When investors read a business plan, they’re not starting from a neutral position. They’re already skeptical.

They’ve seen similar ideas before. They’ve seen strong narratives fall apart under basic questions. So they read with a filter: what doesn’t hold up here?

Most business plans aren’t written for that mindset. A business plan for investors is. It’s structured to reduce doubt.

That’s what this business plan for investors guide is built around. The 12 sections investors expect and the 4-W framework they use to judge them.

Why do investors need a business plan?

Investors use your business plan to verify three things: that the market is real, that the team can execute, and that the financials hold up under scrutiny. Everything else in the document supports one of those three.

So when an investor opens your plan, they’re not reading it cover to cover. They’re scanning for proof. As the SBA puts it, “Investors want to feel confident they’ll see a return on their investment”, and your plan is where they decide if that confidence is warranted.

Here’s how each category gets proven:

- Is the market real? Show market size and growth: TAM (Total Addressable Market), SAM (Serviceable Addressable Market), and SOM (Serviceable Obtainable Market) with defensible assumptions.

- Can the team execute? Show team credibility: domain experience, prior exits, and a hiring plan to close any gaps.

- Do the financials hold up? Show unit economics, runway, and exit math: each customer is profitable, the funding you’re raising buys enough time to hit the next milestone, and the investor can see how they get their money back.

If any one of those three falls apart, the rest of the plan doesn’t matter. A polished narrative around weak unit economics is just a slower rejection.

That’s the bar your plan has to clear.

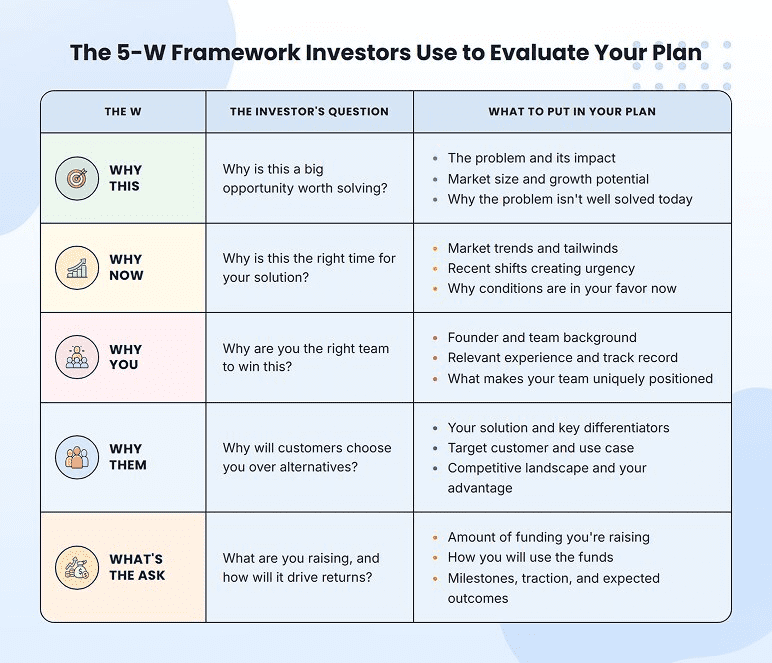

What do investors look for in a business plan? (the 4 W’s framework)

Investors look for one thing in a business plan: a clear why.

Why this problem, why now, why this team, and why this investor? If you can answer all four with conviction, the rest of the plan becomes a lot easier to write, because every other section is just supporting evidence for one of these four.

This is the 4-W framework, drawn from Sequoia Capital’s pitch deck template and adopted as the standard structure for evaluating an investor pitch. I’ve added a fifth W. What’s the ask, because no plan closes without it.

If you can answer all five clearly, the rest of your plan is supporting evidence.

Why this?

The investor is asking: Is the problem real, painful, and big enough?

This is where you prove the market exists in measurable terms, not as a “fancy idea.” Show the customer’s pain quantitatively: hours wasted, dollars lost, processes broken. Then size the opportunity using TAM, SAM, and SOM math. (More on that in the market analysis section below.)

If you can’t put a dollar figure on the pain, you don’t have a “why this” yet.

Why now?

The investor asks: What changed in the world that makes this possible today?

A great business at the wrong time is still a no. So the job here is to name the inflection: what specifically shifted in the past 18-24 months that opens a window for this business to win.

That inflection usually comes from one of four places.

- A regulatory shift (new compliance requirement, a deregulation event, a policy change).

- A tech breakthrough (a capability that didn’t exist or wasn’t affordable before).

- A cost curve crossing (something that used to be too expensive is now cheap enough).

- A behavior change (a customer segment shifting how they buy, work, or live).

Pick the one that actually applies to your business and prove it with a recent stat or a verifiable shift. “AI compute costs dropped 80% in the past 18 months” or “remote work adoption hit 35% of US knowledge workers post-2020” land. “The market is growing” doesn’t.

If you can’t name a clear shift, the honest answer is that the timing isn’t actually a differentiator, and investors will figure that out fast.

Why you?

The investor is asking: why is this team going to win, and what’s missing?

Show the operating experience that maps directly to this problem. Prior exits, domain expertise, and time spent inside the industry. If the founder has never sold to enterprises and the plan is to sell to enterprises, that gap matters.

Then own the gaps openly. List the two or three roles you’ll hire in the next 6-12 months and tie them to milestones. Investors trust founders who can name what they don’t have more than founders who pretend to have everything.

Why them?

The investor is asking: Why are you pitching me, specifically?

This one separates founders who’ve done their homework from founders who blasted 200 emails. Reference the investor’s portfolio, fund stage, sector thesis, and check size. Show why your deal fits their fund, not just any fund.

A line as simple as “we’re approaching you because of your work with [portfolio company] and your stated focus on [sector]” signals due diligence on the investor.

What’s the ask?

The investor is asking: how much, what does it buy, and when do I see returns?

State a specific raise amount tied to 12-18 months of runway and 2-3 named milestones. Vague or open-ended asks signal that the founder hasn’t done the math. (Full breakdown in the funding section below.)

How to write a business plan for investors

A business plan is your proof that you’ve answered the five Ws.

Each section below documents a specific assumption that an investor will challenge. The market analysis proves why this is. The traction and milestones sections prove why now. The team section proves why you. The funding ask and financials prove what you need and how the investor gets paid back. The plan’s job is to make those answers visible, defensible, and easy to verify.

The next question is what version of that plan you write, because length and depth depend on who’s reading it. Here’s the rule of thumb I follow:

- Pitching VCs or angel investors? A 10-12 slide pitch deck, a 3-5 page executive summary, and a working financial model.

- Applying for an SBA loan? A traditional 20-30 page plan with full financials, three-year projections, and detailed use of funds.

- Talking to corporate or strategic investors? A 15-20-page plan with an appendix tends to land best: dense enough to show rigor, short enough to read in one sitting.

If you pick the wrong format, you’ll either drown a VC in detail or hand a banker a deck that doesn’t answer their underwriting questions.

The 12 sections below apply to all three formats.

1) Executive summary

This is where most investor decisions begin. The rest of the plan only gets read if the executive summary clears the first filter.

Many seasoned VCs and angel investors only read the executive summary and make a decision on that page or two, whether to open the rest of the plan. Do not think of it as an introduction, but as an independent investment case.

This should be able to answer the fundamental investor queries without the help of this section being pulled out and emailed to a partner: What does this company do? Who pays for it? What is the motivation to construct today? Which are the achievements have been made so far? How much money would be required, and what would it help to demonstrate?

There are six components to a good executive summary:

Keep it to 1-2 pages, roughly 400-800 words. It can be arranged in two ways:

- Block Format: A clear heading paragraph with one or two tight paragraphs below each of the six elements.

- Narrative format: One page with short paragraphs for problem, solution, traction, market, financials, and ask.

It is never okay to have the reader ask, “Where is the business model?” “Where is the customer?”, “Where is the traction?”, or “What is the ask?”.

The test is simple. If an investor can decide after reading the executive summary alone, you’ve done it right. That means cutting adjectives, leading with numbers, and making sure the business model, customer, market size, and ask are all obvious on a first pass.

2) Opportunity

The opportunity section of your business plan will define the problem you are solving and the solution you have to offer. It introduces your products and services as well as highlights their key features and Unique Selling Propositions (USPs).

In this section, you’ll prove that your company is chasing a viable problem and you have a segment of customers willing to pay for your products and services.

3) Industry and market analysis (with TAM/SAM/SOM)

A big market number on its own doesn’t help. Investors want to see that you can define the market in a way that connects to your customer, your reach, and your path to revenue.

The framework they expect is TAM, SAM, and SOM:

- TAM: The full revenue opportunity if every possible customer bought your product.

- SAM: The slice of TAM you can actually serve, given geography, channel, and customer fit.

- SOM: The realistic share you can win in the next 3-5 years with your current team and capital.

Most founders stop at TAM. That’s a mistake. A sharp investor discounts “the global market is $50 billion” unless you show how that number narrows down to customers you can actually reach.

Say you’re building an HR software tool for US companies with 100-1,000 employees.

The TAM should be Global HR tech. Fortune Business Insights values it at $43.66B in 2025, growing at a 9.2% CAGR (Compound Annual Growth Rate). The SAM would be US mid-market companies in your target size band, and SOM would be a realistic 5-year customer count × average contract value.

If you can win 1,200 customers at an $18,000 ACV (Annual Contract Value), your SOM is $21.6M ARR (Annual recurring revenue) by year 5.

The goal is to show defensible assumptions: geography, segment, pricing, and conversion rate.

So, how to frame it by industry? Here is a breakdown industry-wise:

- Tech and SaaS: Lead with TAM/SAM/SOM and category CAGR. Cite named sources (IBISWorld, Statista).

- Services and local businesses: Skip global numbers. “240 medical offices within 20 miles, only 3 specialized cleaners” lands harder than a $400B industry figure.

- E-commerce: Focus on category demand, AOV (Average Order Value), channel mix, and repeat purchase behavior.

- Regulated industries: Define the market by your actual addressable customer base, and name the regulatory shifts driving demand.

4) Competitors overview

Investors are wary of any plan that says “no direct competitors.” That’s a warning sign. It means that the founder has not thought about the market or does not know it. In any business, competition exists even if it is just the status quo.

Name 3-5 competitors and one or more indirect competitors. The competition your customer has when he/she doesn’t purchase from you is indirect: spreadsheets, manual processes, an in-house team, or just doing without.

But if you’re a project management tool, you don’t just have competition from Asana, you have competition from Slack and the email workflow your prospect already has.

Compare all of the competitors for each of these axes:

- Product: what its features are and what they do better or worse than you.

- Pricing: price points, pricing model, and monetization.

- Positioning: who they are targeting and what message they are presenting to the target.

- Traction: Targeted fundraising, users, and revenue, growth rate.

- Differentiation: What they’re famous for & what you can do.

It should be a competitive matrix, and the output should be the matrix.

Finish off the section on your competitive advantage. I do not mean “we’re better than them. That is not an advantage. What you actually need is that competitors can’t copy you in the next 12-24 months, because of the tech moat, distribution channel, cost edge, and/or network effect. Choose one and demonstrate it.

5) Revenue model

Your revenue model section has to answer four questions: What does each customer pay? How often? What’s the gross margin? What’s your CAC-to-LTV ratio?

If any are missing, the section won’t hold up under investor scrutiny. Investors don’t fund pricing pages; they fund unit economics that work.

| Metric | Formula | Benchmark to clear |

| CAC payback | CAC ÷ monthly gross profit per customer | Median SaaS payback hit 20 months in 2024, Technavio; anything over 24 is a red flag |

| LTV/CAC | Lifetime value ÷ acquisition cost | 3:1 minimum, 5:1+ is best-in-class |

| Gross margin | (Revenue – COGS) ÷ Revenue | SaaS 75-80%+, e-commerce 30-50%, services 20-40% Metastat Insight |

| Burn multiple | Net cash burned ÷ net new ARR | Under 1.0 by $25-50M ARR (popularized by David Sacks) |

If you miss the benchmark for your category, the rest of the plan gets read with skepticism. So clear it and give investors the financial model the benefit of the doubt.

Close with two things: your pricing relative to competitors and why, and the revenue streams you plan to add in the next 18-24 months.

6) Milestones and traction

Investors want to see that your business is more than just an idea – they want to see some traction. However, not every traction is equal and includes it in measurable metrics such as revenue (MRR/ARR), customers, retention or churn rates, NPS (Net Promoter Score), signed LOIs (Letter of Intent), or patents filed.

Check off the areas that are relevant to your business:

- Revenue traction: MRR, ARR, total revenue to date, growth rate month over month.

- Customer traction: total customers, paid pilots, signed LOIs, named logos.

- Product traction: MVP (Minimum Viable Product) shipped, feature releases, usage metrics, NPS, or retention scores.

- Partnership traction: signed distribution deals, channel partnerships, supplier contracts, and reorder rates.

- Credibility traction: press mentions, awards, patents filed, advisor commitments from named operators.

Then list your next 12-month milestones with specific dates and metrics. “Launch by Q4” is weak. “Hit $50K MRR by month 9, close Series A by month 12” is fundable.

7) Team overview

Investors fund teams more than ideas. Most of them will tell you straight: a B-grade idea with an A-grade team beats the reverse every time.

So treat this section as a credibility test. Investors are evaluating three things:

- Relevant operating experience. Have the founders done something like this before? Sold to this customer, scaled this kind of company, navigated this industry?

- Domain expertise or prior exits. Years inside the industry, technical depth, and a previous company sold or scaled.

- Coverage gaps and how you’ll close them. Which key roles are missing, who you’ll hire in the next 6-12 months, and how that hiring is tied to your funding ask.

For each founder and key team member, write a 3-4 line bio: title, current role, prior companies, and the specific experience that maps to this business. Then map the org chart and call out the gaps openly.

Investors trust founders who name what they don’t have more than founders who pretend to have everything. That’s what lenders and investors look for in this section, more than credentials or polish.

8) Marketing and sales plan

The fastest way to lose an investor here is to list every channel you’ve ever heard of. SEO, social, content, email, paid ads, partnerships, influencer, events. What investors want is the story of how you actually acquire customers, told in numbers.

Start with 2-3 channels you’ve genuinely tested. For each one, show:

- CAC (cost to acquire a customer)

- Conversion rate

- Payback period

If paid search has a 14-month payback and partnerships have a 4-month payback, an investor immediately knows which lever to pull and whether your funding ask matches your unit economics.

- Then explain the sales motion. Does the deal close on the website, or does it need a 30-day cycle with three calls and a procurement review? B2B founders skip this constantly, then wonder why investors push back on their CAC math. A 6-month enterprise sales cycle with a $40K ACV and a $12K CAC works. The same cycle with a $4K ACV doesn’t.

- Don’t skip retention. Acquisition is the starting point. If your churn is 8% monthly, you’re filling a leaky bucket and your LTV math is fiction. Spell out the onboarding flow, the expansion path, and the churn benchmark you’re targeting. If you don’t have the data yet, name the metric you’ll watch and the threshold that would make you change strategy.

9) Company operations

This section shows whether you can actually deliver what you plan to sell. Investors aren’t looking for every operational detail. They want answers to four questions:

How does the product get made or delivered? Walk through the workflow from input to customer. For SaaS, that’s the dev cycle and infrastructure stack. For a coffee shop, its supply chain, daily prep, and customer flow.

What does the business depend on? Name your critical suppliers, tools, hosting providers, or distribution channels. Investors want to know what breaks if one of them goes away.

When does the team need to grow? Tie hiring to revenue milestones, not calendar dates. “We hire two AEs at $1M ARR” is stronger than “two AEs in Q3” because it shows the trigger.

How does quality hold up as volume grows? SOPs, training, QA, support workflows. The thing that keeps your unit economics from collapsing as you scale.

The depth of detail and the shape of operations both shift by business type.

| Business type | Workflow | Key dependencies | What changes as it grows |

| SaaS | Build, test, deploy, support | Cloud hosting, dev team, security tools | More QA layers, support tiers, and uptime controls |

| Local service | Booking, dispatch, delivery, follow-up | Staff, equipment, and local suppliers | More crews, route planning, and training systems |

| Product business | Sourcing, production, inventory, fulfillment | Manufacturers, packaging, logistics | Inventory controls, backup suppliers, and warehouse systems |

10) Financials

This is the section investors challenge most because it turns the rest of your plan into numbers. Your market, pricing, sales strategy, hiring plan, and funding ask all have to connect here in a way that makes sense.

The goal is to show that your numbers are built from clear assumptions. Start with the three core statements:

| Statement | What it shows | Why investors care |

| Profit and loss statement | Revenue, costs, and profit | Shows whether the business can become profitable |

| Cash flow statement | When cash enters and leaves the business | Shows whether the business can survive between sales, expenses, and payments |

| Balance sheet | Assets, liabilities, and equity | Shows financial position, debt load, working capital, and ownership structure |

Typically, the plans that investors are interested in contain 3-5 year projections. Typical format is monthly projections for year 1, quarterly or annual projections for subsequent years.

Available cash is typically the first place to examine when looking at cash flow because payments rely on cash flow. VCs and angel investors will pay more attention to margins, growth, customer acquisition, retention, burn rate, and runway.

Then add in the metrics that correlate to your business model:

| Business type | Metrics investors check |

| SaaS | ARR, churn, net revenue retention, CAC payback, LTV/CAC, gross margin, burn multiple |

| Local service business | Gross margin, break-even point, labor cost, repeat customers, and cash flow timing |

| Product/e-commerce business | AOV, repeat purchase rate, inventory cost, fulfillment cost, working capital |

| Asset-heavy business | Debt capacity, equipment costs, depreciation, utilization rate, cash flow |

Your assumptions matter as much as the final numbers. A line like “revenue grows 200% in year 2” means little unless the plan explains what drives it. Show the logic behind:

- Pricing

- Customer count

- Average order value

- Conversion rate

- Sales cycle

- Payroll

- Marketing spend

- Payment terms

- Cost of goods sold

Investors also judge financials by business stage. They judge pre-revenue businesses on startup costs, pricing logic, assumptions, runway, and the path to break even. An early-revenue business needs to show gross margin, customer acquisition cost, repeat sales, and cash burn.

At the growth stage, investors pay closer attention to revenue retention, hiring efficiency, operating margin, and cash flow. A fully-grown business should have profitability, debt capacity, EBITDA, working capital, and balance sheet health.

11) Funding demand

By now, you know the ask is one of the five questions investors expect answered. This section is where you actually answer it. Three things the section needs: how much, what kind, and where it goes.

How much and what kind? Are you raising debt (which you’ll repay with interest) or equity (which dilutes ownership in exchange for capital)? Investors expect the plan to specify which, and a hybrid ask without justification looks unfocused.

Where it goes. Break the use of funds down by category, with a percentage allocation tied to specific milestones. A typical early-stage breakdown looks something like this:

| Category | Allocation | Tied to |

| Engineering | 40% | Product roadmap, MVP build-out |

| GTM and sales | 25% | First 5 enterprise hires, channel buildout |

| Operations | 15% | Hiring infrastructure, tooling, ops lead |

| Working capital | 10% | Day-to-day cash flow buffer |

| Compliance and legal | 5% | IP filings, contracts, and regulatory work |

| Reserve | 5% | Unplanned expenses or extension of capital |

Numbers shift by stage and business model. Hardware will skew heavier on operations. SaaS skews heavier on engineering and GTM.

Close with the return. For equity, that’s the projected valuation at exit and the multiple. For debt, the repayment schedule and interest terms.

12) Appendix

The appendix is where you put everything an investor might want to verify, but doesn’t need to read upfront.

Include:

- IP filings, patents, trademarks

- Registrations, licenses, permits

- Product photos, screenshots, demos

- Detailed financial statements and projections

- Raw market research and survey data

- Full competitor research

This section is optional, but it’s quietly useful. When an investor flags a number or a claim and asks for backup, the appendix is where the answer should already be sitting.

A quick recap before we move on. Investors weigh financials, traction, and team most heavily, making those three sections defensible to the question level. The other nine build the case. These three close the deal.

Of course, knowing what to put inside the plan is only half the work. The other half is choosing the right document for the conversation you’re in. Up next, I’ll cover the difference between a business plan, a business proposal, and a pitch deck.

Business plan vs business proposal vs pitch deck vs what investors actually want

These three documents get mixed up constantly, and it costs founders meetings. Here’s how I’d think about it.

The pitch deck is your door opener. It runs 10-12 slides, mostly visual, built to complement your written plan in a first meeting or a cold email. Investors decide in two minutes whether to take the call.

The executive summary is what they read before they agree to that call. One or two pages. If it doesn’t land, the deck never gets opened.

The business proposal is for warm conversations where a real deal is on the table. It runs five to ten pages, focused on one specific funding ask, what it buys, and what the investor gets back. This is what most people are looking for when they search “business proposal for investors.”

The business plan is the long-form document. Around 15-30 pages, full operating detail, financial model attached. SBA lenders, corporate investors, and any serious diligence process will ask for it.

Most founders build only the plan and try to force it into every conversation. That’s backwards.

Build the deck and executive summary first, because those create the meetings. Then the financial model, since it travels with everything else. Then the proposal for warm deals. The full plan comes last, once you’ve heard which numbers investors actually push back on.

Stop juggling three different documents

Build your plan, deck, and financial model in one workflow

Exit strategy and risk analysis

Investors won’t fund a business unless they can see how they get paid back. That’s the whole point of the exit conversation. So keep it short and direct. Cover two things:

- How the exit happens: There are three realistic paths: acquisition (by far the most common), IPO (rare and only for late-stage growth companies), or a founder or management buyout. Name which one fits your business and why.

- What could go wrong on the way there: Most VCs expect a 5-7 year horizon and a 5-10x return on early-stage deals. Growth-stage investors typically target 3-5x over a similar window. Angels and strategic investors will work with longer holds.

Investors are going to find the risks anyway, so name them yourself. List three to five specific risks and how the plan mitigates each. Common ones include:

- Market timing. What happens if adoption is slower than projected?

- Regulatory. Pending or possible policy shifts that affect the model.

- Key personnel. Concentration risk on the founder or one technical lead.

- Competitive moat. What stops a well-funded entrant from copying the playbook?

- Capital risk. What happens if the next round comes in at a lower valuation or doesn’t close at all?

For a deeper walkthrough, see our exit strategies for business owners guide.

Build your investor-ready business plan with Upmetrics

Most founders spend 40+ hours on a single investor-ready plan: building three-year financial projections, formatting the executive summary, rewriting it three times after feedback, and stitching the deck together at the end. Then they hand it to an investor who scans it for two minutes.

Upmetrics’ AI business plan generator cuts that work down without weakening the output. Answer a few questions about your business, and it drafts each of the 12 sections this article covers, with prompts that adapt to your business type, stage, and the type of investor you’re pitching.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

How long should a business plan be for investors?

How is a business plan for investors different from a regular business plan?

What's the difference between a business plan and a business proposal for investors?

How can I make my business plan stand out to investors?

What are the most important sections of a business plan for investors?

Can I use a template for my business plan for investors?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more