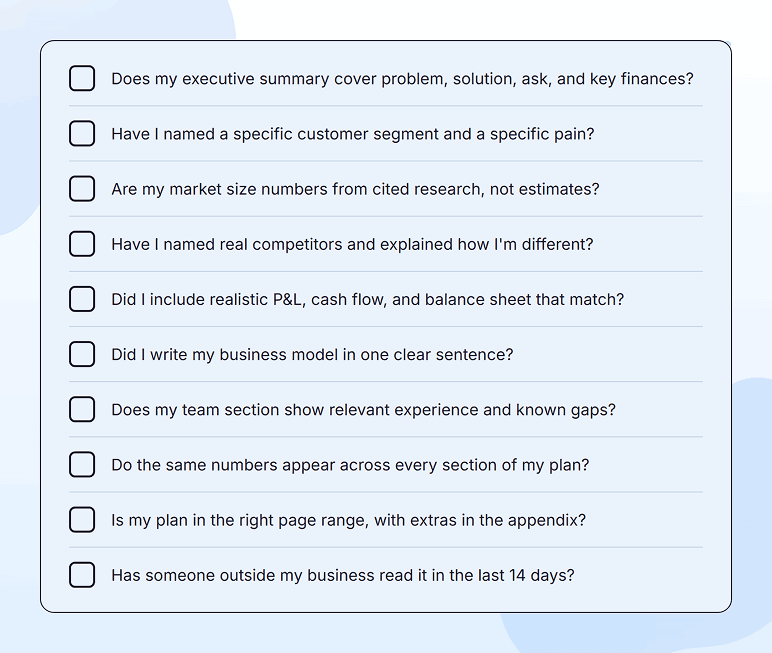

How to fix the most common mistakes — pre-submission checklist

You’ve read about all 13 common business planning mistakes. Now run your plan through them. Below, I’ve added a 10-question checklist that catches the patterns behind every mistake covered above.

Before you submit your plan to a lender or investor, sit down for 15 minutes and answer each question honestly. If every answer is yes, you’ve avoided what gets your plans rejected. If any answer is no, that’s where to fix before you send it.

For more reference on what a strong plan actually looks like, see investor-ready business plan examples. If you’re also building a deck for investors, pitch deck mistakes covers the visual side of the same problems.

Conclusion

Writing a fundable business plan isn’t about being a great founder. It’s about catching your own mistakes before a lender catches them for you.

Run through your draft with the 13 mistakes in mind, and you’ll be in better shape than any other first-time plans that get rejected.

If you’re starting from scratch and want help structuring your plan, I suggest Upmetrics is worth a look. It walks you through every section with guided prompts and real examples, plus built-in forecasting that keeps your numbers from going off the rails.

Wait no longer. Complete your draft and use the checklist before you submit.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

What is the biggest mistake when creating a business plan?

How long should a business plan be?

What should not be included in a business plan?

What are common errors in a business plan?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more