If you’re like most new business owners, writing a business plan is probably the last thing you want to do right now. You’d rather test the idea, talk to customers, set up your product or service, or just start selling. I get it. A formal plan feels slow, especially if you’re not chasing funding yet.

But that’s exactly why I think “why is a business plan important?” deserves a better answer than “because every business needs one.”

A plan matters because it turns the idea in your head into something you can actually test. It shows you whether the numbers work, whether your customer is clear, whether the market is real, and whether you have enough cash to survive the early months.

So I’m going to give you 12 practical reasons to write one, each with a specific action step you can take today. By the end, you’ll know whether you need a full plan or a simple one-pager to move forward.

The short answer: why a business plan is important

A business plan is important because it makes you pressure-test the business on paper before you spend real money finding out whether it works. It pulls the idea out of your head and onto paper, where you can see if the customer, the pricing, the costs, and the cash actually hold up.

If you read nothing else here, read this. A plan is worth writing even if you never raise a dollar, because it catches the weak assumptions that turn into expensive mistakes later. Harvard Business Review covered research showing that entrepreneurs who write formal business plans are 16% more likely to achieve viability than otherwise similar entrepreneurs who don’t.

If you read nothing else here, read this. A plan is worth writing even if you never raise a dollar, because it catches the weak assumptions that turn into expensive mistakes later. Harvard Business Review covered research showing that founders who write a formal plan are about 16% more likely to achieve viability than otherwise similar entrepreneurs who don’t.

A plan helps you:

- See if anyone actually wants what you’re selling

- Know who your customer is, specifically

- Size up competitors before they catch you off guard

- Turn “grow the business” into goals with dates and numbers

- Spot the month you’d run out of cash

- Get a loan or investment, since lenders expect a plan

- Find the weak spots while they’re still cheap to fix

- Decide whether you need a full business plan or a simple one-page plan

What a business plan actually does for you

Before the 12 reasons, one thing worth clearing up. A plan isn’t valuable because you end up with a polished document. It’s valuable because of what writing it forces you to figure out.

Let’s think of it as the argument for your business.

Why should this exist? Who is it for? Why would anyone pay for it? What does it cost to run? How does it make money? What could go wrong?

That answers two questions at once: what is a business plan, and why is it important? If you want the full definition and structure, read our guide on what a business plan is.

A good plan does three jobs. It proves the idea by testing your market, pricing, costs, and cash flow before you commit serious money. It guides you by turning loose goals into actual decisions, milestones, and budgets. And when you need it to, it convinces other people, like lenders, investors, or a new hire, that the business has been thought through.

That’s why a plan still earns its keep even if you never raise money. The goal isn’t 30 pages because someone told you every business needs one. It’s getting clear enough to explain the business, make decisions, and catch weak assumptions before they get expensive.

12 Reasons why a business plan is important

Here are the 12 reasons a business plan is worth writing, even if you’re not chasing a loan or pitching investors.

1. It helps you test whether your business idea can work

An idea always sounds strong in your head. The plan is where it meets resistance. When you write down your price, your real costs, and how many sales it actually takes to break even, the math either holds up or it doesn’t. A weak assumption caught on paper costs you an afternoon. The same assumption costs you real money after launch.

Write down your price, expected sales volume, startup costs, and monthly costs, then sanity-check your logic against a few real business plan examples.

2. It’s what lenders and investors expect to see

A lender or investor won’t fund the idea that exists in your head. They fund the version you can put on paper and walk them through. The SBA is upfront about this; most lenders and investors expect a traditional business plan, and even if you start with a lean one, some will ask you to go deeper before they’ll move.

I know that sounds like a lot, but it really comes down to four questions they want answered: How much money do you need? What exactly will you spend it on? How does the business pay it back? And why should anyone believe your numbers? If you answer those four clearly, you’re most of the way there. Everything else in a funding plan is supporting detail.

Before you write anything else, pin down three things: how much you need, what you’ll spend it on, and how the business repays it. Then walk through our guide on what lenders look for in a business plan, so you know how they’ll read it.

3. It forces you to actually know your customer

Writing the plan forces you to define your target customer specifically—that one section decides your pricing, your marketing, and where you spend your first dollars. A customer defined too broadly can’t be reached affordably, no matter how big the market sounds. “Small business owners,” “busy parents,” “local residents,” these feel huge and safe, but you can’t run an ad or a promotion against a group that vague.

Writing the plan forces the specificity. A meal-prep business isn’t serving everyone who wants to eat healthy. It might be serving working parents within five miles who want four ready-to-heat dinners under $15 each.

Once the customer is that precise, the rest of the plan gets easier to fill in, pricing, packaging, delivery radius, and even the menu. Define them loosely, and you’ll spend real money reaching almost no one.

Write a one-paragraph customer profile naming who they are, what they need, what they use right now, and why they’d switch to you. If you can’t fill it yet, that’s the plan doing its job, pointing you at what to research.

4. It exposes your competition before they surprise you

The competition section of a plan makes you map how your customer solves this problem today, before you’ve spent money assuming they’ll switch to you. That’s where most founders go wrong. They list the businesses that look like theirs and stop there, missing the options that actually take the sale.

A new fitness studio will size up other studios. But its customers might just as easily choose a YouTube workout, the gym in their apartment building, a Saturday running group, or a $10 budget chain down the road. None of those looks like a competitor.

All of them compete for the same decision. Your real competition is usually whatever is cheaper, easier, or more familiar than what you’re offering, and you want to know that while you can still adjust your pricing or your pitch, not after launch.

List your top three competitors, including the indirect ones, then write one specific reason a customer would pick you over each. Our guide on competitive analysis walks through how to do this properly.

5. It turns vague goals into measurable milestones

The goals and milestones section forces every ambition you have into a number with a date attached, and that’s the only form a goal is actually useful in. “Grow the business” can’t be managed, because there’s no way to tell on any given Tuesday whether you’re doing it.

Be specific and turn that fuzzy goal into something you can actually check: book 20 paid discovery calls by March 31, hit $8,000 in monthly revenue by month six, and land 40 repeat customers before you make your first hire. Pick a number, pick a date. That’s it.

When you’re starting, you’re busy all the time, and a lot of that busyness feels like progress even when it isn’t. A dated milestone is the only thing that tells you the truth, whether the work actually moved the business, and whether to keep going, change the approach, or stop and rethink before you’ve burned another three months.

What you can do is write three milestones: one for sales, one for cash, and one for customers. If you can’t put a number and a date on a goal, don’t worry, it just means the goal isn’t finished yet. Keep working it until you can.

6. It catches cash-flow problems before they sink you

A cash-flow forecast tells you the specific month you’ll run out of money. Not whether you’re profitable, but the exact month your account goes negative if nothing changes. Once you can see that date coming three or four months out, you still have real options: trim a cost, delay a hire, push for faster payment.

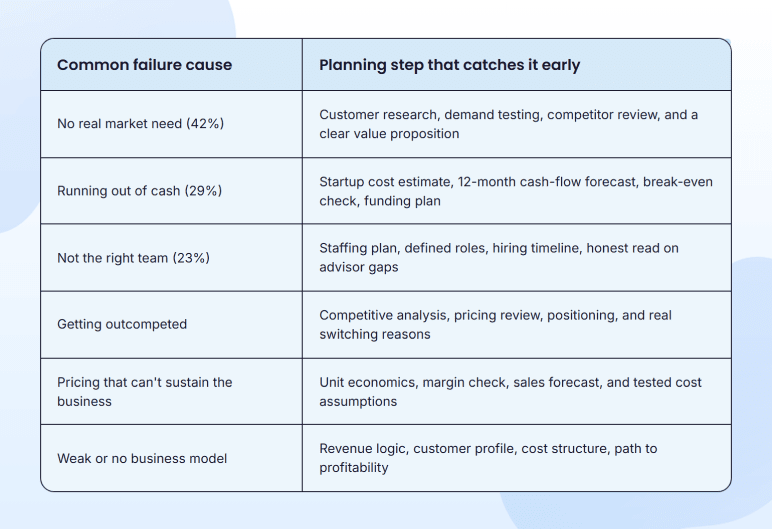

Learn the same thing from your bank balance instead, and there’s usually nothing left to adjust. CB Insights ranks running out of cash as the number one reason startups fail, with no real market need close behind, and a lot of that is just timing nobody mapped in advance.

Build a 12-month cash-flow forecast with opening cash, income, fixed and variable costs, debt payments, and ending cash. A rough version you actually finish beats a perfect one you never start.

7. It helps you make decisions under pressure

A written plan acts as a reference point for the decisions you have to make fast, before emotion or urgency makes them for you. Most hard calls in a young business aren’t hard because the answer is complex. They’re hard because they show up suddenly, and every option feels urgent.

A big one-time order at a thin margin. A second location before the first one’s steady. An early hire you’re not sure you can afford. When your plan already says, in writing, that the goal is to repeat local customers at healthy margins, that thin-margin order is easier to turn down without second-guessing it for a week. The plan won’t make the call for you. It keeps you anchored to what you decided when you were thinking clearly.

Keep a one-page summary of your customer, your offer, your pricing, and your top goals somewhere you’ll actually see it.

8. It shows you where to spend limited time and money

The budgeting and strategy sections of a plan make you attach every dollar and every week to a specific goal. That’s the only thing that stops a small launch budget from leaking away on things that merely feel productive.

Say you have $5,000 to start. That isn’t enough to cover a website, inventory, ads, equipment, and local partnerships all at once, so the plan makes you rank them by what actually moves you toward your next customer or your next dollar.

The part founders underrate is what this rules out. Deciding what you’re not doing this quarter is more important than adding one more thing to the list, and the plan is where that decision gets made on purpose instead of by default.

In scenarios such as this, go through your planned expenses and cut one item that doesn’t directly support your next customer, revenue, or cash-flow milestone. If cutting it feels hard, that’s usually a sign it was never tied to a goal in the first place.

9. It gets everyone on your team pointing the same way

A plan gives everyone you work with the same answer to three questions: who the customer is, what you’re selling them, and what you’re not doing this year. That shared answer is what keeps a small team from quietly working against itself.

Here’s how it goes wrong without one. A customer asks for a custom version of your product. Your salesperson says yes, and it closes the deal. Your one developer loses two weeks building a one-off. You watch the margin on that deal disappear.

Nobody did anything wrong. They were each doing their job. They just didn’t share the same picture of what the business is trying to be. When that picture is written down, the disagreement happens before the work, not after it’s already cost you two weeks.

So keep a one-page version of the plan and hand it to every new hire, contractor, or partner before they start, not after they’ve guessed what the business is about. That one habit prevents most of this.

10. It surfaces risks and weak spots early

Every founder already knows their business’s weak spot. It could be the supplier they’re a little too dependent on, or the one client who’s become half the revenue, or the launch date they’re privately not sure they’ll hit.

Writing the plan is what drags that out of your head and onto the page, where you have to actually look at it. And honestly, that’s uncomfortable for a minute. But it’s a lot cheaper to feel uncomfortable about your single-supplier problem now than to discover it the week they raise prices or go under.

That’s really all the risk section is for. Not to scare you, just to make you name the thing you’re already half-worried about while it’s still small enough to do something about, find the backup supplier, spread the revenue, pad the timeline.

Spend twenty minutes on it. List your real risks, what happens if each one hits, and what you’d do about it. That’s the whole exercise.

11. It links to better business outcomes

Most planning advice stops at “write the plan before you start.” That’s where competitors stop, too. The actually useful idea is what the plan does once you’re operating, when you can finally hold it up against what really happened.

Your sales forecast said 80 customers in the first quarter. You got 32. Your assumption was a $40 average ticket size. Reality came in at $58. You assumed paid ads would be your top channel; referrals are actually doing the work. None of that is failure. It’s information you couldn’t have had before launching, and it’s only useful if there’s an original document to compare against.

That’s what makes the quarterly review the real payoff of writing the plan. You’re not redoing the work. You’re updating the numbers, milestones, risks, and customer assumptions to match what the market just taught you, so the next quarter’s decisions are based on what’s actually true.

If you want to see more of the research behind this, our roundup of business plan statistics goes deeper.

12. It builds in an exit and a plan B

This part of the plan decides what you do if the business stalls, and what happens to it when you eventually leave. Both get decided either way. The only question is whether you decide them now, with options, or later under pressure with less cash and fewer of them.

The fallback is the part founders skip because thinking about it feels like admitting doubt. It isn’t. A business that misses its targets for months is common, not a failure of nerve, and the founder who already thought it through acts early instead of scrambling once the money’s gone.

The exit is the same logic, just further out. Selling the business, handing it off, or closing it cleanly is far easier when the books are clean, customers come back, and margins are steady, and none of that can be bolted on at the end. It’s built in from the start, or it isn’t there.

So write one honest paragraph: what’s your move if this doesn’t work, and what would make this worth buying from you later? The answer doesn’t have to be good yet. You just have to have asked before the situation asks for you.

Who needs a business plan most (and who can keep it lean)

Most founders need some kind of business plan, but the depth should match the decision, and some situations make a fuller plan urgent.

You need one most when you’re about to make a decision that’s hard or expensive to undo. Applying for a loan. Pitching investors. Signing a lease. Buying equipment. Hiring staff. Bringing on a partner. Moving into a new market. In those moments, the plan isn’t paperwork; it’s where you find out whether the decision holds up before your money is committed to it.

If you’re still testing a small idea, keep it lean. The SBA splits plans into two common formats: a traditional plan, more detailed and usually what lenders or investors expect, and a lean startup plan, shorter and focused on the essentials. For a fuller breakdown, see our guide on types of business plans.

| Who needs it? | Recommended depth | Why |

|---|---|---|

| Just have an idea | A lean one-pager | You need to pressure-test the idea fast. |

| Founders signing a lease or buying equipment | Full business plan | These decisions create fixed costs, so the numbers need to work before you commit. |

| Founders hiring employees or contractors | Lean plan at minimum; full plan if payroll is significant | People need clear goals, roles, priorities, and enough projected revenue to support the added cost. |

| Existing business owners trying to fix slow growth or cash-flow problems | Full business plan or updated plan | The plan helps compare what was expected with what is actually happening in sales, margins, demand, and cash flow. |

| Founders pivoting or expanding | Full plan for major changes | A new offer, location, or market changes the customer, costs, operations, risks, and cash needs. |

| Solo founders testing a small idea | Lean one-page plan | You still need clarity on the customer, offer, pricing, costs, and next steps, but you do not need a long document yet. |

| Side hustlers using personal savings | Lean one-page plan | A short plan is enough to prevent vague decisions and avoid spending money without a clear test. |

So, is a business plan really necessary? Yes, but the detail should match the size of the decision. Outside money, debt, payroll, a lease, or a major expansion means writing the full plan. Still testing demand means start with one page and expand it when the business actually needs more.

What it really costs you to skip the business plan

The cost is almost never just “no document.” It’s a decision made on weak information, launching something people don’t want, underestimating how much cash you’ll need, hiring before revenue can carry it, picking the wrong market, and signing a lease before the sales math works.

The early years are unforgiving with those mistakes. BLS data shows roughly one in five new businesses don’t survive their first year, and about half are gone within five. Planning doesn’t guarantee survival. What it does is help you avoid the expensive mistakes that come from untested assumptions.

Our guide on why business plans fail covers the mistakes that make plans less useful in the first place.

This isn’t a claim that every failed business would’ve been saved by a plan. Plenty wouldn’t. The honest point is narrower: a large share of expensive failures begin as small assumptions nobody tested, and the plan is the cheapest place to test them, while changing direction still costs you an afternoon instead of the business.

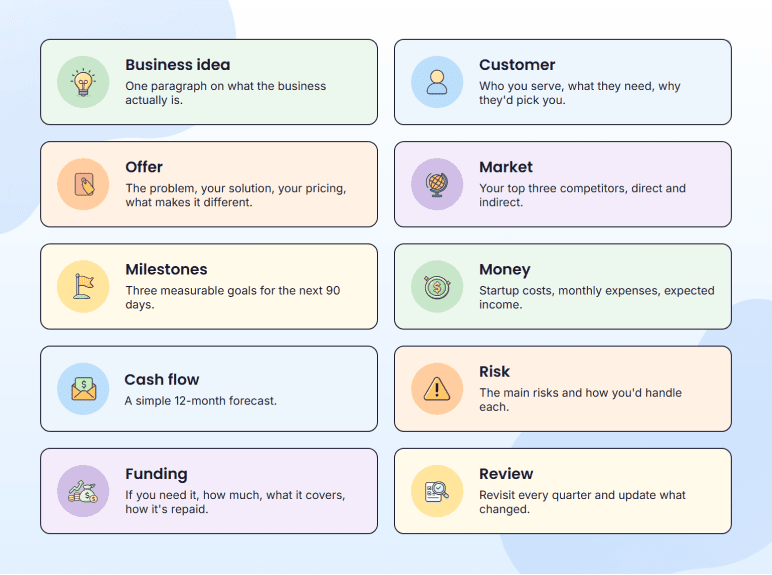

How to turn these reasons into an actual plan

You’ve basically done all the thinking. Every reason above was pointing at a part of the plan, the customer one, the cash-flow one, the risk one. Writing the plan is mostly just putting those answers in one place, in an order that makes sense.

Here’s the checklist. Go top to bottom, and don’t try to do it all in one sitting:

Still testing an idea? Do the first five and stop. That’s a real one-pager, and it’s enough. Raising money, hiring, signing a lease, or expanding? That’s when the rest is worth writing, with proper financials and operations details.

Upmetrics’ AI business plan generator gets you through the first draft faster, though the real work is still testing your assumptions before they cost you money.

Conclusion

If you came here doubting whether a business plan is worth the time, keep this: a plan is the cheapest place you will ever get to be wrong. An assumption you test on paper costs you an afternoon. The same assumption tested with real money can cost you the business.

That is the case for planning. The 12 advantages of having a business plan above are not abstract; each one is a practical use you can act on this week without ever raising a dollar. The customer work, the cash forecast, the risk list, all of it comes back to testing your thinking before it gets expensive to be wrong about it.

So start today. If a blank document is what is stopping you, Upmetrics walks you through each piece with guided prompts and builds the financials as you go, so you can start your business plan with the structure already there.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Frequently Asked Questions

What are the main purposes of a business plan?

What's the difference between a business plan and a business model?

How long does it take to write a business plan?

Should I write the business plan before or after starting the business?

Does having a business plan actually increase your chances of success?

How long should a business plan be?

Vinay Kevadia

Vinay Kevadiya is the founder and CEO of Upmetrics, the #1 business planning software. His ultimate goal with Upmetrics is to revolutionize how entrepreneurs create, manage, and execute their business plans. He enjoys sharing his insights on business planning and other relevant topics through his articles and blog posts. Read more